Recently in Hong Kong this writer can report that Hong Kong maintains its distinctive energy.

If the border remains closed to most non-residents, and is likely to remain so for now, those hotels not minting money from the quarantine business are on a “needs must” basis opting for so-called staycations whereby they offer cheap “all you can eat” deals to local residents who do not want to venture abroad because of the two or, often, three-week quarantine they would face on their return.

The result is crowded hotels with reception areas looking more like the check-in areas of budget airlines and pool areas exhibiting a complete lack of social distancing.

This curiosity aside, Hong Kong remains remarkably normal with land auctions, as ever, a major item in the news.

Henderson Land, one of the territory’s most long-established property developers, agreed on 3 November to pay a record HK$50.8bn (US$6.5bn) for a 50-year land grant for a commercial development on the harbour front of the Central financial district.

Henderson said in a statement that the project, which will comprise two office towers and a multifunctional building close to the harbour, will involve a total investment of HK$63bn (US$8.1bn).

The price paid works out at HK$31,463 per sq ft (US$4,034) which is a major sign of confidence.

The above is a reminder, if it was needed, of the extraordinary and likely continuing resilience of the Hong Kong property market despite all the political turbulence of recent years resulting in the passing of the National Security Law on 30 June 2020, commonly referred to locally as the “NSL”.

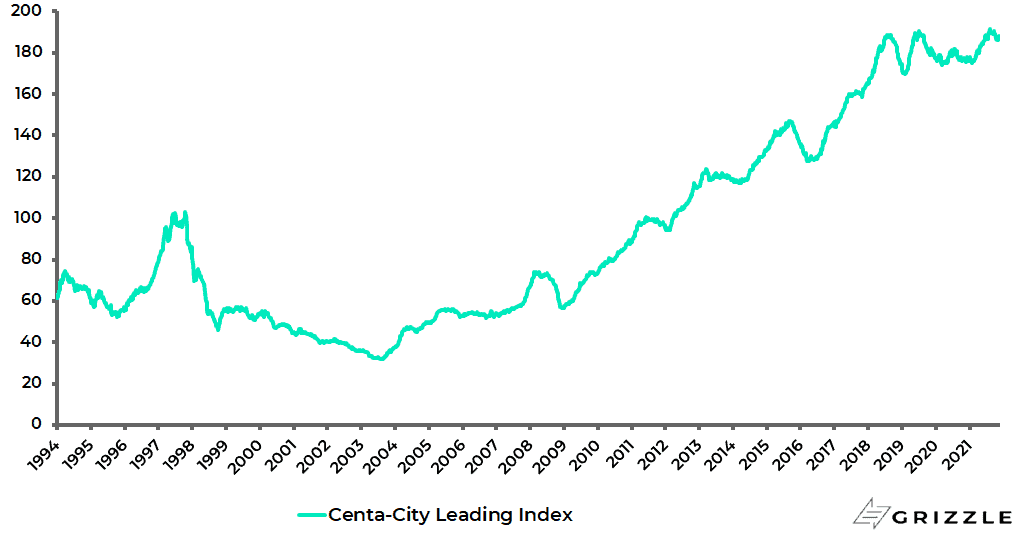

The Centa-City Leading Index of apartment prices has risen by 6.1% so far this year, though down 2.3% from the record high reached in early August.

Hong Kong Centa-City Leading Index of apartment prices

Residential property yields also remain positive relative to financing costs even though rents have been falling with the obvious risk, giving the continuing strict quarantine regime, departing expat families at the end of the current school year.

Residential property yields are running at 2.4%, compared with mortgage rates of around 1.4%.

There are about 300,000-400,000 expats in Hong Kong, excluding domestic helpers, accounting for about 4-5% of the population.

That said, many more mainland Chinese can be expected to move to the territory when the border is reopened even if there is a mass expat exodus.

