Bottom Line

Constellation Brands did what no other cannabis company will, wrote down assets.

This quarter’s writedowns were only a drop in the bucket with more to come in our view (i.e Tokyo Smoke), but at least Constellation is admitting values for both cannabis and cannabis-producing assets need to come down.

Canopy Growth’s (TSX: WEED; NYSE: CGC) decision has implications for Aurora Cannabis and others.

If we don’t see an asset write-down from Aurora this quarter it means the company is doing whatever they can to postpone the inevitable and writedowns are almost assured in the December quarter when the annual auditing takes place.

Investors should expect writedowns across the board in cannabis over the next two quarters due to much slower growth of cannabis 1.0 than asset values imply.

Constellation Ultimately Buys the Rest of Canopy, But for a Big Discount

Constellation is now deep in the red on its Canopy investment and is going to be looking for any way to salvage what is left.

Canopy has no valuation support at C$20/sh and will continue falling towards its book value of C$10.60/sh while it continues to lose over C$140 million a quarter.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]We are calling it now, Constellation will average down on its investment and buy out the rest of Canopy if the stock price falls towards book value of ~$10/sh. Given the writedowns we think are still coming, the true book value is closer to $8.00/sh.[/su_panel]If you own Canopy today, a take under from Constellation, even if done at a 30%-50% premium would leave you sitting on big losses.

The bottom is not in, prepare for more pain.

The Quarter Could Have Been Even Worse

Canopy’s revenue may have missed analysts’ estimates by 27%, but results could have been even worse if it weren’t for the recent acquisition of C3.

C3 contributed 75% of the revenue growth in the quarter when excluding the sales returns and without it Canopy would have only shown 4% growth in the cannabis business overall.

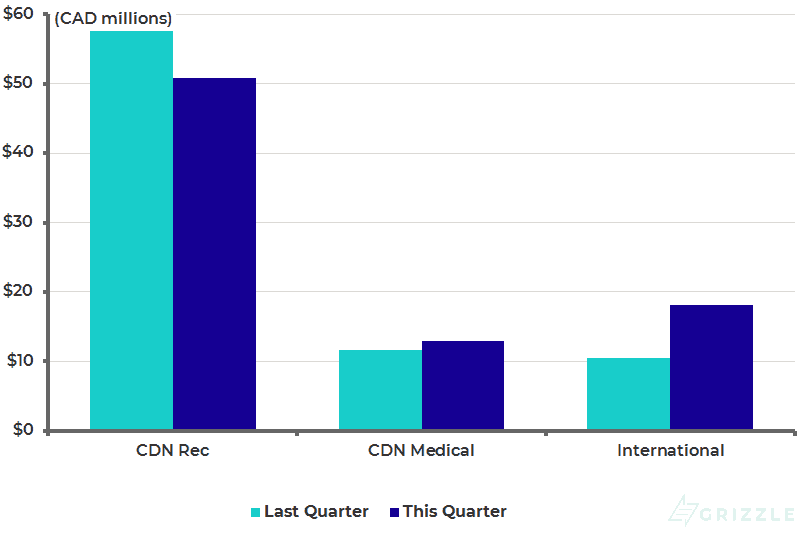

Revenue by Segment

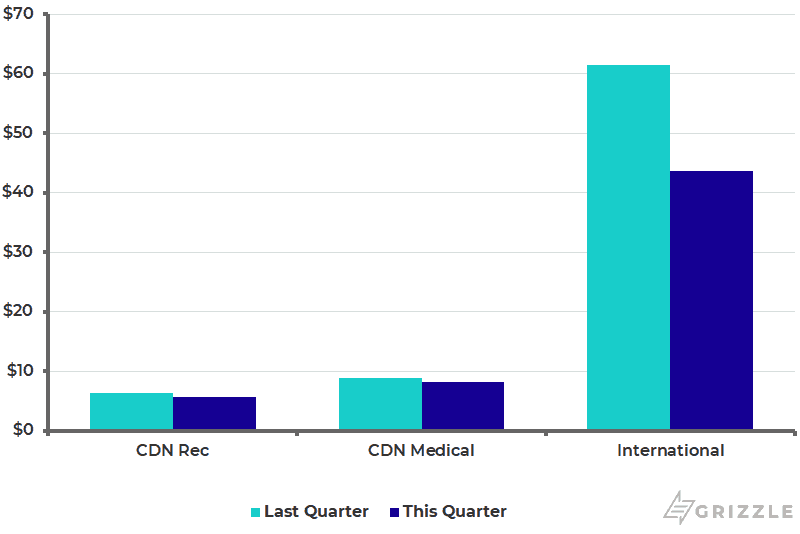

C3 is also the reason pricing held up so well. C3 selling price per gram of C$43 had a huge impact on Canopy’s average selling price as a whole.

