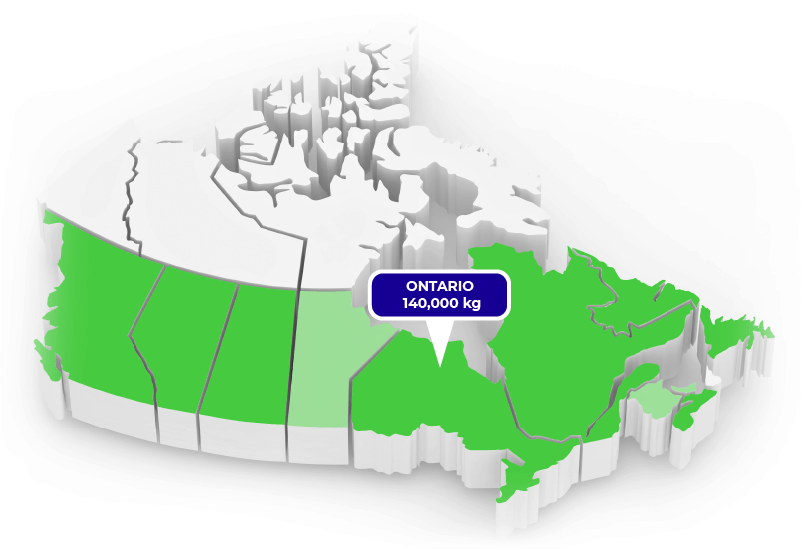

CAPACITY BY PROVINCE IN 2022

MEDRELEAF CORP

Ticker: LEAF (TSX)

Stock Price (Feb 2018): $20.50

Grizzle’s Future Target Price: $10.00

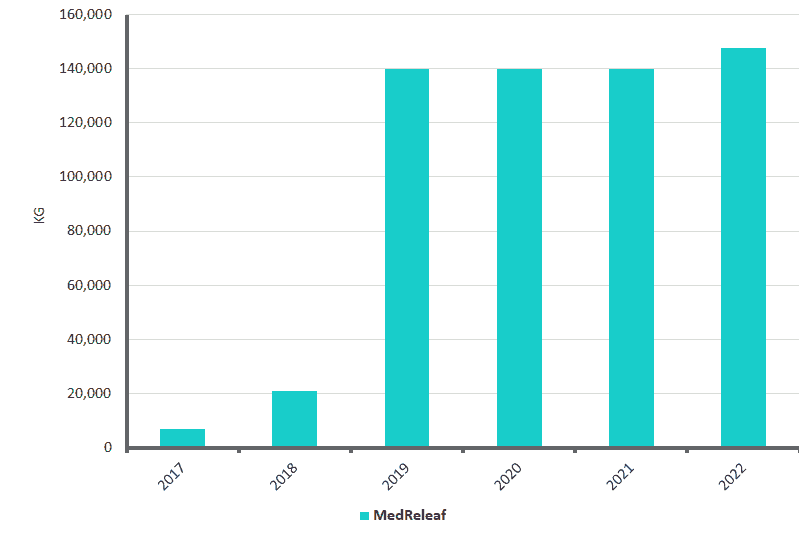

Current Annual Capacity: 16,500 kg

Future Annual Capacity: 154,200 kg

MedReleaf Corp, headquartered in Ontario, will be the fourth largest legal producer in Canada by 2022. MedReleaf is carving out a premium niche for itself with 35,000 kg of future indoor hydroponic grown marijuana capacity.

A recent deal to buy a traditional produce greenhouse will add 105,000 kg of supply by early 2019. By 2022 MedReleaf will be producing 140,000 kg a year in Canada (14% of Canadian demand). Potential greenhouses in Australia and Germany could add another 14,000 kg by 2022.

MedReleaf currently commands the highest retail price in Canada for their premium dried flower and oil extracts ($8.98/gram) and has a dedicated medical consumer base. MedReleaf will be the company to watch to judge the industry’s ability to maintain retail prices in the face of a significant oversupply of dried flower scheduled to hit the market starting in 2019.

We don’t believe stringent safety standards and high consumer popularity will be enough to halt the eventual slide of retail prices for every type of marijuana product.

What is the Canapocalypse?

The wave of marijuana supply is coming. Hundreds of greenhouses are being built across Canada and as harvests begin to flood the market in 2019, the Canapocalypse (aka price collapse) will soon be upon us. Retail prices are going much much lower unless legal producers find other countries to absorb the excess supply.

In this 4-part series we take you through a full analysis of the 4 largest legal producers, explain what assets they own, the potential export opportunities, future growth potential and what the stocks are worth. After reading our report, you will be better able to navigate this exciting, but risky emerging industry.

For some background reading on the coming Canapocalypse, check out Up in Smoke, our deep dive report of the Canadian marijuana sector as well as The Marijuana Export Mirage, an in-depth analysis into global supply and demand of marijuana.

