CAPACITY BY PROVINCE IN 2022

CANOPY GROWTH CORP.

Ticker: WEED (TSX)

Stock Price (Feb 2018): $26.31

Grizzle’s Future Target Price: $15.00

Current Annual Capacity: 35,000 kg

Future Annual Capacity: 440,000 kg

Canopy Growth is the big boy in the marijuana space. By 2022 it will be the largest producer of marijuana in Canada and potentially the world. Canopy has a well-developed medical and online distribution channel with its Tweed Main Street and Spectrum brands garnering high consumer awareness. Management is aggressively pursuing international supply deals and joint ventures to take advantage of Canada’s first mover advantage in the legal supply of marijuana.

What is the Canapocalypse?

The wave of marijuana supply is coming. Hundreds of greenhouses are being built across Canada and as harvests begin to flood the market in 2019, the Canapocalypse (aka price collapse) will soon be upon us. Retail prices are going much much lower unless legal producers find other countries to absorb the excess supply.

In this 4-part series we take you through a full analysis of the 4 largest legal producers, explain what assets they own, the potential export opportunities, future growth potential and what the stocks are worth. After reading our report, you will be better able to navigate this exciting, but risky emerging industry.

For some background reading on the coming Canapocalypse, check out Up in Smoke, our deep dive report of the Canadian marijuana sector as well as The Marijuana Export Mirage, an in-depth analysis into global supply and demand of marijuana.

Management Team

Bruce Linton – Chairman and CEO

Bruce Linton is the founder of Canopy Growth Corporation (CGC) and co-founder of Tweed Marijuana Inc. He is still the CEO of communications company Martello Technologies, a firm that provides voice call analytics services for companies that use Mitel voice communications. His background is in telecommunications and computer retail. Linton graduated with a bachelors degree from Carlton University.

Tim Saunders – Senior Vice President and Chief Financial Officer

Tim Saunders joined Canopy Growth in summer 2015 after gaining executive and leadership experience across a number of sectors, including mobile, telecom, semiconductors, manufacturing, and cleantech. Saunders has some solid contact in the export office of the Canadian government, which has helped Canopy become a leader in marijuana exports. He has earned his CPA, CA with PricewaterhouseCoopers and is a graduate of Bishop’s University where he obtained his BBA.

David Bigioni – Chief Marketing Officer

David Bigioni joined Canopy Growth in August 2017 to lead the company’s brand strategy. He previously led marketing and sales at Molson Coors and also led marketing campaigns for Unilever and TD Bank. Bigioni graduated from Wilfrid Laurier University with a BBA in business, management, and marketing.

Domestic Expansion

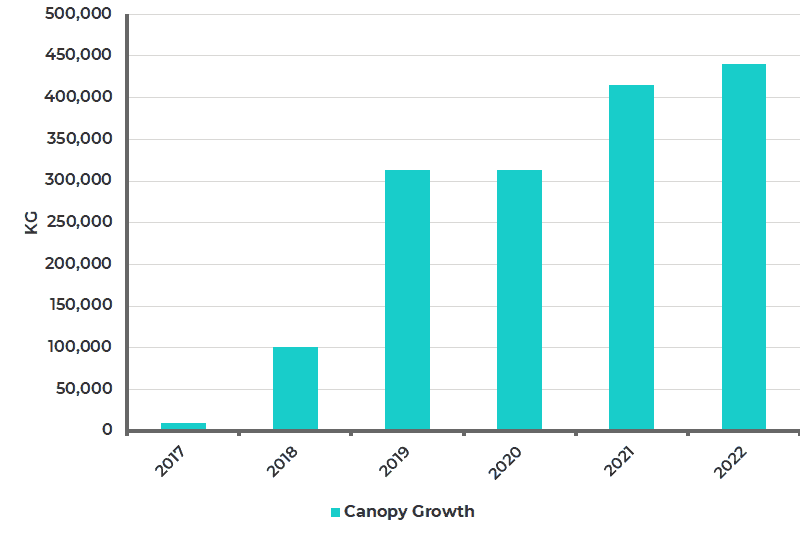

Canopy has the most aggressive growth outlook in the legal marijuana industry. Canopy harvested 32,000 kg of marijuana on an annualized basis in the fourth quarter of 2017 and says they have capacity to produce 35,000 kg today. Longer term, based on total potential square footage of 5.6 million sq ft in Canada (assuming 90% is for greenhouse space with the rest for processing, shipping and personnel), Canopy greenhouses could be producing as much as 508,000 kg (400,000 kg net) of domestic flower per year (50% of long term demand in Canada).

