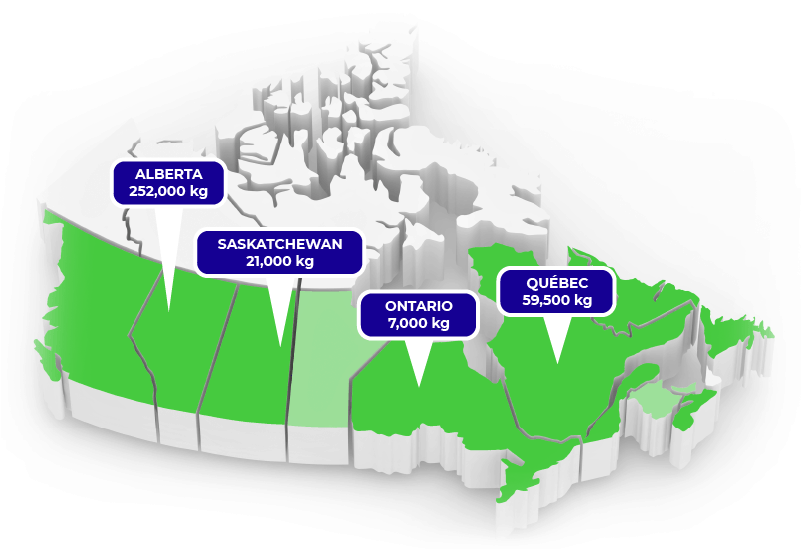

CAPACITY BY PROVINCE IN 2022

Aurora Cannabis Inc.

Ticker: ACB (TSX)

Stock Price (Feb 2018): $10.32

Grizzle’s Future Target Price: $5.80

Current Annual Capacity: 8,800 kg

Future Annual Capacity: 422,235 kg plus 120,000 kg of oil processing capacity

Aurora Cannabis Inc. is the second largest legal marijuana producer in the world after Canopy Growth Corp. Headquartered in Alberta, Canada, Aurora has plans to produce over 270,000 kg a year by 2021 from greenhouses in Canada, Denmark, and Australia. With the purchase of CanniMed and additional expansions they will likely be producing closer to 340,000 kg. The company will soon own a large oil processing facility as well that will make it the industry’s largest cannabis oil processor.

What is the Canapocalypse?

The wave of marijuana supply is coming. Hundreds of greenhouses are being built across Canada and as harvests begin to flood the market in 2019, the Canapocalypse (aka price collapse) will soon be upon us. Retail prices are going much much lower unless legal producers find other countries to absorb the excess supply.

In this 4-part series we take you through a full analysis of the 4 largest legal producers, explain what assets they own, the potential export opportunities, future growth potential and what the stocks are worth. After reading our report, you will be better able to navigate this exciting, but risky emerging industry.

For some background reading on the coming Canapocalypse, check out Up in Smoke, our deep dive report of the Canadian marijuana sector as well as The Marijuana Export Mirage, an in-depth analysis into global supply and demand of marijuana.

Management Team

Michael Singer – Chairman of the Board

Michael Singer is the chairman of the board for Aurora, but is also the CFO for Clementia Pharmaceuticals, a clinical-stage biopharma company. He has served as CFO for a number of small biotech companies and served as CFO of Bedrocan Cannabis Corp before it was acquired by what is now Aurora Cannabis. Singer received his bachelor’s degree in accounting and finance from Concordia University and a graduate degree in accounting from McGill University.

Terry Booth – CEO

Terry Booth began his career as an electrician, and has served as the president or CEO of 6 companies since his early twenties. He is currently the CEO of Aurora but is also the president of Superior Safety Codes, a permit and inspection agency in the province of Alberta. Booth graduated from the Northern Alberta Institute of Technology and is a master electrician.

Cam Battley – Chief Corporate Officer

Cam Battley is the public face of Aurora. He comes to Aurora from Health Strategy Group where he is still currently part owner. Health Strategies focuses on market intelligence gathering and communications for pharmaceutical and biotech companies. Battley served as director of communications for Eli Lilly and was also a legislative assistant to the Canadian Minister of Consumer and Corporate Affairs. He has very strong sales and presentation skills and handles investor and stakeholder outreach in North America.

Why does the management team all have second jobs?

We question why most of the management team have second jobs while trying to run a TSX-listed company at the same time. Competing in an emerging and rapidly changing industry is difficult enough even with a manager’s complete focus. We worry that without management’s full attention, the company may fail to achieve market leadership at home and abroad.

Domestic Expansion

Aurora has current sales of 4,000 kg a year and total capacity of 9,000 kg. By 2021 the company plans to produce 290,000 kg in Canada and another 61,000 in Denmark for total global capacity of 351,000 kg.

The recent acquisition of CanniMed Therapeutics included a giant cannabis oil processing facility that will have capacity to process 120,000 kg of dried flower a year (12% of demand in Canada) when construction is complete by early 2019. This will be the largest oil processing facility in Canada and will allow Aurora to compete as the industry leader in marijuana extracts such as gel capsules, oils, creams, etc.

