Bottom Line:

Canopy Growth continues to test investors resolve. This time last year Canopy was promising explosive growth and market domination, just as soon as cannabis was legalized.

Well here we are six months later and it looks like all the growth from the first wave of legalization is behind us and profitability is still nowhere in sight.

Canopy, and the rest of the cannabis stocks are doing their best to make investors feel like they are in the movie Groundhog Day, doomed to repeat June 2018 all over again.

Investors are back to hoping the next 6 months will show explosive growth and these companies will grow into their sky-high valuations, because as it stands today the rest of the year is a wash.

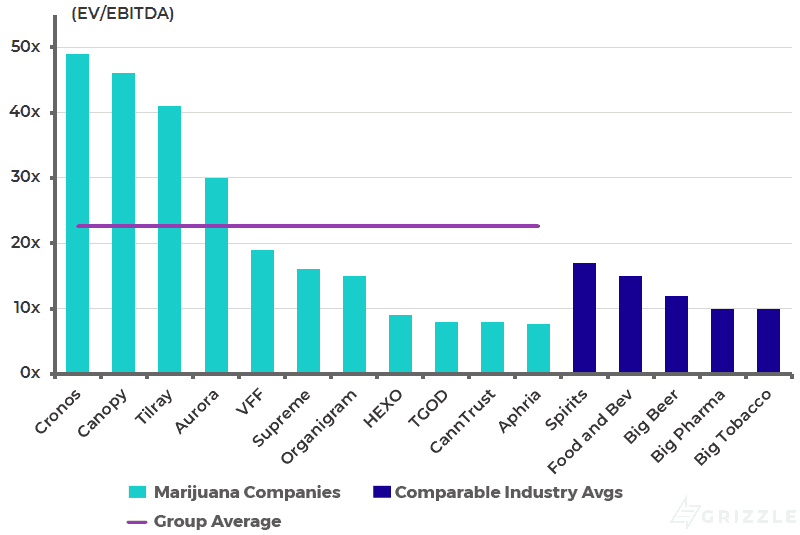

Estimate 2020 EV/EBITDA Multiples

Canopy saw cannabis revenue in Canada fall 4%, while international cannabis revenue fell 33% over last quarter. Volumes declined in both regions with additional pricing weakness internationally.

The $94 million headline revenue number this quarter benefited from a big increase in “other” revenue, though profitability did not. Overall it looks like revenue growth from selling cannabis will be hard to come by over the rest of the year.

With 9 months of legalization behind us, we’re left with two important takeaways.

Those Pursuing a Generic Quality, Mass-Produced Model will Continue to Struggle

The winners are going to be companies producing cannabis that is in demand, plain and simple. So far, the winners seem to be craft growers who focus on small batch quality flower and organic producers who command a big price premium in the market.

None of the big generic brands (Tilray, Canopy, Aurora, Aphria, HEXO, Cronos) have been successful in building superfans and repeat customers so far, judging by product reviews, rising inventories, and cannabis community discourse online.

Aurora, owner of organic producer Whistler, and Aphria, owner of Broken Coast, possess the internal DNA to break out of their generic cage. All the other big guys growing and selling conveyor belt cannabis will continue to struggle domestically and internationally unless something changes.

Capital is Trickling out of Canada and into the U.S.

From a Canadian investors point of view, why stick with the big guys who are struggling to grow revenue and generating mounting losses when there are cheaper U.S. names to buy with better growth opportunities and big potential regulatory catalysts to look forward to.

All is not lost for Canada however. LPs still have an opportunity, through vapes and edibles, to reestablish themselves as growth leaders, but the black market is evolving quickly with high-end products and far superior branding.

Branding restrictions will continue to be a challenge and may only get worse with an election on the horizon and a Conservative government leading in the polls.

Canada will have to get the rollout of edibles, vapes, and topicals right or its role as the world leader in Cannabis could be at risk.

As it stands today, Canopy’s earnings did nothing to change the current narrative for legal cannabis.

2019 is turning out to be another transition year on the way to a hopefully fully functioning and unrestricted legal cannabis market in the years to come.

Operational Review

Canopy generated net revenue of $94.1 million in the quarter, well below GMP estimates of $107 million but slightly above consensus of $90.5 million.

Revenue from actual cannabis production was down 5% to $69.9 million or $7.50/gram. Even with this decrease, Canopy still sits at the top among peers.

Revenue Per Gram

Canopy’s quarterly production costs increased 22% to $79.1 million. This is particularly weak when you consider revenues and cannabis production both fell. Among peers, they sit at the top with costs of $8.50/gram, a 32% increase quarter over quarter.

Production Costs Per Gram

Gross profit for the quarter was $15 million, down 18% from last quarter due to the rising production costs. Canopy continues to generate the lowest gross margin in the peer group, negating the benefit of having the highest revenue per gram.

Gross Margin Per Gram

General operational costs were $139.9 million, up 12% quarter over quarter. This was largely driven by jumps in General and Administrative (G&A) and Sales and Marketing (S&M). On a per gram basis, they are spending the most among peers at $15 per gram, a 22% increase over last quarter.

General and Administrative Costs Per Gram

This left a quarterly EBITDA loss of $124.9 million. This represented a 17% decrease and left them with the largest per gram deficit in the group.

Quarterly EBITDA Per Gram

Canopy spent $1.6bn on property, operations and buying other companies last quarter. This is a massive burn rate.

They will likely be back to the market looking for more cash before the year is out.

The Supply-Demand Conundrum

Two of the most telling numbers to come from Canopy’s earnings are their kilograms sold and international medical revenue. They sold only 9,329 kg, down 8% quarter over quarter, while international medical sales fell an eye-popping 33% quarter over quarter to only $1.8 million.

This raises some red flags for us as we expected continued robust sales internationally to make up for some of the weakness in Canada.

Another worrying sign was the level of inventories, which increased 42% quarter over quarter to $262.1 million, reaching almost a year of sales. This should put the argument that there is a lack of supply, not demand to bed once and for all.

Overall, we came away this quarter with more questions than answers about the future.

Canopy is putting together an imposing group of assets, but the question remains, can they execute?

Unfortunately, investors will have to wait a few more quarters if they want to find out.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.