Canada Greenhouse Capacity

Time to Ramp Up

The most important question is how quickly new capacity can come online. Let’s use competitor Aurora’s ‘Aurora Sky’ facility as a benchmark for construction time, as it is the largest single greenhouse in construction. Aurora Sky began construction around October 30 2016 and the full 100,000 kg a year of capacity is scheduled to be operational by June 2019, for a 32-month total construction schedule. If we apply this timeline to the 4 large greenhouses being built by Canopy, capacity expansion should follow the timeline below.

Major Greenhouses

Tweed Farms

1 million sq ft total with 458,000 sq ft currently being converted to a marijuana greenhouse and an additional 212,000 sq ft being built from scratch, in addition to current capacity of 350,000 sq ft. First harvest from the new facilities will likely be in early June 2018, but full utilization of the 1 million sq/ft won’t commence until late 2018.

Vert Cannabis QC

700,000 sq ft total, with a retrofit of the existing greenhouse beginning in January 2018. First harvest will be in June or July 2018 most likely with capacity fully utilized by the end of 2018. Canopy owns 67% of the JV.

Tweed BC JV #1

Deal announced October 11 2017. First harvest expected by July 2018. Assuming the facility is completed and planted 25% at a time, the full 100,000 kg of capacity should be ready by March 2019. Canopy owns 67% of the JV.

Tweed BC JV #2

The option to build this facility has not even been exercised yet. Construction will likely follow the Tweed BC #1 facility. Assumed groundbreaking in April 2019 points to a full capacity up and running near the end of 2020, early 2021. Canopy owns 67% of the JV.

Canopy Growth Capacity by Year

International Expansion

Management is aggressively diversifying the business by signing many different types of deals with overseas cannabis companies, but the volumes of these deals are not huge compared to the growth expected out of Canada. Global expansion (Denmark, Australia and Jamaica) will add up to 45,000 kg at most, equal to 10% growth on domestic volumes.

Germany

Subsidiary Spektrum Cannabis GmbH signed a seed license deal with Alcaliber of Spain. Alcaliber pays Canopy a license fee to use its seeds so they can grow and sell their own marijuana supply. This deal does not increase demand for Canopy’s domestically grown marijuana.

Australia

Signed a supply agreement with AusCann Group Holdings of Australia (Canopy owns 11%) to be AusCann’s exclusive supplier of marijuana for the Australian medical market.

Auscann was granted a license to grow domestic marijuana in May 2017, so will eventually move away from foreign supply deals. This deal will not provide a long-term source of foreign demand for Canadian-grown marijuana.

Canopy may buy out AusCann in the future, which would give them a significant presence as a domestic supplier in the Australian market, but with the government indicating it wants to foster a competitive domestic market, Canopy will have to compete with other producers just like in Canada.

If medical patients in Australia grow to be 1% of the population, in line with our expectations for Canada, Australia will need 37,000 kg a year of supply. Even if Canopy buys out AusCann and captures 30% of the market, it would only equal 3% growth on top of their 2022 capacity target of 440,000 kg.

Denmark

Canopy created Spektrum Denmark by forming a JV with Danish Cannabis ApS. Canopy owns 62% and is in the process of building a 430,000 sq ft greenhouse to supply about 51,000 kg per year to the European market. Production from Denmark will contribute at most 12% growth to Canopy’s volumes.

Jamaica

Canopy created Tweed JA to supply the Jamaican marijuana market. Canopy owns 49% of the JV. The Jamaican market needs 9,000 kg or less and with 57 approved growers and 209 waiting for application approval, the capacity of Tweed JA should add no more than 3-5% to overall growth.

International Growth May Disappoint

Throughout history, when governments or companies want to gain corporate knowledge from competitors the easiest way to do so is to form a joint venture or consulting arrangement and then terminate the relationship once you have absorbed all the intellectual property of the other party. China has basically institutionalized this strategy of knowledge transfer.

Canopy looks to be going down a very similar path, signing joint venture agreements instead of setting up wholly-owned production facilities and transferring their growing techniques, strains and seed varieties to potential future competitors in exchange for a licensing fee. We worry that long term, meaningful international demand for Canadian marijuana may not materialize to the extent expected by the market.

AS IT STANDS TODAY, INTERNATIONAL OPPORTUNITIES WILL ONLY ADD 10% GROWTH TO CANOPY’S OVERALL GLOBAL VOLUMES. NOT THE EXPLOSIVE GROWTH INVESTORS ARE CURRENTLY ANTICIPATING.