Major Greenhouses

Aurora Sky – This facility in Edmonton, Alberta is the largest single greenhouse in Canada and is a good benchmark for judging construction time. Aurora Sky broke ground on October 30, 2016 and the full 100,000 kg a year of capacity is scheduled to be operational by June 2019, for a 32 month total construction schedule.

Aurora Vie – 40,000 sq ft facility in Quebec with growing capacity of 4,000 kg a year. The facility is currently operational with multiple ongoing harvests.

Aurora Mountain – The original Alberta facility. Aurora Mountain View has been producing since 2015 with a design capacity of 5,400 kg annually.

Aurora Lachute – 48,000 sq ft facility purchased in the acquisition of H2 BioPharma last year. The facility is located near the Montreal International Airport with capacity to produce 4,500 kg per year and should be operating at full capacity by year end.

CanniMed Saskatchewan – Aurora is completing the purchase of CanniMed, a legal producer with plans to produce 21,000 kg of dried flower by the end of 2019. CanniMed is also building a large oil processing facility that can handle 120,000 kg of dried flower a year. This will enable Aurora to turn most of their dried flower into value added products for the retail market if they so choose.

The Green Organic Dutchman – Aurora currently owns 17.62% of The Green Organic Dutchman (TGOD) with an option to increase the stake to 50%. TGOD capacity will be 116,000 kg by the end of 2019 or 58,000 net to Aurora at full capacity.

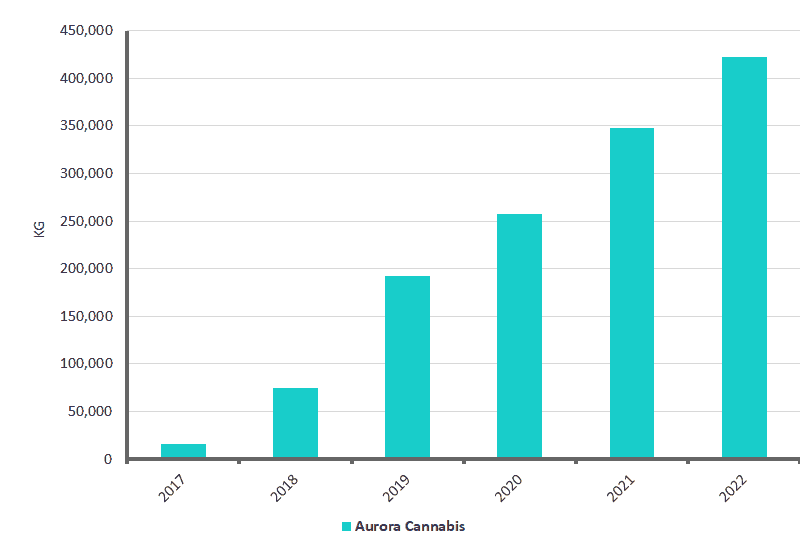

AURORA CANNABIS GROWTH CAPACITY BY YEAR

International Expansion

Management is aggressively diversifying the business by signing many different types of deals with overseas cannabis companies. Global expansion facilities in construction (Australia, Denmark) will add up to 81,000 kg at most, equal to 30% growth outside Canada.

The Netherlands

Signed a distribution and marketing agreement with Fagron NV of the Netherlands. Fagron will be the distributor of some or all of Aurora’s supply to Germany and other European countries. Volumes are dependent on European demand.

Germany

Aurora owns Pedanios, a large medical marijuana distributor in the EU. The company is currently applying for a German cultivation license and will also distribute exports from Canada in the interim. Aurora is currently exporting 1,000 kg on an annual basis to Germany.

Denmark

Established Aurora Nordic, a joint venture with a large European greenhouse operator to build a greenhouse in Denmark. Aurora owns 51% of the JV. Production from Denmark will be 120,000 kg or 61,200 kg net to Aurora when the greenhouse is complete in 2019. The Denmark facility will contribute 23% growth to capacity in 2022.

Australia

Aurora owns 22.9% of Cann Group, a medical marijuana supplier in Australia. Cann Group will have production capacity of 22,000 kg of supply in the next 2 years or 5,000 net to Aurora. Subsidiary CanniMed is currently shipping 60 kg equivalent per quarter to Australia for medical use. If Aurora buys out the rest of Cann Group, Australia will contribute 7% growth to volumes.

International Growth May Disappoint

Throughout history, when governments or companies want to gain corporate knowledge from competitors the easiest way to do so is to form a joint venture or consulting arrangement and then terminate the relationship once you have absorbed all the intellectual property of the other party. China has basically institutionalized this strategy of knowledge transfer.

Aurora looks to be going down a very similar path, signing joint venture agreements instead of setting up wholly-owned production facilities. In the process they are transferring growing techniques, strains and seed varieties to potential future competitors. International governments are committed to cultivating domestic sources of supply and international producers have publicly stated a desire to import marijuana only until domestic production can be built. We worry that long term, meaningful international demand for Canadian marijuana may not materialize to the extent expected by the market.

