A new breed of cannabis company has recently emerged, quickly captivating the capital markets and drawing substantial attention from investors.

We are talking about cannabis extractors.

Put simply, extractors take cannabis flower and turn it into highly concentrated cannabis oil.

Investors have become enraptured at the revenue potential of these businesses.

The thinking goes, ‘think of how many new greenhouses are starting up in Canada and the U.S. right now, spurring massive potential demand for processing services due to consumers’ preference for oil-infused products such as vape pens, edibles, and drinks over smoking dried flower.’

The future of the extraction industry looks bright, but investors are putting their money at risk if they don’t fully understand the business model and both the risks and opportunities for these companies in 2019 and beyond.

In this guide, we explain the extraction business models, market opportunities and risk, plus explore if any of these stocks are well positioned to emerge as dominant players in the industry.

After reading our deep-dive you should be able to make an educated decision whether these stocks are ripe for investment or should be avoided.

Vertical Integration or Specialization

The Canadian cannabis market hasn’t yet determined if it will be a vertically integrated model similar to the U.S. or if the market will fragment into companies that specialize in each segment of the value chain.

In the agriculture industry, there is no precedent for publicly traded processing companies. Processing of corn, wheat, and soybeans is done privately through cooperatives or by individual farmers, telling us profit margins are thin.

In the crude oil market, large conglomerates were originally vertically integrated, handling the drilling, producing, refining, and retail sales all within a single company.

Over time the falling profit margins and earnings volatility of the refining business pushed these companies to spin out their refining arms into independent entities.

So far in cannabis, large licensed growers have signed small extraction agreements with third-party firms while building their own in-house extraction capacity at the same time.

The jury is still out on whether the cannabis industry goes full integration to start before specialization takes over like in the crude oil business.

If extraction companies want to keep all the capacity they’ve built fully utilized it is very important to convince the industry they possess special extraction knowledge and processes that can’t be replicated anywhere else.

The Different Cannabis Extraction Business Models

Even though cannabis extraction simply turns flower into oil, this process can be contractually set up in many different ways.

- Tolling – Extraction companies are paid a flat fee per gram to take a grower’s flower, turn it into oil and return the finished oil to the grower who will sell it into the market.

- Spot Market Sales – Extraction companies can go out and buy flower themselves, turn it into oil and sell the unlabeled oil on the wholesale market.

- White Labeling – Extraction companies buy flower, turn it into fully packaged consumer products which are then purchased by cannabis brands who slap their own label on the product and sell it to consumers.

- Retail – Extraction companies buy wholesale flower and turn it into retail-ready products with their own in-house branding. These products can be sold directly to government distributors or dispensaries.

Tolling

Pros: Extractors are guaranteed a fee per gram regardless of what happens to prices for dried flower or oil. There is no commodity risk. The only way the extractor gets into trouble is if the company they have a contract with defaults or goes bankrupt.

Cons: This is the lowest risk but lowest return business model. The extractor can’t take advantage of changes in flower and oil prices to increase margins. They also lose out on higher margins from white labeling.

Spot Market Sales

Pros: The company can take advantage of changes in the price of dry cannabis and oils to buy and sell at opportune times. If they time the market right, margins and profit will be higher than under a tolling agreement where the profit margin is fixed based on the contract.

Cons: Prices can be volatile so unless the company has some very smart people who really understand the market, they could make less than with a tolling agreement and in the worst case lose money. Profits will be very unpredictable and vary widely from year to year.

White Labeling

Pros: Through offering fully packaged value-added products, extractors can increase profits. They are providing an additional service to growers by not only turning flower into oil, but also packaging the oil so it can go directly onto store shelves after a label has been slapped on.

White labeling generates lower profits than spot market sales, but is a much less risky way to make money.

Cons: Labeling and packaging are more capital intensive than extraction alone and require more machines and investment up front.

Retail

Pros: This is the highest margin business model. Extractors capture the entire price difference between the retail price of a vape pen and the wholesale price of the dried flower that goes into making it, which can be substantial.

By creating in-house brands and selling direct to the consumer, extractors can build brand awareness and drive demand and higher margins for their products. They won’t be hurt if an extraction customer has trouble selling its own oil to customers and cancels or reduces future orders.