Canopy Growth Stock Valuation

To value Canopy we look at the steady state cashflow potential of the business, which for our purposes is 2022 when the Canadian market for flower will be largely mature. We then apply a steady state Enterprise Value (EV) to EBITDA multiple to arrive at the future value of the company. Taking the future value and discounting it back to today gives us the present value of Canopy shares.

Enterprise Value (EV)

The value of the entire company taking into account any debt outstanding and cash in the bank. Calculated as the total value of stock outstanding plus the value of debt minus cash in the bank.

EBITDA

Earnings before interest on debt, taxes and depreciation. Similar to the cashflow of the business.

Present Value

To the average person a dollar in your pocket today is worth more to you than a dollar in your pocket one year from now. Therefore the future, higher value of a company needs to be adjusted back to its present value to see what it is worth to us TODAY.

USING A PROBABILITY WEIGHTED AVERAGE OF OUR UPSIDE, DOWNSIDE AND BASE CASE SCENARIOS, THE VALUE OF CANOPY TODAY IS $15.00/SH.

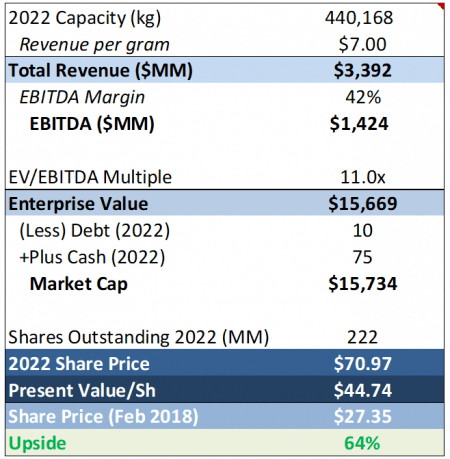

UPSIDE CASE (5% probability)

The upside case looks at what the stock is worth if absolutely everything goes right. Under this scenario, we assume Canadian supply is only adequate to meet growing demand and producers are able to maintain prices through successful branding, new product R&D and other means. The stocks trade in line with global tobacco producers, who have significant pricing power and concentrated market share.

$7/gram retail price, 42% EBITDA margins, capacity in line with management guidance and an 11x EV/EBITDA multiple.

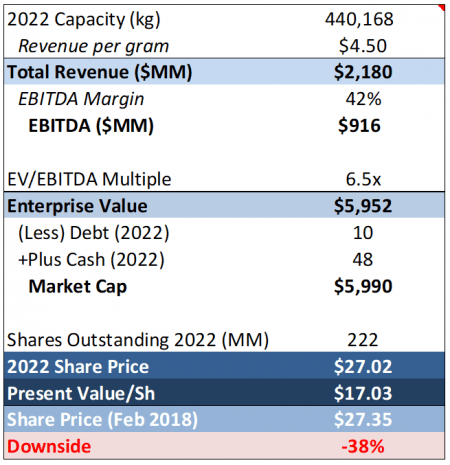

BASE CASE (60% probability)

Canada is flooded with new legal supply and a lack of barriers to entry causes higher cost producers to go out of business, balancing supply with demand. The stocks still manage to maintain margins in line with global tobacco producers through innovation and lower production costs. Stocks trade at the high end of commodity multiples.

$4.50/gram retail prices, 42% EBITDA margins, capacity in line with management guidance and a 6.5x EV/EBITDA multiple.

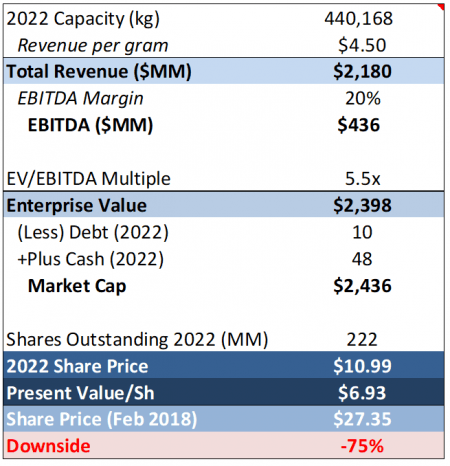

DOWNSIDE CASE (35% probability)

Canada is flooded with new legal supply and a lack of barriers to entry causes higher cost producers to go out of business, balancing supply with demand. Government control over distribution and retail and inflexible excise taxes lead to smaller margins for the producers as prices fall. Stocks trade at the midpoint of commodity multiples.

$4.50/gram retail price, 20% EBITDA margins, capacity in line with management guidance and a 5.5x EV/EBITDA multiple.

Read Up in Smoke – In this deep dive macro analysis of the Canadian marijuana sector, Grizzle lays bare all the inconvenient truths of this highly overvalued sector.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.