AS IT STANDS TODAY, INTERNATIONAL OPPORTUNITIES WILL ADD 23% GROWTH TO AURORA’S OVERALL GLOBAL VOLUMES IN 3 YEARS. NOT THE EXPLOSIVE GROWTH INVESTORS ARE CURRENTLY ANTICIPATING.

Aurora Cannabis Stock Valuation

To value Aurora we look at the steady state cashflow potential of the business, which for our purposes is 2022 when the Canadian market for flower will be largely mature. We then apply a steady state Enterprise Value (EV) to EBITDA multiple to arrive at the future value of the company. Taking the future value and discounting it back to today gives us the present value of Aurora’s shares.

Enterprise Value (EV) – The value of the entire company taking into account any debt outstanding and cash in the bank. Calculated as the total value of stock outstanding plus the value of debt minus cash in the bank.

EBITDA – Earnings before interest on debt, taxes and depreciation. Similar to the cashflow of the business.

Present Value – To the average person a dollar in your pocket today is worth more to you than a dollar in your pocket one year from now. Therefore, the future, higher value of a company needs to be adjusted back to its present value to see what it is worth to us TODAY.

USING A PROBABILITY WEIGHTED AVERAGE OF OUR UPSIDE, DOWNSIDE AND BASE CASE SCENARIOS, THE VALUE OF AURORA TODAY IS $5.80/SH.

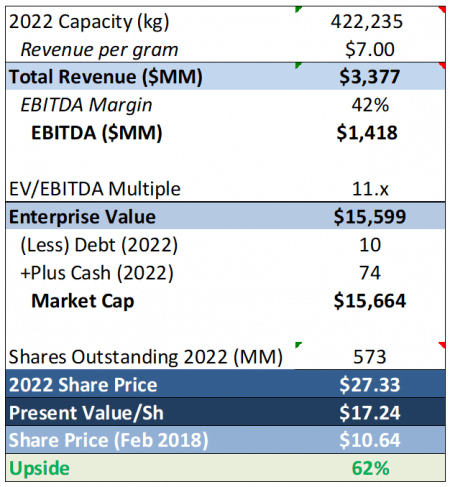

UPSIDE CASE (5% probability)

The upside case looks at what the stock is worth if absolutely everything goes right. Under this scenario, we assume Canadian supply is only adequate to meet growing demand and producers are able to maintain prices through successful branding, new product R&D, and other means. The stocks trade in line with global tobacco producers, who have significant pricing power and concentrated market share.

$7/gram retail on flower and $9.80/gram on extracts, 42% EBITDA margins, capacity in line with management guidance and an 11x EV/EBITDA multiple.

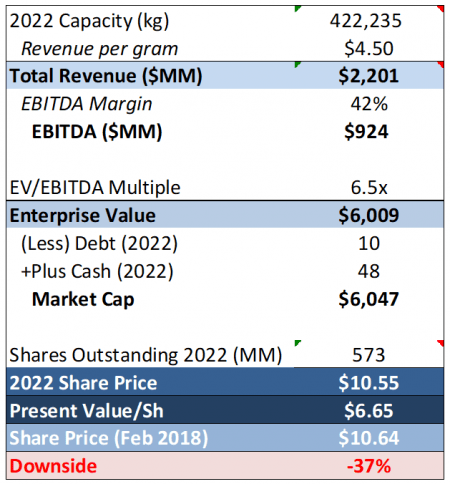

BASE CASE (60% probability)

Canada is flooded with new legal supply and a lack of barriers to entry causes higher cost producers to go out of business, balancing supply with demand. New sources of supply abroad shut down any opportunity to export excess marijuana produced in Canada. The stocks still manage to maintain margins in line with global tobacco producers through innovation and lower production costs. Stocks trade at the high end of commodity multiples.

$4.50/gram for flower, $6.30/gram for extracts, 42% EBITDA margins, capacity in line with management guidance and a 6.5x EV/EBITDA multiple.

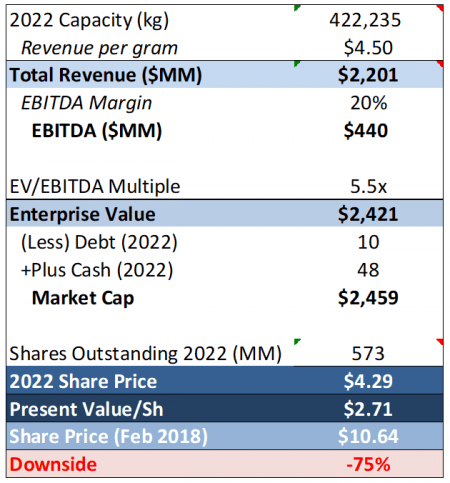

DOWNSIDE CASE (35% probability)

Canada is flooded with new legal supply and a lack of barriers to entry causes higher cost producers to go out of business, balancing supply with demand. New sources of supply abroad shut down any opportunity to export excess marijuana produced in Canada. Government control over distribution and retail and inflexible excise taxes lead to smaller margins for the producers as prices fall. Stocks trade at the midpoint of commodity multiples.

$4.50/gram for flower, $6.30/gram for extracts, 20% EBITDA margins, capacity in line with management guidance and a 5.5x EV/EBITDA multiple.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.