Cons: Competing directly with vertically integrated growers and standalone retailers could hurt business. A grower may not sign a white label or tolling agreement with an extractor who is directly competing with them on store shelves.

The Players

The four leaders in the extraction industry are MediPharm Labs (TSXV: LABS, OTCQX: MEDIF) ), Valens GroWorks (CSE: VGW), Neptune Wellness (CVE: NEPT) and Radient Technologies (CVE: RTI).

The companies are mainly differentiated by their management teams and capacity and have not yet developed proprietary extraction methods or significant intellectual property portfolios at this early stage, even though the companies will tell you otherwise.

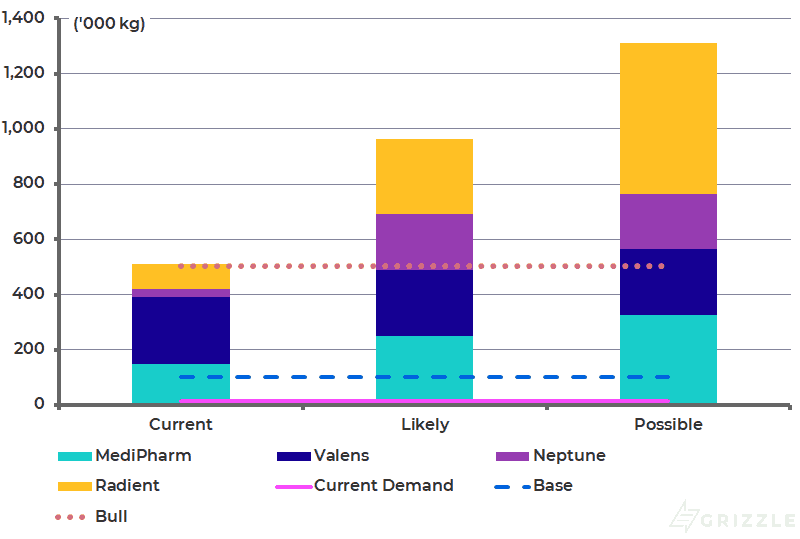

Current and Planned Capacity of Each Extraction Company

| 000′ Kilograms | Current | Likely | Possible |

| MediPharm Labs | 150 | 250 | 325 |

| Valens GroWorks | 240 | 240 | 240 |

| Neptune Wellness | 30 | 200 | 200 |

| Radient Technologies | 91 | 274 | 548 |

| Total Industry Capacity | 511 | 934 | 1,283 |

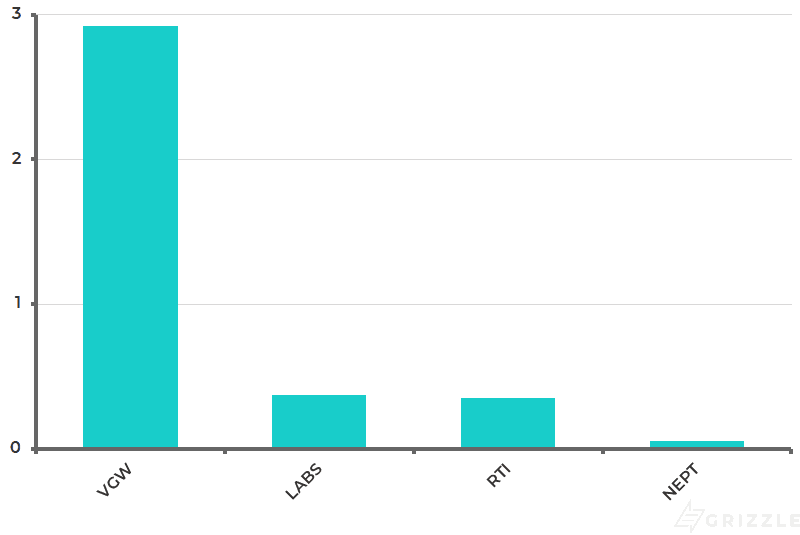

Cannabis Extraction Industry Cash Positions

Looking at the cash positions of the four large extraction companies we see a large spread in liquidity.

MediPharm is on the low end likely because the company is actually profitable on an EBITDA basis and has seen a cash infusion from warrants and options in the last two quarters to cover the liquidity gap.

