Bottom Line:

Luckily for Canopy, this was largely a meaningless quarter, because if they put up results like this in 2019 we would be worried for Constellation Brands and for all stockholders.

We want to be clear this was a transition quarter for Canopy as they ramped up headcount and marketing to be ready for legalization.

They have a recreational market cost structure but no recreational sales yet so this is the worst earnings results we should see from the company.

Canopy is not out of the woods yet as management has a lot of work to do to convince investors it will continue to be a market leader in cannabis.

Based on this quarter’s gross margin and cost structure, Canopy will have to sell 108,000 kg a year to break even. They harvested 15,000 kg this quarter (60,000 kg annualized), but sold only 2,200 kg, so a long way to go.

Investors should look through this earnings release and focus on the next six months which will determine if Canopy will remain a stock market darling or become an industry laggard.

If Canopy is not on a path to positive earnings by March of next year investor should start looking for a new market leader.

Operational Review

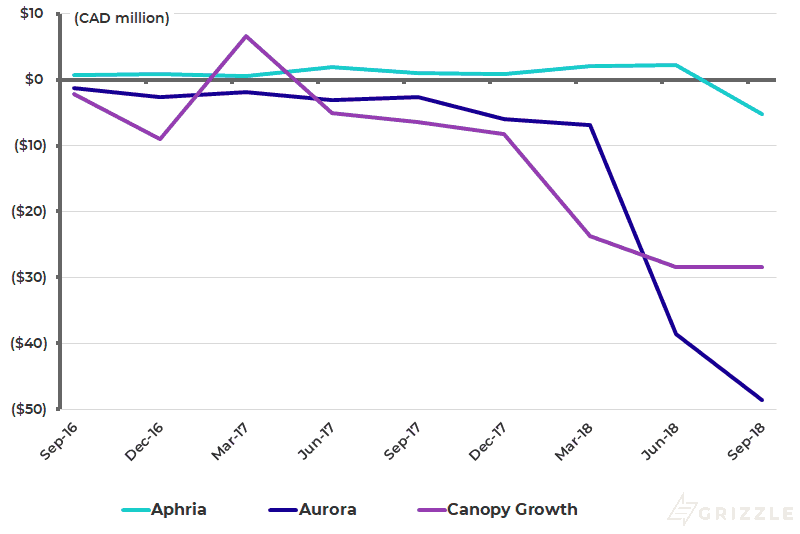

We track EBITDA for the three largest producers to see if they are turning the corner towards profitability.

Canopy continued to generate negative EBITDA this quarter but at least the deficit stopped growing, unlike Aurora Cannabis.

The EBITDA deficit should shrink for all three companies next quarter as they ramp up recreational sales and if it doesn’t investors should be worried.

Quarterly EBITDA by Company

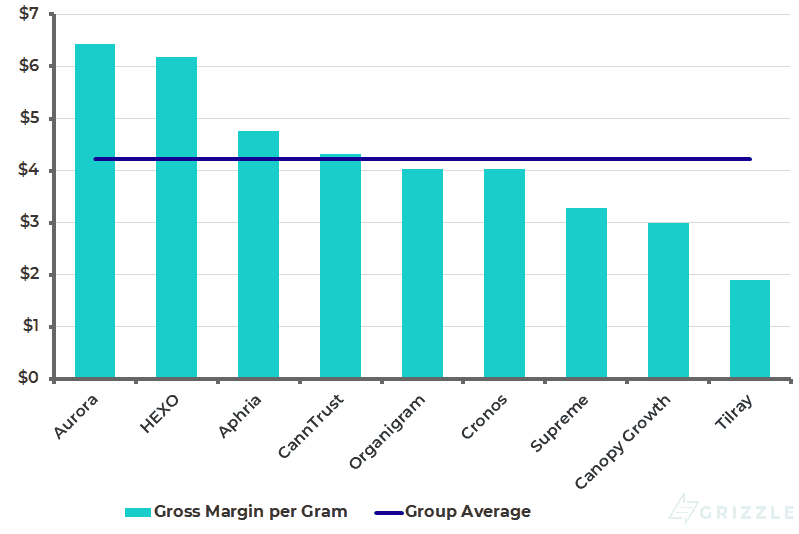

Canopy’s gross margin fell to $7 million from $11 million in the prior quarter, driven by production inefficiencies and the inclusion of depreciation into operating costs. Next quarter the gross margin should at least double as new facilities that are already included in costs begin to generate revenue.