MANAGEMENT TEAM

Neil Closner – CEO

Neil Closner was previously the head of business development for Mount Sinai hospital in Toronto before he became the CEO of MedReleaf. Prior to that he had spent a number of years in investment banking, private equity and as a strategic adviser to corporations. He also was the CEO of a baby-focused retail company which was eventually sold to Toys “R” Us.

Donald Courtney – Chief Operating Officer

Donald Courtney has many years of solid experience running the Canadian operations of an assorted list of global consumer goods companies. He ran operations for LG Electronics and Constellation Brands among others. He graduated from Saint Lawrence College with a degree in engineering and went on to take a number of courses in supply chain management over his career. Courtney’s past experience will directly benefit MedReleaf as it seeks to bring down manufacturing costs and establish an industry-leading supply chain.

Eitan Popper – President and Co-Founder

Eitan Popper is a founder of MedReleaf and has extensive international business experience. Prior to MedReleaf he was an investment principal for a Middle East and Africa investment network. Before that he worked for an Israeli infrastructure investment and management firm. Popper will likely be an asset to MedReleaf as they attempt to establish global greenhouses and a distribution network. He graduated from Universidad Iberoamericana in Mexico for his undergrad and received an MBA from Tel Aviv University and a Masters in fluid mechanics from Stanford.

Domestic Expansion

MedReleaf sales are 5,000 kg today with total production capacity of 16,500 kg. Including the recent acquisition of a 100,000 sq ft greenhouse in Ontario, MedReleaf will have 140,000 kg of capacity constructed and ready to go by early 2019. If MedReleaf wants to grow capacity beyond 140,000 kg they will have to do another large equity raise, which we do not include in our forecasts.

Major Greenhouses

Markham Ontario Facility

The Markham facility has 7,000 kg of capacity and was fully operational in 2017. The facility uses indoor hydroponic growing techniques and has the highest yields in the industry at more than 300 grams per sq ft, compared to an industry average of 120 grams per sq ft for a normal covered greenhouse.

Bradford Ontario Facility

The Bradford facility just completed an additional expansion and capacity is now 9,500 kg. The final expansion phase is expected to finish by late summer 2018, increasing capacity to 28,000 kg. This facility is also indoor hydroponics and has an industry-leading yield.

Exeter Ontario Facility

MedReleaf purchased a fully constructed greenhouse in February with capacity of 105,000 kg per year once fully retrofitted. An adjacent plot of 95 acres was also purchased and can support another 150,000 kg greenhouse if management decides to raise more money and expand in later years. The Exeter facility is a traditional enclosed greenhouse and has yields more in line with the industry at 120 grams per sq ft.

MEDRELEAF GROWTH CAPACITY BY YEAR

International Expansion

MedReleaf is in the process of expanding overseas, but looks to be behind peers, judging by the firm capacity of deals signed so far and the number of countries they operate in. In the following analysis we have only included international deals that increase MedReleaf’s capacity abroad or increase demand for exports of Canadian grown marijuana. Distribution deals are excluded because they will not help alleviate the coming marijuana oversupply in Canada or contribute to growth in capacity.

Germany

MedReleaf through its subsidiary MedReleaf Germany GmbH is in the running for a government tender to grow 6,600 kg domestically to supply the German market in 2022. We assume they win this tender and build a greenhouse in Germany to supply the local market.

Australia

MedReleaf owns 10% of Indica Industries Pty., a licensed medical marijuana producer in Australia. Australian demand for medical marijuana could reach 38,000 kg a year longer term, but even if MedReleaf buys out the other 90% of Indica it doesn’t own and captures 20% of the market, Australia would only add 6% to total volumes.

International Growth May Disappoint

Throughout history, when governments or companies want to gain corporate knowledge from competitors the easiest way to do so is to form a joint venture or consulting arrangement and then terminate the relationship once you have absorbed all the intellectual property of the other party. China has basically institutionalized this strategy of knowledge transfer.

MedReleaf is insulating itself from these risks through its direct ownership of international subsidiaries, which is a positive compared to larger peers. Keeping seed strains, growing techniques and other corporate knowledge in-house will increase MedReleaf’s ability to differentiate its product in international markets.

Risks remain with international governments committing to cultivate domestic sources of supply and international producers publicly stating a desire to import marijuana only until domestic production can be built. We worry that long term, meaningful international demand for Canadian marijuana may not materialize to the extent expected by the market, leading to much lower retail prices in Canada.

MEDRELEAF’S INTERNATIONAL PRODUCTION CAPACITY WILL ONLY BE 14,200 KG IN THREE YEARS (11% GROWTH ON TOTAL VOLUMES). NOT THE EXPLOSIVE GROWTH INVESTORS ARE CURRENTLY ANTICIPATING.