The company is still burning about $5 million a quarter on new equipment and inventory, however, so will need to boost sales to break even on a cash flow basis or cut capital spending significantly in coming quarters.

Valens should turn a profit on an EBITDA basis next quarter and also has $62 million in cash, giving the company the longest liquidity runway.

Investors should expect another capital raise from companies with below a year of liquidity before their capital expenditures need to fall and the companies can operate sustainably.

Years of Cash Left at Current Burn Rate

The Opportunity for the Cannabis Extraction Industry

The extraction model is not a fad and is here to stay.

Similar to how the crude oil market functions today, standalone extractors will likely buy cannabis flower in bulk on the spot market and sell the oil wholesale or in packaged form to brands who will then put the product on store shelves.

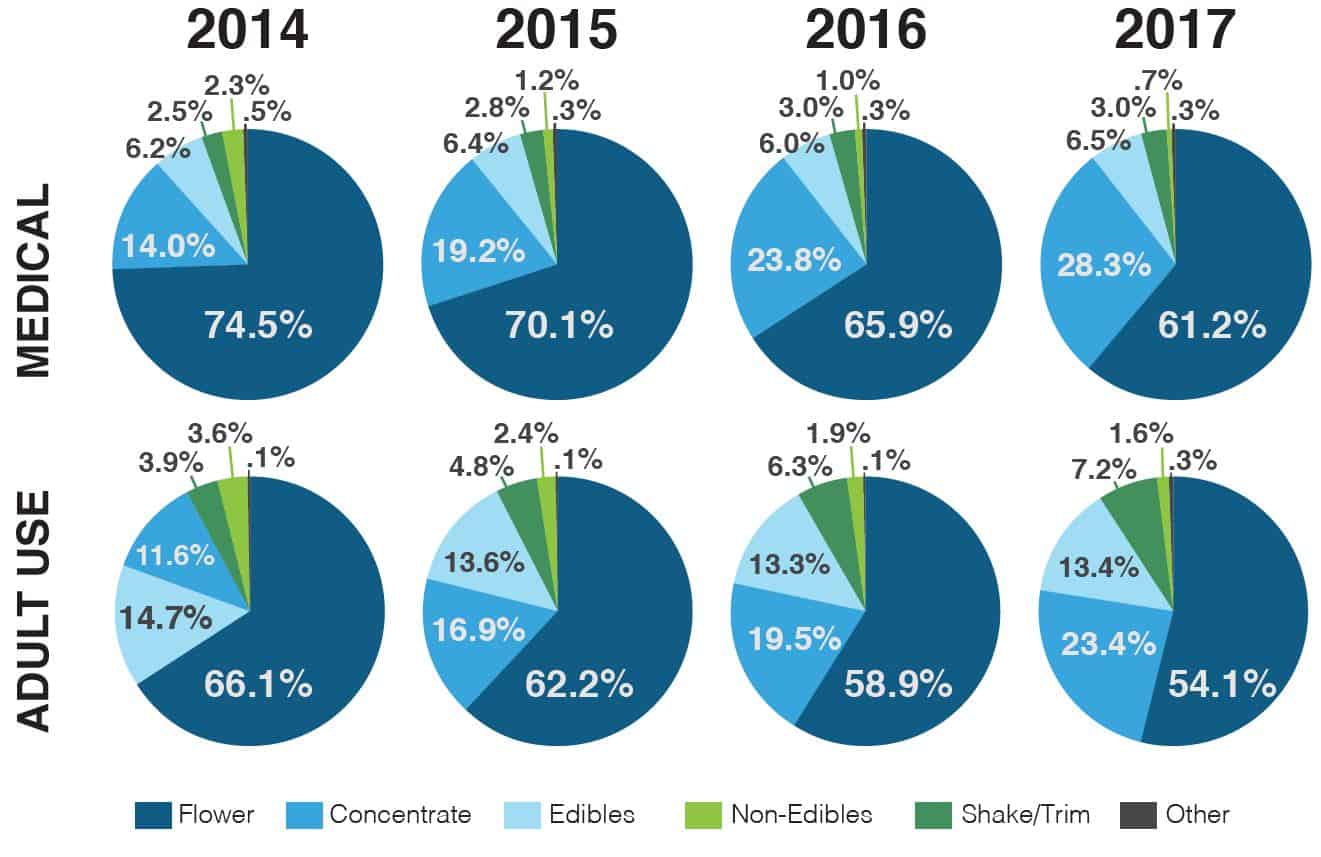

Canada alone produces 900,000 kg of cannabis so there will be significant demand for extraction capacity as consumer demand evolves past raw flower to oil infused products, similar to how legal U.S. markets have developed.