Price per Gram by Segment

Prices in Canada fell 10% in the recreational market and 8% in medical and we expect pricing across the industry will continue to slide.

International prices were amazing but still fell 30% from last quarter and could start to become a drag on revenue growth next quarter if pricing keeps falling.

Where Does Canopy Go From Here?

Some investors may look at the write-offs this quarter as a positive sign. Canopy is bringing the balance sheet and revenue back to reality and will be set up to exceed expectations going forward.

The problem with this narrative is that Canopy is still attempting to sell products at a premium price into a market that’s barely growing.

Canopy may have the highest revenue per gram in the industry, but it comes at the cost of growth.

Management will not have the benefit of a German acquisition next quarter to mask recreational volumes that are actually falling.

The company even warned in the press release that the growth we saw internationally this quarter will not repeat.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Now that a price war is underway in the Canadian market, Canopy will have to live without growth if it wants to maintain premium prices, or it will need to bite the bullet and cut prices to drive growth. Either outcome will be a bitter disappointment to analysts who are expecting 30% revenue growth for the next two quarters.[/su_panel]Every licensed producer in Canada has two choices.

- Cut costs and resize your business to generate profits in a much smaller than expected legal Canadian cannabis market.

- Try to grow your way out of the Canadian disaster through international sales.

All the big LPs are choosing option number 2, and through that lens, Canopy is better positioned than most in the long term.

Canopy is generating the most revenue from Europe in the group so is well-positioned, however, results are at the whim of European politicians.

Canopy may end up being the winner in the race for international expansion, but in the meantime, the stock price is going much lower as it adjusts to the realities of the market.

Earnings Review

Canopy Growth (NYSE: CGC, TSE: WEED), the world’s largest cannabis producer, reported second-quarter results on Thursday, missing earnings and revenue estimates once again. The stock price fell as much as 10% in pre-market trade, having lost nearly 4% on Wednesday.

Net revenue of C$76.6 million was 229% higher than a year ago but missed estimates by C$14 million. Net revenue fell 15% from the first quarter but was impacted by a C$32.7 million restructuring charge related to the soft gel and oil portfolios. Gross revenue was 6% higher quarter-on-quarter.

The GAAP loss per share widened to C$1.08, missing estimates by C$0.73. The net loss of C$374.6 million narrowed from a C$1.28 billion loss in the first quarter.

EBITDA Continues to Deteriorate

Canopy Growth’s gross margin fell to negative 13% due to the restructuring costs and write-downs. Without these charges, the gross margin would have been 38%.

Operating expenses rose 15% from the previous quarter and 48% from a year earlier to $269 million. The higher operating expenses were attributed to marketing costs related to the roll-out of ‘Cannabis 2.0’ products in Canada.

The net result was adjusted EBITDA of -C$155.7 million versus -C$92 million in the first quarter. In addition, share-based compensation for the quarter amounted to C$92 .8 million, down slightly from the previous quarter.

Canopy harvested 40.5 tonnes of leaf, a 1% decline from the second quarter. In total 10,913 kilograms and equivalents were sold, resulting in inventory levels rising 17% to C$461 million. Cash and equivalents fell 13% to C$2.7 billion, implying a negative cash flow of about C$407 million.

Slowing Sales and Lower Prices Hit Recreational Revenue

Sales momentum has slowed in recreational segments, while medical dry cannabis sales have fallen, but been replaced by oil sales. International sales accounted for C$18 million or 15% of total gross revenues.

While the volume of recreational dry cannabis sold to businesses rose 9% sequentially, revenue fell 8% from the previous quarter. Business-to-business sales of oil and soft gels fell 80% sequentially, with revenue falling a similar amount.

Recreational sales to consumers showed stronger growth of 34%, though lower prices acted as a drag on revenue growth. Sales to consumers still account for just 10% of total dry cannabis sales.

Sales of medical dry cannabis fell 41% from a year ago but were 24% higher than the previous quarter. The company has managed to maintain margins in this segment allowing revenue to grow faster than volumes.

Canopy’s fastest-growing segment is cannabis oil and softgel for the medical market. Kilogram equivalent sales grew 46% from last quarter and 100% from a year ago to 997 kgs. Revenue from oils grew 205% from a year ago, but only 38% from the last quarter. This indicates prices may have come under pressure in the segment.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.