CarMax reported its first quarter fiscal 2021 results ended in May pre market that exceeded Wall Street’s expectations.

The company generated $3.23B of revenue, beating analyst estimate of $2.7B by 21%, but was down by 40% year over year.

CarMax was able to generate net income of $5M, but it was significantly lower by 98% year over year.

As a result, earnings per share was $0.23 which crushed consensus of $0.14 by 64%.

The company disclosed its EBITDA of $87M, which was higher than the street estimate of $68M by 26%, but tanked by 79% year over year.

Debt Burden

The drastic drop in EBITDA should be a cause for concern because of the company’s massive pile of debt.

Since CarMax’s debt to EBITDA ratio has roughly soared to 171X, compared to 33X in the last first quarter, the company faces the very real possibility of not being able to meet its debt obligations due to being highly levered.

This issue is further amplified when considering the fact that its current cash reserve only allows the company to last for a less than a quarter without having to dilute its shareholders or finance more debt.

However the company sits on a massive auto loans receivables amount worth over $12B. This is mainly due to the fact that CarMax Auto Finance has offered various payment assistance options including waiving late fees that expired in May 31.

Therefore, we believe that the company has a chance to pay its debt without having to fully resort to more dilution and debt issuance if it is able to collect at least the right amount of receivables in the coming months.

Coping With COVID-19

The sudden decline of its performance year over year was solely due to the outbreak of the virus.

As a result the company’s stock price dropped significantly along with its peers, but efforts taken to adapt to the new reality has instilled confidence amongst investors causing its shares to claw back most of its losses.

Another key initiative taken by the company to retain much of its operations during the pandemic was the move towards conducting most of its business processes online.

According to its recent response to the virus, the company announced that via online its customers are now able to select a vehicle, get pre-approved for financing, and get a trade in offer on an existing vehicle if applicable.

The company also conducts curbside operations at most of its stores now where it allows customers to finalize their transactions without having to come into the store and violate social distancing norms.

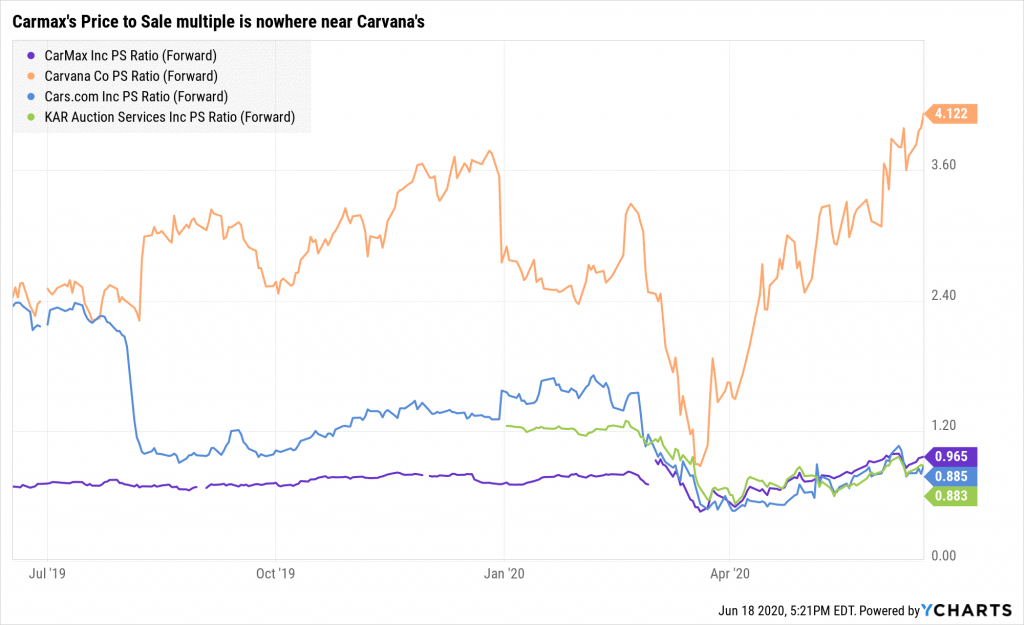

CarMax is not the only company in the sector to rely on online sales, as industry leader like Carvana has also embraced this trend. This has allowed many investors to renew their faith in the sector and many short sellers to cover their positions as a result.

But as the following chart illustrates, this has benefited mostly Carvana’s share price since its PS multiple has risen more aggressively than its peers.

However when considering the fact that the unemployment rate still remains high thanks to the virus, investors must realize that people are not as confident as they once were in making large item purchases.

Therefore we believe that regardless of its initiatives, Carvana’s PS multiple suggests that its share price make light of this fact, while CarMax’s PS multiple implies that its share price better reflects this issue.

Final Thoughts

Even in light of the current circumstances, CarMax has managed to beat several analyst estimations in the reported quarter.

However its debt burden is quite severe and if the company cannot effectively continue collecting its receivables, the company might have to dilute their shareholders and/or issue more debt.

Also, even though the company has a conservative PS multiple compared to Carvana, investors must understand that business might not go back to normal due to the high unemployment rate unless a vaccine is found, and its debt is under control.

Therefore we encourage investors to exercise caution if they are contemplating adding this company to their portfolio.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.