In U.S. legal markets, demand has rapidly evolved from smokable flower to oil-based products. Concentrates and edibles are more than 40% of demand in Colorado and 50% in California and growing.

Not to mention insatiable consumer demand for CBD, which will require millions of pounds of extracted hemp to satisfy.

Market Share Over Time by Product Format

At this early stage in the market’s development, most growers lack the experienced personnel and specialized knowledge to extract cannabis flower into oil, creating significant demand for third-party processing services.

As extraction companies refine their extraction techniques and build a proprietary library of oil formulations they could become indispensable partners to any grower of cannabis.

The Risks for the Cannabis Extraction Industry

There are a few big risks investors need to be aware of before they dive into owning extraction stocks.

It’s Cheap to Join the Game

Per gram of capacity, it is much cheaper to buy extraction equipment than it is to build a greenhouse and start growing.

For example, it costs $1.50-$3.00 per gram to build a cannabis greenhouse compared to $0.10-$0.30 cents per gram for extraction equipment.

This may explain how companies have managed to beef up capacity so quickly.

The cheap cost of entrance means we will see many more players enter the field in an attempt to take some of the juicy profits for themselves.

Extractors like MediPharm and Valens generated ~40% gross margins last quarter, which are twice as high as the best global oil refineries.

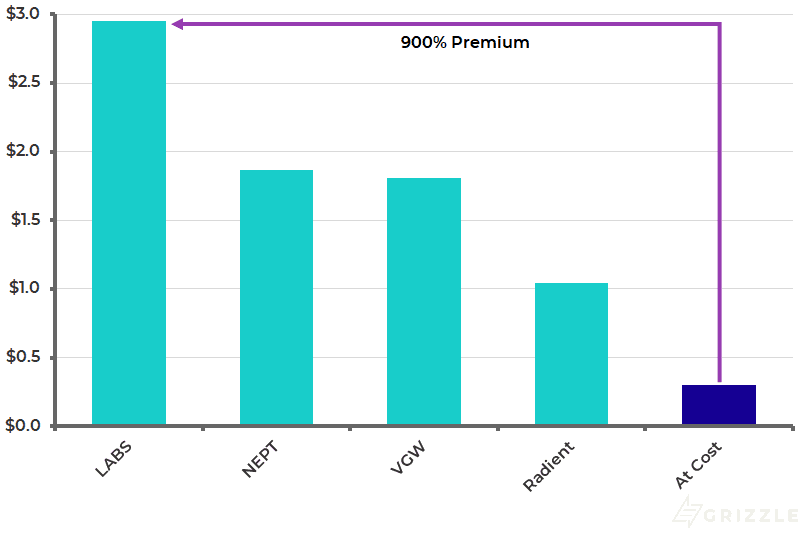

There is also a huge capital markets incentive to create an extraction company.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Public extraction companies trade for $1.92 per gram of capacity on average while it costs only $0.09-$0.30 per gram to buy equipment to start your own extraction company. Anyone with deep pockets could buy equipment for $0.30, go public and turn that $0.30 into $1.00-$3.00, for a rapid 300-900% gain.[/su_panel]If margins and public stock premiums stay where they are, new extraction companies will continually go public until the easy money can no longer be made.

Investors should be prepared for extraction margins and the market cap per gram to fall over time.

