Bottom Line

Canopy Growth (TSE: WEED) delivered a mixed earnings report, but the news of a majority investment by Constellation Brands will overshadow earnings and lead to significant stock outperformance for Canopy today and for the industry as a whole over the next few trading days.

Constellation Brands (NYSE: STZ) has effectively taken over Canopy and is the first big blue chip player to fully buy in to the cannabis story.

This deal puts a floor under Canopy stock with Constellation likely to buy out remaining shareholders if the stock price falls too far.

On the flip side it removes any M&A upside for Canopy investors, who should now think of this stock as a low risk but low return way to play the growth of the cannabis market.

Institutional investors and big players in tobacco, beer, soda, and spirits will all come calling in the months to come and they won’t be looking at Canopy.

With the upside removed from Canopy Growth we think a stock rotation is about to occur into other large producers who still could be bought out as the market matures.

We like Aphria (TSE: APH) for its low cost structure and reasonable multiple and Tilray (NASDAQ: TLRY) for its significant international distribution and R&D capabilities.

Earnings — What Went Right

Canopy Growth had another quarter of explosive growth — revenue was up 63% in the last 12 months.

Prices charged for oils and flower continue to increase and drove the overall revenue per gram to a new high of $8.94 per gram.

Even if we remove revenue from exports to Germany, selling prices were still up 8% quarter over quarter — a strong result.

Canopy harvested 9,685 kg in the quarter up significantly from 4,811 kg last quarter and is at an annual capacity of 40,000 kg a year.

The company is well positioned for legalization with supply agreements signed in the 5 largest provinces and retail stores under construction in the provinces that allow private retail opportunities.

Canopy has more than 23,000 kg of dry equivalent marijuana in storage ready for legal sales, which is likely already spoken for through provincial supply agreements.

Pricing in Germany is very strong at $13.62 per gram compared to $7.34 for flower in Canada, demonstrating the significant profit potential from supplying Europe, even though we do see risks to growth in the region.

A significant shortage looks to be inevitable in the early days of the legal market, benefiting the company through higher selling prices and market share.

Earnings — What Went Wrong

The cash burn increased with earnings before taxes, interest costs and depreciation (EBITDA) coming in at a loss of $47 million vs a $9 million loss this time last year.

$67 million of cash was spent on operations and $180 million on investments meaning the company is burning $250 million of cash a quarter.

With management no longer disclosing growing costs our focus turns to production costs per gram, which at $5.50 is the highest in the industry.

Provinces are rumoured to be negotiating $4.50 per gram or less wholesale prices, meaning Canopy will have to bring down costs dramatically to generate any profit.

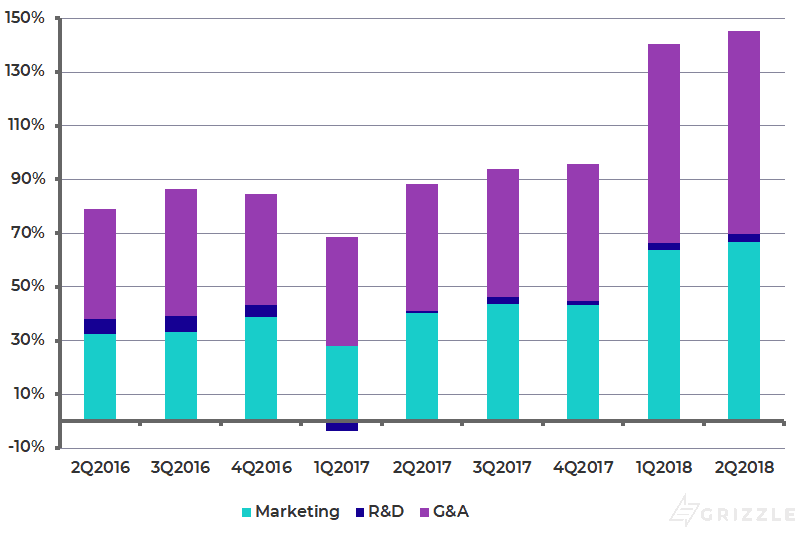

Overhead costs are also still going up as a percentage of revenue and with stock prices embedding 30% EBITDA margins in coming years, Canopy still is showing no signs of improving profitability.

There also looks to be some operational delays with the B.C. Tweed JV greenhouse #2, which gained its cultivation license on April 14, 2018, but as of June 30 was not harvesting any supply.

Producers usually have partially grown plants that can be transferred to a facility the day it’s licensed, leading to at least a partial harvest a few months later.