Volumes declined as well, down 18%, making Canopy the only company to ship less product than the quarter before.

Falling medical sales may have been a conscious decision by the company to shift focus to building inventory for legalization. We will have to wait until next quarter to confirm this was an aberration.

Canopy now sports the lowest gross margin in the peer group, but this metric will look much better in the next two quarters as production ramps up faster than costs.

Gross Margin by Licensed Producer

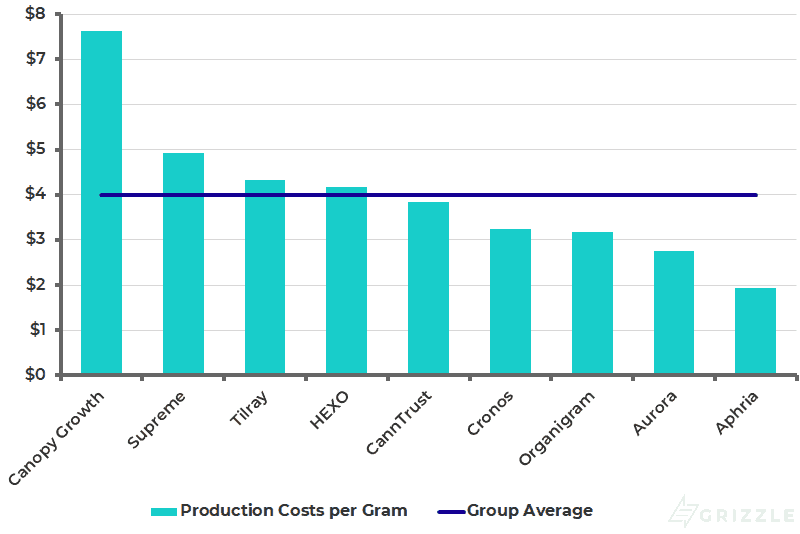

Production costs increased this quarter and are almost twice the industry average which is way too high.

We will need to see a significant improvement in the first two quarters of recreational sales or Canopy could see significant pressure on its stock price.

Production Costs per Gram

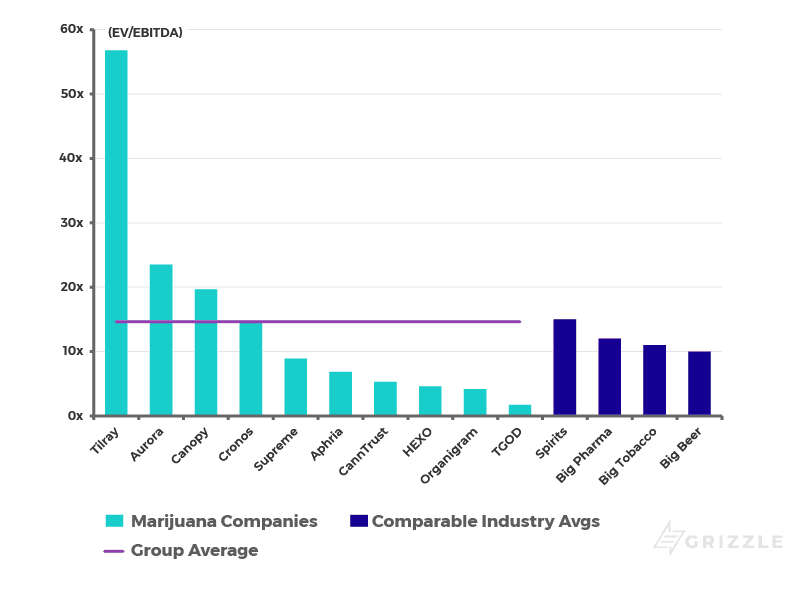

Valuation

The problem facing investors is they own a stock already pricing in good times ahead.

Investors are looking for hundreds of millions in EBITDA in 2019, a dominant market share in Canada and attractive product pricing.

It will be difficult for Canopy to deliver on all of those metrics without some hiccups along the way.

We recommend investors rotate into lower multiple names with less downside like Aphria, CannTrust or Supreme until Canopy proves to investors it deserves the title of industry bellwether.

EV/EBITDA in 2020

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.