Public Market Value per Gram of Capacity

Cannabis Extractors Will Struggle to Fill All That Capacity

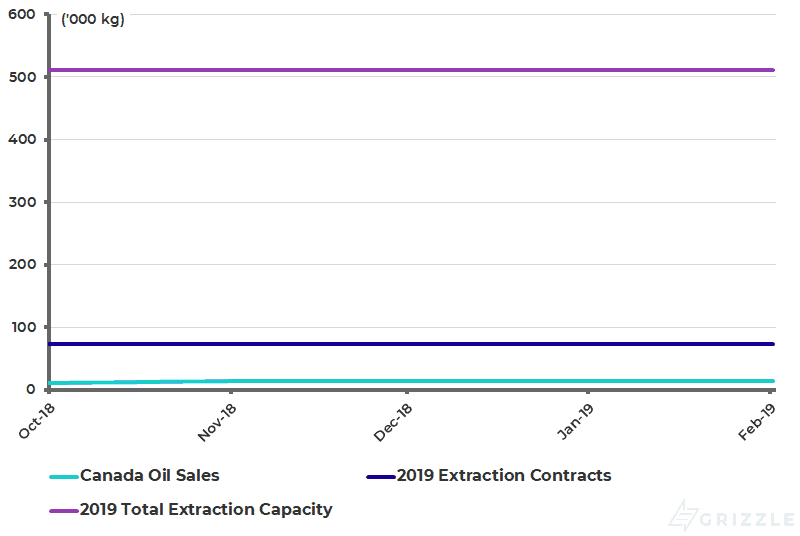

The legal market in Canada sells 100,000 kg of dry cannabis right now, with extracts making up only 13% of the market, far below the 500,000 kg of extraction capacity online from MediPharm, Valens, Neptune and Radient alone.

The 500,000 kg will grow to 1 million kg by 2020 and 1.5 million by 2021, not even counting capacity from private extraction companies and growers like Aphria with 200,000 kg of in-house capacity.

Ultimately, even under the most bullish cannabis oil demand scenario, extraction supply will far exceed demand.

Current Demand: In the last five months of legalization in Canada, oil demand has been running at an annual rate of only 13,000 kg dry equivalent.

Base Case: Oil demand is additive to flower demand and causes the legal cannabis market to double in 2020 to 200,000 kg per year. Oil sales make up 50% of legal cannabis sales or 100,000 kg, in line with demand trends in California, the most developed cannabis market in North America.

Bull Case: Demand for oil in vape pens and infused into edibles takes over 50% of the remaining black market plus 50% of the legal market.

The black market and legal market combined are estimated at 810,000 kg a year in 2018 according to Statistics Canada. We assume the market grows to 910,000 kg with oil making up 55% or 505,000 kg a year.

Current, Likely and Possible Processing Capacity

The above chart shows us that it will potentially be a challenge for extractors to find buyers for their capacity.

Cannabis extraction companies can’t rely on demand outside of Canada either. Sales to Europe from Canadian licensed producers (LPs) are running at less than 2,000 kg a year, requiring massive growth to make a dent.

Federal legalization in the U.S. is still two years away at least and with multi-state operators building their own oil extraction equipment or buying from already established U.S. extractors, it is doubtful U.S. companies will be contracting with Canadian extraction companies at scale anytime soon.

Looking at the capacity of announced binding contracts, Valens has contracts for only 19% of capacity in 2019 and 46% in 2020, while MediPharm has binding purchase agreements for only 18% and 7% of capacity in 2019 and 2020.

Putting even this lower amount of contracted capacity in perspective, the committed capacity just for Valens and MediPharm alone is 72,000 kg in 2019 which would require oil demand to grow 500% from the February run rate.

But What About CBD?

Some will make the argument that exploding CBD demand requires fields of hemp to satisfy consumers and they are technically right.

Canada harvested 135,000 acres of hemp in 2018 or 43 million kg of raw hemp. This dwarfs the 500,000 kg of public extraction capacity.

However, a kg of hemp yields only 18 grams of CBD, while a kg of cannabis yields 170 grams of THC, 10x more.

Economics are worse too, with wholesale CBD extract selling for $6.50 per gram compared to THC extract at $40/gram.

If extractors process hemp instead of cannabis their revenue potential would be significantly lower and they would wildly miss consensus estimates.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]The much lower revenue opportunity from hemp means that even if extractors are running full out producing CBD they will still miss revenue estimates. [/su_panel]Processing Hemp Doesn’t Pay Compared to Cannabis

| C$MM | Annual Capacity (kg) | Max Revenue from Cannabis | Max Revenue from Hemp |

| MediPharm | 250,000 | $771 | $15 |

| Valens | 240,000 | $288 | $14 |

| Neptune | 200,000 | $428 | $12 |

| Radient | 273,750 | $586 | $16 |

Source: Grizzle Estimates, SEDAR Filings, AG Canada

If the only thing MediPharm extracted was hemp the company would max out at $15 million of annual revenue, compared to consensus of $100-$300 million over the next three years.

