The first time we met Bruce Linton, we left unimpressed.

The management team in place at Canopy never seemed like the calibre of people to carry the company, let alone the industry, to long-term success. They favoured promotion over operations.

Canopy was a company that worked well in the promo phase, driven by Linton promising the moon at every turn, but now with the market transitioning to a point where operations matter, Canopy is exposed.

With the co-CEOs both on their way out after the CFO was replaced in June, we question why Constellation (NYSE: STZ) gave billions to a management team whose entire vision they obviously U-turned on completely.

If Bruce was the problem he would have been the only one leaving, but it’s clear Constellation is signalling a plan to clean house and start fresh.

Investors have a problem.

They are stuck with a corporate investor running the show with no experience growing cannabis.

Not to mention we think there are likely skeletons in the closet Constellation has yet to uncover.

The best case for investors is a stock stuck as a market laggard with write-down risk hanging over the shares.

Worst case, future write-downs kill investor confidence, narrowing the huge multiple premium to the group.

Canopy stock has 30%-40% downside to it if the company trades towards the market multiple, $25 in the U.S. (NYSE: CGC) or C$32 (TSE: WEED) in Canada.

Investors should be very wary of holding a company that is likely looking at big write-downs in the very near future.

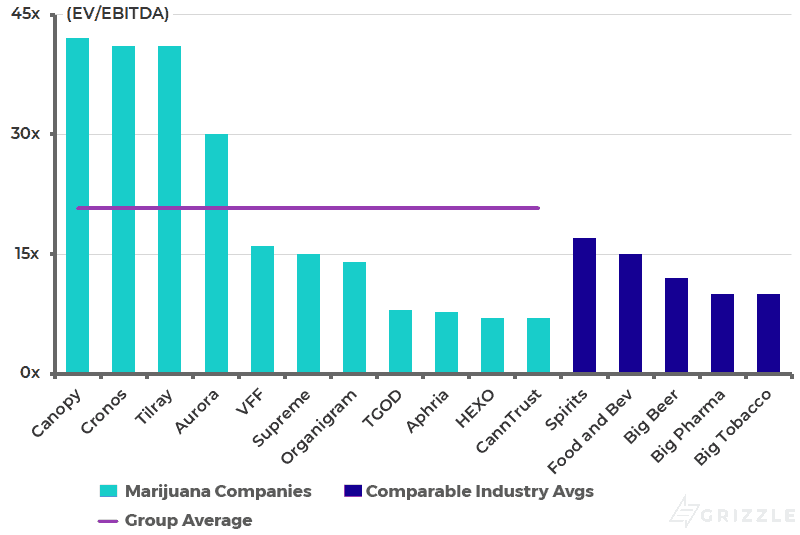

2020 Forecast EV/EBITDA

Write-downs Are Inevitable

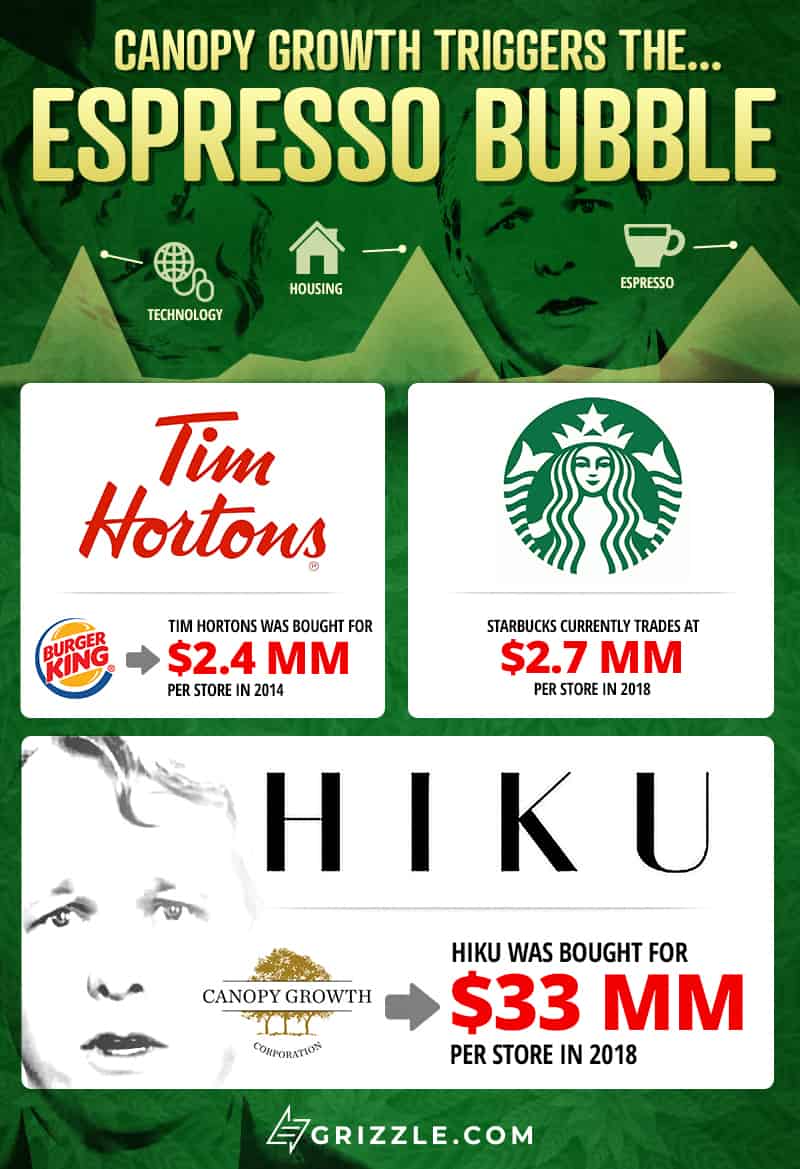

Highlighting only one of Linton’s many deals should make it obvious there is significant write-down risk in the Canopy portfolio.

Canopy paid C$270 million for Tokyo Smoke, a set of seven coffee shops. Goodwill and intangible assets made up more than 90% of the deal.

