https://www.youtube.com/watch?v=mQjMhEl_erw

Legal cannabis producer Canopy Growth (NYSE:CGC, TSE:WEED) reported surprisingly strong results.

Revenue came in at C$124 million, 18% better than consensus of C$105 million.

Revenue benefitted from the recent skincare and vaporizer acquisitions and the rollout of more retail stores across Canada.

It looks like Canopy regained some of the rec market share it lost in June with sales into the provincial distributors rising to $53.5 million compared to $58.4 million two quarters ago.

The market will buy the stock on this revenue beat, but results were not driven by the Canadian cannabis business, it was the acquisitions of C3, This Works and Storz & Bickel.

Management guided that Storz & Bickel sales were seasonally strong this quarter and cannabis sales are usually down in Q1 over the holiday season of Q4 so these results could partly reverse next quarter.

Revenue was up 60% from last quarter, but if we remove returns which should really apply to a prior quarter revenue was up 13% QoQ though revenue was still up 50% from December 2018.

The EBITDA loss of -C$92 million was 20% lower than consensus of a -C$116 million loss and will be taken well by the market as a sign the growing losses are over.

Analysts expect the EBITDA loss to fall to ~C$300 million in the coming 12 months compared to a loss of C$380 million over the last 12 so there is more work to do.

Reaching positive EBITDA will be just the first step for Canopy to begin mending its reputation with investors.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]The new CEO is just beginning to restructure the company and we expect more write-offs to come. The expensive multiple means any earnings disappointments could hit the stock price hard. It will require more than a cash pile to rescue the fundamentals of this overvalued stock. [/su_panel]