Valens is similar, generating only $14 million of annual revenue from hemp compared to consensus revenue estimates of $52-$170 million.

Higher-yielding hemp strains are in the works, but the timing of when these strains will be planted and harvested is unknown at this point.

Analyst Estimates are Too High

The table below lays out consensus revenue and EBITDA estimates (a measure of cashflow) for Valens, Medipharm, and Neptune.

If consensus is right, there will be impressive growth for all the extraction stocks.

MediPharm and Valens, in particular, would see revenue growth of 180% and 500% in 2019 compared to 2018.

Cannabis Extraction Industry Consensus Estimates

| VGW | 2019 | 2020 | 2021 |

| Revenue | 52 | 125 | 171 |

| EBITDA | 23 | 63 | 84 |

| EBITDA Margin | 44% | 51% | 49% |

| LABS.V | 2019 | 2020 | 2021 |

| Revenue | 116 | 201 | 317 |

| EBITDA | 26 | 64 | 90 |

| EBITDA Margin | 22% | 32% | 28% |

| NEPT | 2019 | 2020 | 2021 |

| Revenue | 54 | 114 | 176 |

| EBITDA | 10 | 28 | 48 |

| EBITDA Margin | 19% | 25% | 27% |

As of May 1 2019; Source: S&P CapitalIQ, Altacorp Capital.

However, when we look at the capacity needed to hit these EBITDA and revenue numbers, these companies are almost assured to disappoint investors over the next 12-24 months.

Based on last quarter’s EBITDA margin of $0.12 per gram, Neptune needs to process 194,000 kg in 2019 and 211,000 kg in 2020.

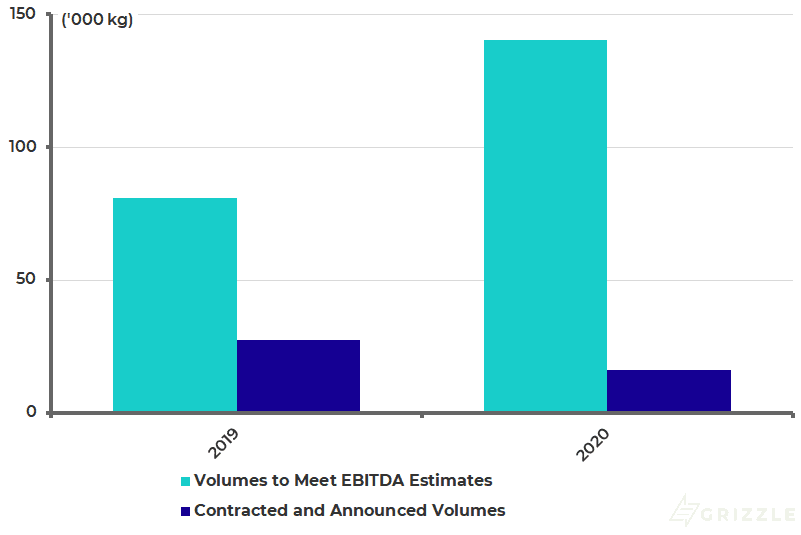

MediPharm has a better margin of $0.30 per gram but still needs to process 80,000 kg in 2019 and 140,000 kg in 2020 to meet estimates.

The problem for both companies is they’ve signed contracts for less than these amounts.

