Bottom Line

Canopy Growth stock (TSE: WEED) should trade off on its earnings report today.

Not a great quarter from Canopy on both a numbers basis and our gut feeling after reading management’s comments.

We would recommend investors move into lower priced, but just as capable, marijuana producers if they still believe in the potential of this industry.

Management’s decision to stop reporting growing costs was a huge misstep.

It is ok to argue the current metric is no longer useful to investors, but give them a new metric to follow instead of refusing to provide any information at all.

Bruce Linton also appointed a co-CEO to handle operations while presumably he handles the empire building.

Appointing a co-CEO before the legal industry has even opened demonstrates management’s embedded hubris.

This combination of hubris and declining transparency is never a good combination in a fledgling industry.

What Went Right

Canopy Growth had another quarter of explosive growth — revenue was up 55% in the last 12 months.

Prices charged for oils and capsules continue to increase and are contributing to a rising selling price per gram, a positive sign for revenues.

The company now has 74,000 patients, up 35% over the last year.

The company is well positioned for legalization with supply agreements signed in the 5 largest provinces and retail stores under construction in the provinces that allow private retail opportunities.

Canopy has over 16,000 kg of dry equivalent marijuana in storage ready for legal sales, only enough to supply Canada for 15 days.

A significant shortage looks to be inevitable in the early days of the legal market, benefiting the company through higher selling prices and market share.

What Went Wrong

Canopy Growth reported revenue that missed expectations by 9%. This is the seventh quarter the company has missed analyst revenue estimates.

Management filed a proxy statement along with earnings asking for shareholder approval for another 13 million shares to be issued for employee compensation, diluting current shareholders by another 6%.

The cash burn also increased with earnings before taxes, interest costs and depreciation (EBITDA) coming in at a loss of $25 million vs a $1 million loss this time last year.

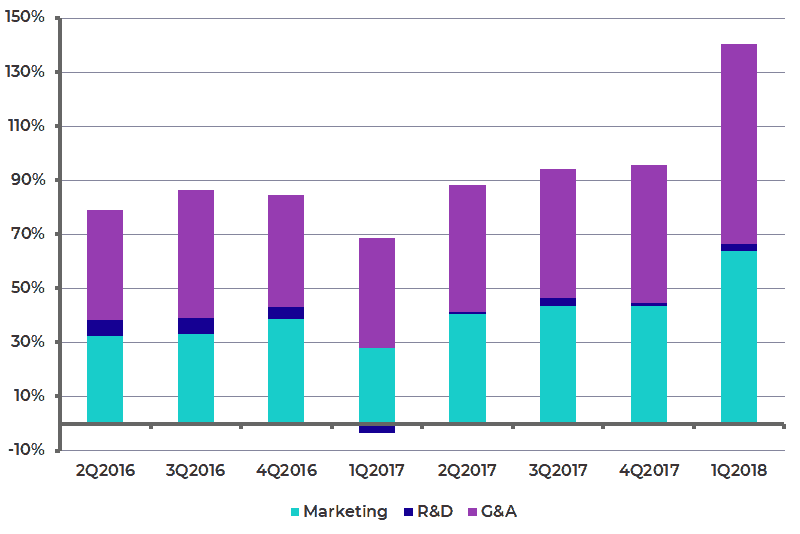

Overhead costs are still going up as a percentage of revenue and with stock prices embedding at least 30% EBITDA margins in coming years, Canopy still has a lot to prove to justify its premium valuation.