Valuation

To value MedReleaf we look at the steady state cashflow potential of the business, which for our purposes is 2022 when the Canadian market for flower will be largely mature. We then apply a steady state Enterprise Value (EV) to EBITDA multiple to arrive at the future value of the company. Taking the future value and discounting it back to today gives us the present value of MedReleaf shares.

Enterprise Value (EV)

The value of the entire company taking into account any debt outstanding and cash in the bank. Calculated as the total value of stock outstanding plus the value of debt minus cash in the bank.

EBITDA

Earnings before interest on debt, taxes and depreciation. Similar to the cashflow of the business.

Present Value

To the average person a dollar in your pocket today is worth more to you than a dollar in your pocket one year from now. Therefore the future, higher value of a company needs to be adjusted back to its present value to see what it is worth to us TODAY.

USING A PROBABILITY WEIGHTED AVERAGE OF OUR UPSIDE, DOWNSIDE AND BASE CASE SCENARIOS, THE VALUE OF MEDRELEAF TODAY IS $10.00/sh.

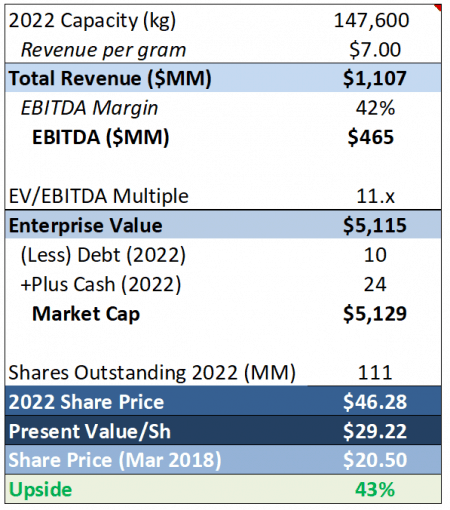

UPSIDE CASE (5% probability)

The upside case looks at what the stock is worth if absolutely everything goes right. Under this scenario, we assume Canadian supply is only adequate to meet growing demand and producers are able to maintain prices through successful branding, new product R&D and other means. The stocks trade in line with global tobacco producers, who have significant pricing power and concentrated market share.

$7/gram retail price, 42% EBITDA margins, capacity in line with management guidance and an 11x EV/EBITDA multiple.

BASE CASE (60% probability)

Canada is flooded with new legal supply and a lack of barriers to entry causes higher cost producers to go out of business, balancing supply with demand. The stocks still manage to maintain margins in line with global tobacco producers through innovation and lower production costs. Stocks trade at the high end of commodity multiples.

$4.50/gram retail prices, 42% EBITDA margins, capacity in line with management guidance and a 6.5x EV/EBITDA multiple.

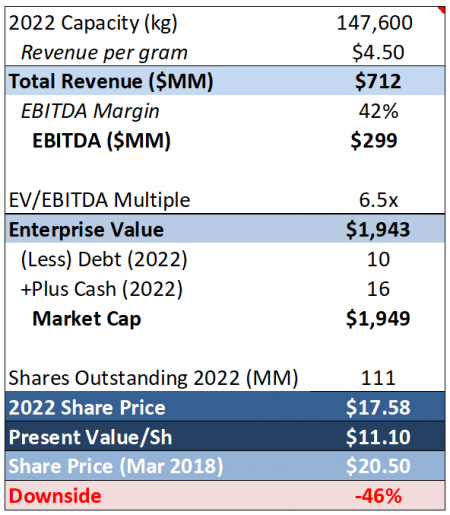

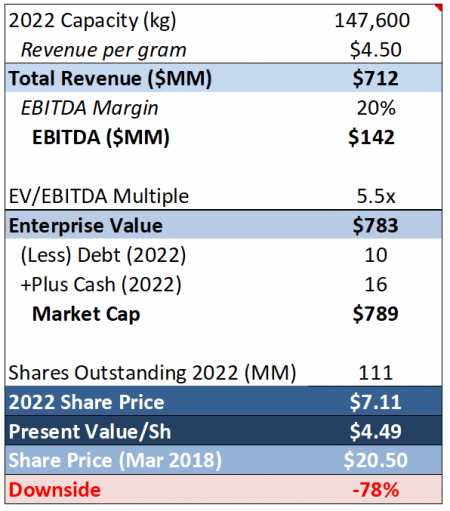

DOWNSIDE CASE (35% probability)

Canada is flooded with new legal supply and a lack of barriers to entry causes higher cost producers to go out of business, balancing supply with demand. New sources of supply abroad shut down any opportunity to export excess marijuana produced in Canada. Government control over distribution and retail and inflexible excise taxes lead to smaller margins for the producers as prices fall. Stocks trade at the midpoint of commodity multiples.

$4.50/gram retail price, 20% EBITDA margins, capacity in line with management guidance and a 5.5x EV/EBITDA multiple.

Read Up in Smoke – In this deep dive macro analysis of the Canadian marijuana sector, Grizzle lays bare all the inconvenient truths of this highly overvalued sector.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.