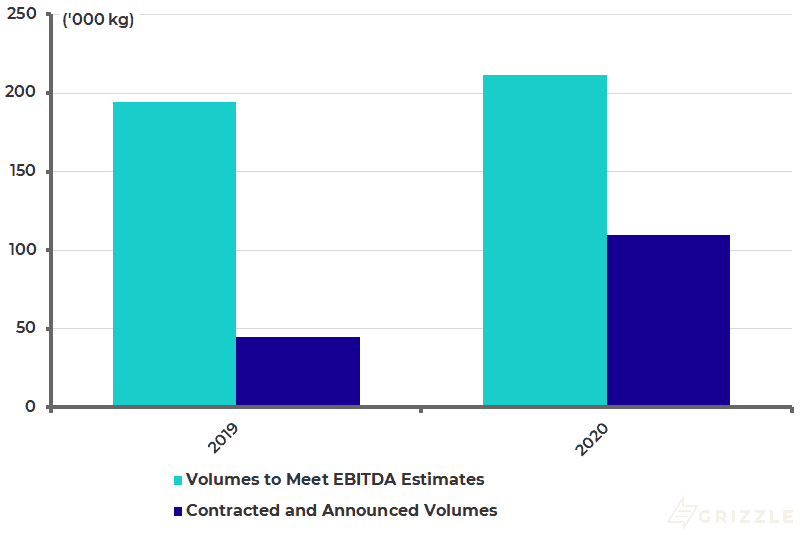

Valens only has contracts for 45,000 kg in 2019 and 110,000 kg in 2020 while MediPharm’s contracts are smaller at 27,500 kg and 16,000 kg respectively.

Both management teams need to sign more contracts soon or see consumer demand explode so they can fill the rest of their unused capacity through spot purchases and sales.

Valens Consensus vs Contracted Capacity

MediPharm Consensus vs Contracted Capacity

Even if these companies manage to sign additional contracts or buy wholesale flower to run at full capacity or close to it, the market just doesn’t need that much cannabis oil.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Consensus EBITDA estimates for Valens, MediPharm and Neptune alone add up to 330,000 kg of sales in 2019 and 560,000 kg in 2020 while cannabis oil demand is only running at 13,000 kg a year. This is a massive gap that will never be closed with the current restrictive regulations in effect.[/su_panel]Extraction Capacity is Far Above Stagnant Oil Demand

A Note on Contract Language

Even though capacity under contract is expected to be a sure thing, the language of the contracts between extraction companies and growers leaves much flexibility.

A sample agreement between a cannabis extractor and a licensed producer reads like this:

Few of the contracts have minimum volume commitments and most are non-binding with an option to use the processor not a contracted requirement. To take into account the potential upside for extractors, we include optional capacity as well as committed capacity in our analysis.

Share Unlock Details and Other Important Information

MediPharm Share Lockups

Founders, employees, insiders and seed shareholders owning ~40% of diluted shares are locked up under the following schedule:

- 25% released on the Listing date (Oct. 1, 2018)

- 25% 6 months after (April 1, 2019)

- 25% 12 months after (Oct. 1, 2019)

- 25% 18 months after (March 31, 2020)

Valens Share Lockups

Valens’ largest shareholder, Noreen Dale Spanell, disposed of 3.5 million shares out of the 15 million she beneficially owns (12% of common shares) on Jan. 30 and agreed to lockup her remaining shares for six months (July 30, 2019).

The buyers of the 3.5 million shares agreed to a 4-month lockup (May 30, 2019).

Neptune Legal Proceedings

A prior CEO of Neptune sued the company for $8.5 million of unpaid wages and additional stock. The first hearing dates are May and June 2019.

The same CEO is alleging remaining royalties from the krill extract business have not been paid and is seeking full payment. The court ruled in favour of the prior CEO at the end of March and Neptune now has to pay the CEO 1% of revenue from March 2014 to today. The amount has yet to be determined but should be at least $1.7 million.

So What Will Happen to Extraction Stocks in 2019?

Extraction stocks have been the cannabis sector darlings of 2019 so far with MediPharm, Valens, and Neptune up 214%, 153% and 51% respectively, handily beating the overall cannabis sector.

These cannabis extraction stocks could have more upside left in the short term if management teams announce new contract signings, but as we move through 2019, the companies will struggle to meet wildly optimistic consensus revenue and EBITDA estimates.

Given that the stocks have run and retail investors are all-in on this sector, we think there is more downside than upside as the companies disappoint earnings expectations quarter after quarter.

From a longer-term perspective, none of the extraction companies have proven they will become the licensed growers’ preferred providers of extraction services.

They have not built enough intellectual property and specialized processing know-how to demand much higher rates than what a licensed producer would spend processing cannabis in-house.

If a large licensed producer announces another in-house processing facility, it could throw cold water on the market’s expectation that independent extraction facilities will capture the majority of oil processing business as Canada rolls out edibles, infused beverages, and vape pens.