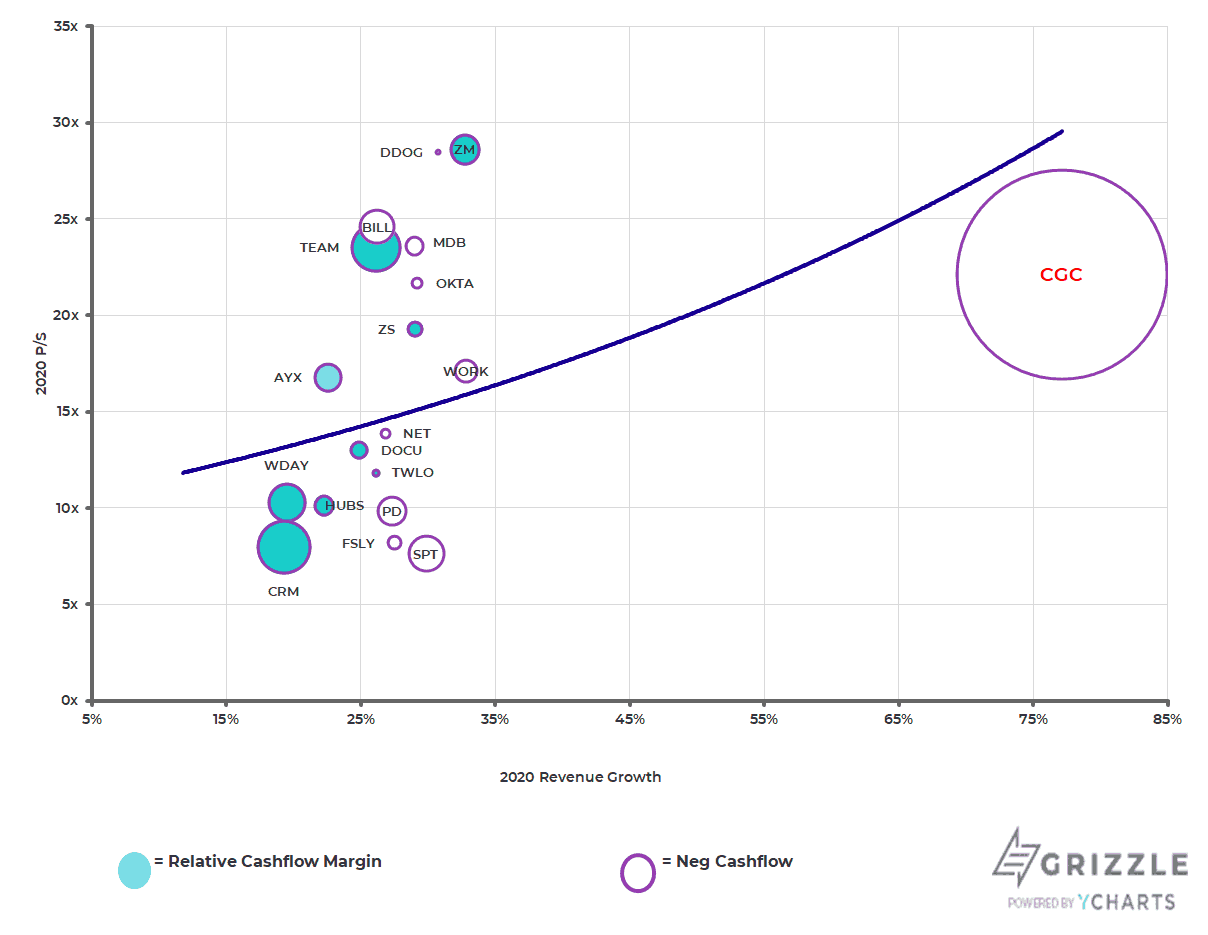

Canopy Not Priced for Surprises

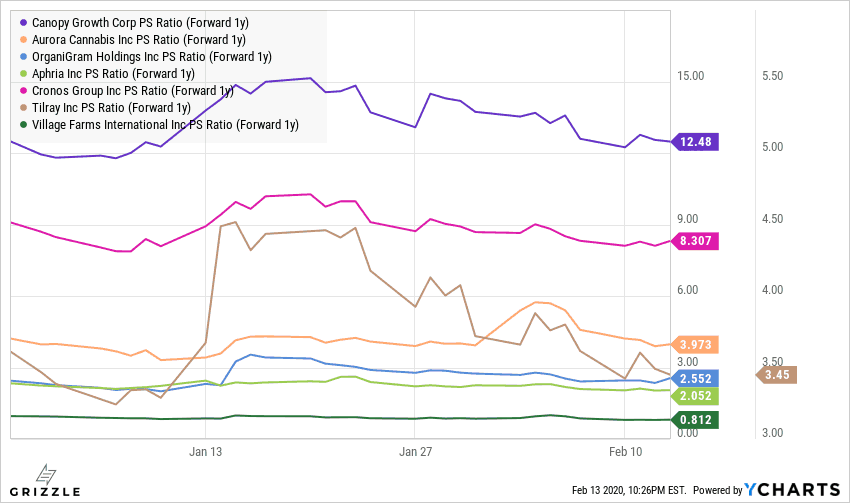

Canopy remains the most expensive cannabis stock in Canada.

At 22x price to sales, Canopy is literally priced like a tech stock, not a second rate producer of commoditized cannabis in a severely oversupplied market.

Cannabis = Tech, Naaaahh

Yes, the company’s international reach and name recognition among cannabis consumers are worth something, but the stock premium more than compensates for any positives results we expect it he coming 12 months.

Stepping back a bit, instead of owning a stock with headwinds still to navigate, you could own fast-growing and profitable tech stocks with better margins instead. This is called “opportunity cost” and is a very real concern in the cannabis industry.