Overhead Costs as a % of Revenue Are Going in the Wrong Direction

Invest Like You Own the Assets

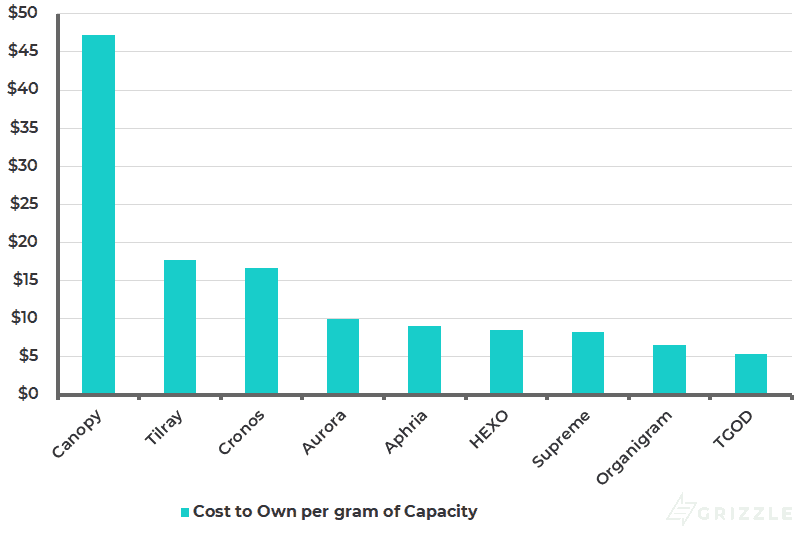

Investors should look at marijuana companies as if they are part owners of each company’s growing capacity.

When you think this way it will help you put each companies stock price into perspective.

Take Canopy Growth for example.

As an investor if you pay $47 to buy some Canopy stock you will technically own 1 gram of production when all planned greenhouses are fully built out.

You are expecting Canopy to take that gram and sell it for a profit which you are entitled to.

The problem is that Canopy currently loses $18 for every gram they grow and even if they can generate a 26% net income margin, in line with giant tobacco conglomerates, your 1 gram will generate $2.34 a year for your $47 payment, a payback period of 20 years and a negative present value.

This is why valuation is so important.

Any marijuana company can be a good investment if the price is low enough, but marijuana valuations are looking rich compared to future legal market reality.

Cost to Own One Gram of Future Growing Capacity

Management teams will push back and say they’re going to make money from much more than just growing and selling simple marijuana products.

We would argue that a majority of revenue will come from raw flower and oil-derived products for at least the next 5 years so valuations should be based on that business model.

Constellation Investment Detailed

This deal is effectively a takeover of Canopy Growth.

Constellation will now have 4 of 7 seats on the board and a controlling stake in Canopy if all warrants are exercised.

Current shareholders of Canopy are being diluted by 50% when including new shares and warrants being issued to Constellation.

The Details

Constellation Brands announced this morning that it’s investing C$5.1 billion into Canopy Growth for 104.5 million shares, bringing its stake to 38%.

Constellation was also awarded warrants that if exercised will bring their ownership stake to around 55% and put another C$7 billion of cash into’s Canopy’s coffers.

Canopy will be the only way Constellation plans to operate in the cannabis market, making it likely Canopy will eventually be taken over by Constellation.

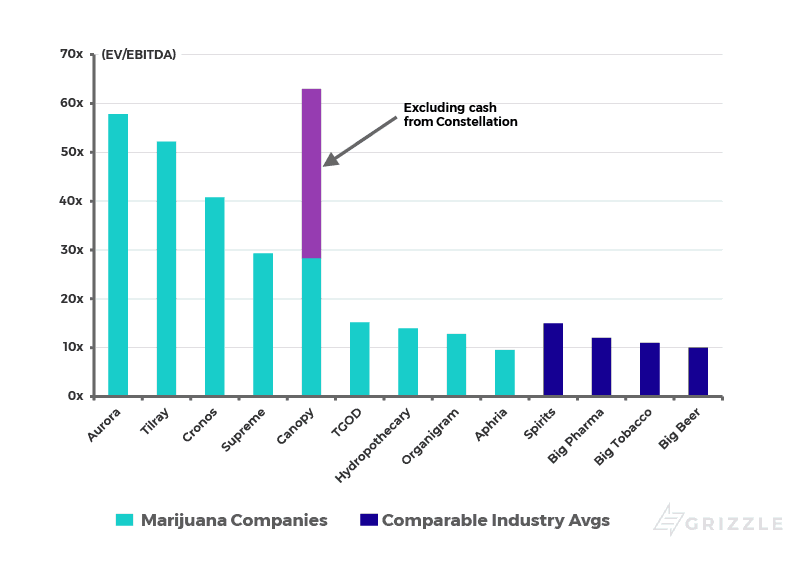

Canopy is Still The Most Expensive Marijuana Stock

Canopy Growth is now firmly the bellwether in the marijuana space, but investors are being forced to pay up for the privilege of owning it.

Canopy trades in line with the group average if you include the $5 billion of cash from Constellation Brands but we argue that should be excluded as it will be spent down eventually and is abnormally high vs peers, which skews the enterprise value calculation.

With the Constellation cash excluded, Canopy trades at a multiple of earnings before taxes, interest costs and depreciation (EBITDA) that is 50% higher than the group average and 4 times higher than comparable industries, such as wine and spirits, tobacco or beer.

Enterprise Value to EBITDA for Largest Licensed Producers

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.