Given that Aphria wrote off C$50 million, or 25% of the purchase price of their entire LATAM portfolio, made up of much higher quality distribution assets, unique licenses, and greenhouses, we can almost guarantee some big Tokyo Smoke write-downs are coming.

Tokyo Smoke is just scratching the surface.

Canopy spent $1.6 billion in the last 12 months on acquisitions and is sitting with over $2 billion of goodwill and intangibles on the balance sheet, a full 50% of assets when you exclude the huge cash pile from Constellation.

With Linton’s track record of overpaying for assets that support the promotional story he wants to tell, we expect the new management team will be quick to write off legacy assets to make sure they have a low bar to jump over to please investors going forward.

What is a Cannabis Investor to Do?

As we’ve continually highlighted, there are only two places of legit opportunity in Canadian cannabis stocks: craft and organic. All one needs to do is see what strains and products are sold out to recognize where the real market demand is.

Would love for it to be 🍑’s for all #potstocks going forward, it ain’t

When the bellwether is a hot air ballon $CGC/ $WEED, it’s dicey AF. Fantasy cannabis is over, real #’s are gutter

Pricing power & moving units is all that matters. Right now that belongs to craft & organic

— Thomas George (@thomasg_grizzle) June 30, 2019

Yes, Canopy still has billions in the bank, but what does Constellation, now running the ship, know about growing high-quality cannabis?

Plain and simple Canopy management is having a real problem growing cannabis.

There is simply no market for Canopy’s low-quality schwag.

Canopy needs to purchase another producer that knows how to grow the cannabis consumers want at scale or poach a master grower who does.

It’s clear Canopy needs to reinvent itself to show the revenue growth investors demand and recapture its long-held crown as the king of legal cannabis.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.