Overhead Costs as a % of Revenue Are Going in the Wrong Direction

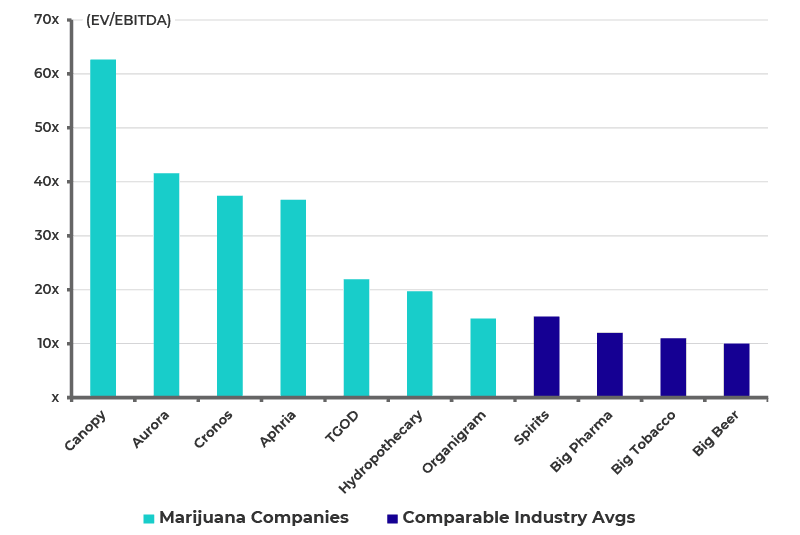

Canopy is Still the Most Expensive Marijuana Stock

Canopy Growth may be the bellwether in the marijuana space, but investors are being forced to pay up for the privilege.

Canopy trades at a multiple of earnings before taxes, interest costs and depreciation (EBITDA) that is 50% higher than the second most expensive player, Aurora Cannabis, and 5 times higher than comparable industries, such as wine and spirits, tobacco or beer.

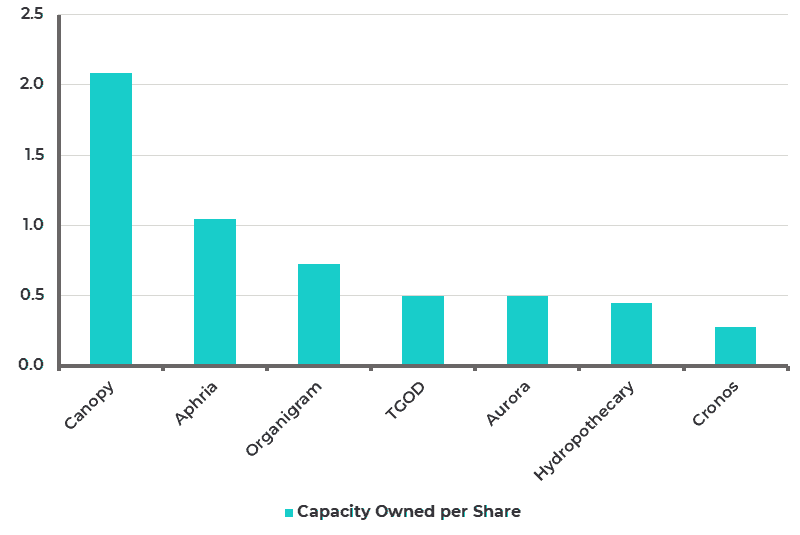

Looking at the industry through the lens of the price an investor pays for ownership of a portion of Canopy’s production capacity, we see that a share of Canopy Growth entitles you to 2 grams of long-term capacity, twice as high as peers.

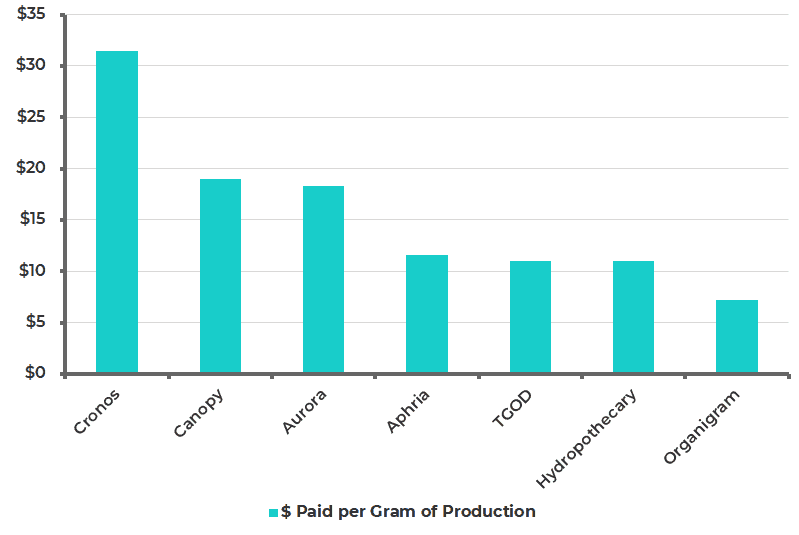

However, the stock price is so high that you’re effectively paying $20 for each gram of capacity.

Only Cronos Group is more expensive on a cost per gram basis.

This metric is useful at this early stage because though no one knows how much cash each company will generate, investors can at least see how much they’re paying upfront for ownership of each company’s production capacity.

Price Paid Per Gram of Capacity You Are Entitled to

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.