Canopy has the least bad news baked into the stock and is most at risk of further stock price weakness once the new CEO announced asset write-offs and mothballs certain facilities, which we think is likely.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Analyst revenue estimates assume a doubling of the Canadian market every year, a 5% increase in Canopy’s market share to 30% from 25% and stable industry prices. Betting on all three outcomes at once is truly foolish considering Canopy is struggling to hold onto market share and the current oversupply has already pushing down prices.[/su_panel]Forward Price to Sales for Licensed Producers

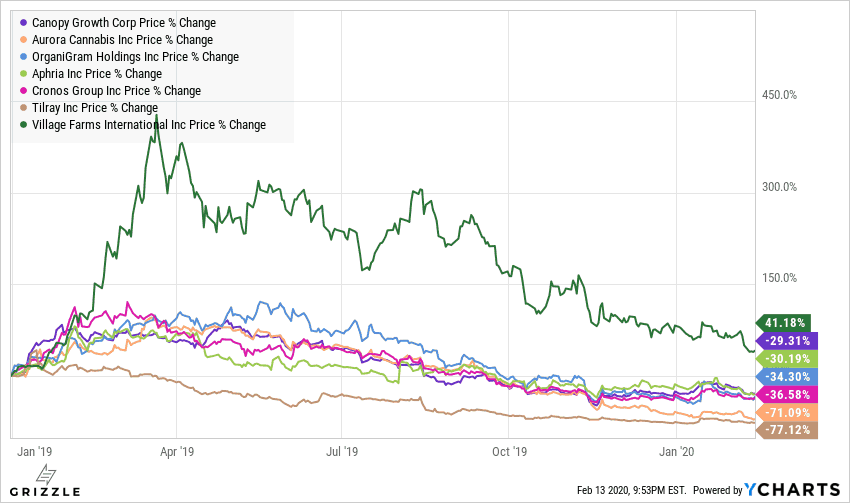

Canopy is the best performing stock in the past 13 months due only to the backing of Constellation Brands and Canopy’s relatively large cash balance.

The actual financials have been an unending nightmare for those who own the stock and a Powerball Jackpot for short-sellers.

It’s abundantly clear the stock has been artificially supported by the market belief Constellation will come in to buy the company if the stock price falls below $20/sh.

We looked into the probability of a buyout in a prior in-depth report and found that a Constellation buyout above C$10.00/sh is not going to happen.

Canopy (Purple) Has Fallen the Least Over the Last 13 Months

Canopy has breathing room to reach positive EBITDA, but it will take significant cost-cutting from the new CEO to avoid disappointing high investor expectations in 2020.

Will he make the hard decisions in time to avoid the issuance of more stock or debt borrowing or will he drink the industry cool-aid and believe legal market growth will bail him out.

Relying on consumers to irrationally switch from a cheaper and higher quality source of cannabis has left the industry in ruins.

It may be time for a different strategy…

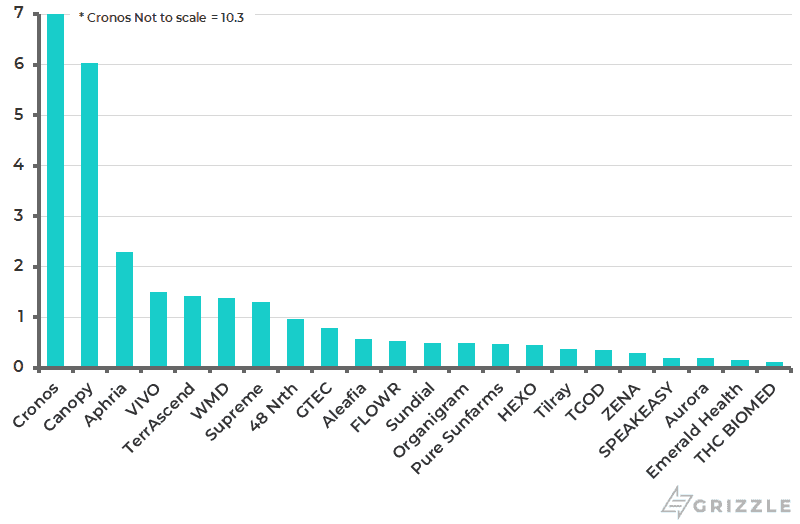

Years of Cash Left

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.