In the mature crude oil markets, refiners struggle to earn their cost of capital and the best refiner is only separated from the worst by the reliability of its assets.

Cannabis extraction companies will have to work to build proprietary extraction techniques and intellectual property to avoid the commoditized fate of their crude oil peers.

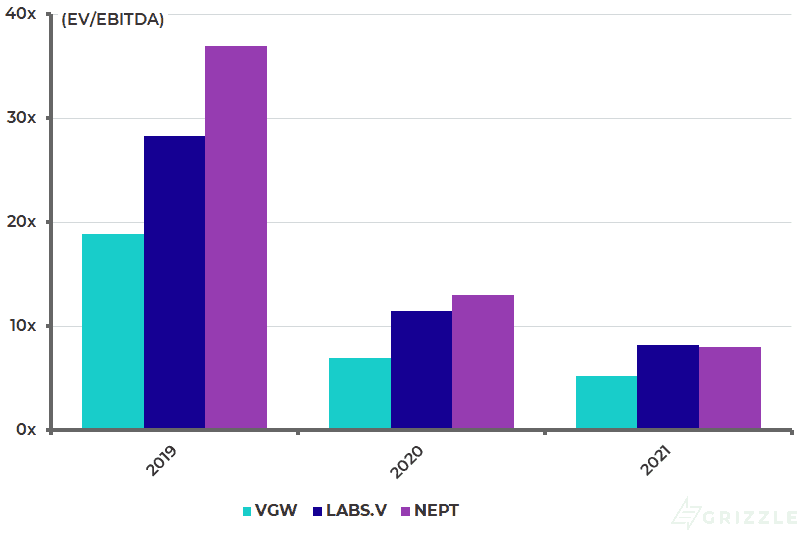

EV/EBITDA Estimates

| Consensus EV/EBITDA Multiple | 2019 | 2020 | 2021 |

| VGW | 18.9x | 6.9x | 5.2x |

| LABS | 28.3x | 11.5x | 8.2x |

| NEPT | 37.4x | 13.4x | 7.8x |

| Weighted Average | 27.9x | 10.7x | 7.2x |

| Licensed Producers | 37x | 19x | 11x |

| U.S. Multi-State Operators | 35x | 14x | Not available |

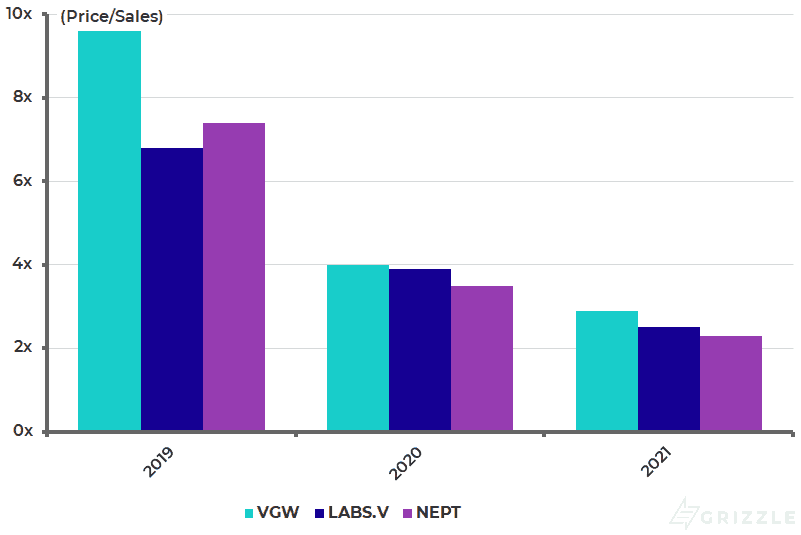

Price to Sales Estimates

| Consensus Price/Sales Multiple | 2019 | 2020 | 2021 |

| VGW | 9.6x | 4.0x | 2.9x |

| LABS | 6.8x | 3.9x | 2.5x |

| NEPT | 7.4x | 3.5x | 2.3x |

| Weighted Average | 7.7x | 3.8x | 2.5x |

| Licensed Producers | 11.0x | 6.0x | 3.0x |

| U.S. Multi-State Operators | 8.6x | 5.0x | Not available |

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.