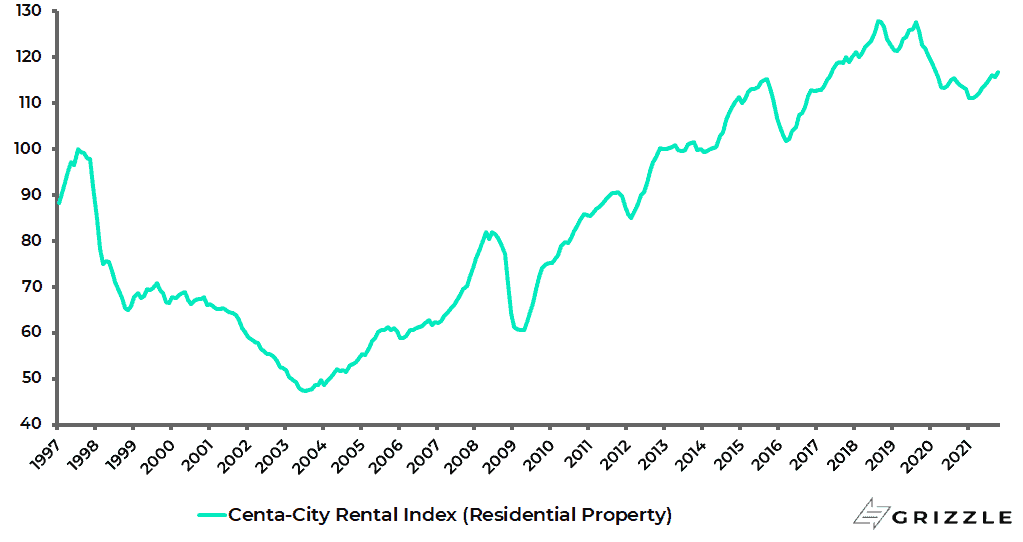

They will, ironically, be more confident about buying property because Beijing is now in charge. Meanwhile, the Centa-City Rental Index of residential properties has declined by 8.5% since August 2019, though it is up 5.2% from the recent low reached in February.

It, therefore, looks like residential rents have already bottomed.

Hong Kong Centa-City Rental Index of residential properties

This means that the main risk, aside from the obvious one of higher US interest rates and therefore higher Hong Kong dollar rates given the US dollar currency peg, is a surge in residential supply triggered by Beijing’s desire to do something about affordability in the territory.

In this respect, mainland officials in Hong Kong recently made public comments about the “shocking” living conditions in the territory.

Thus, Luo Huining, the head of the Liaison Office of the Central People’s Government in Hong Kong, said in late September that he was saddened by the “cage house” living conditions in Hong Kong and that housing has become Hong Kong’s “largest well-being” issue.

Still, Beijing will likely implement any major changes to land policy on a highly incremental basis.

For it surely does not wish to trigger a collapse in prices which would undermine the goodwill of the 50% of the Hong Kong households who own their own residence.

On the subject of land prices, CY Leung, former Hong Kong Chief Executive and now a vice-chairman of the National Committee of the Chinese People’s Political Consultative Conference, told Reuters in September: “They (property tycoons) are a major component of our political and economic ecosystem, so we need to be careful … and not throw the baby out with the bathwater” (see Reuters article: “With tighter grip, Beijing sends message to Hong Kong tycoons: fall in line”, 17 September 2021).

It also remains the case that, for all the talk of unaffordable housing and the lack of supply being a trigger for the 2019 street riots in Hong Kong, the reality is that a not insignificant percentage of the population chose to live in government subsidised housing because it is so cheap.

Thus, 30% of the population now live in public rental housing while 15% live in subsidised sale flats, according to the Transport and Housing Bureau.

The average monthly rent of public rental housing in Hong Kong Island is only HK$74/sqm, compared with HK$400/sqm for private residential properties.

Finally, on this subject, it should be noted that there have never been any specific demonstrations against high land prices per se in Hong Kong.

The Solution to China Property is More Supply, Not Lower Prices

Moving on to the still topical subject of China property, for now the four tier-one cities’ average selling prices are only down about 1% from the peak level reached earlier this year.

Going forward the mainland authorities would probably like to see property prices moving broadly in line with income growth.

But it is certainly the case that Beijing does not want to see a major decline in prices which, to state the obvious, would be highly destabilising in macroeconomic terms.

In this respect, President Xi Jinping’s proclaimed slogan of “Common Prosperity” is much more about creating more public housing than bringing down prices, in terms of giving people a place to live rather than guaranteeing that they own their own property.

The base case on China property remains the same as discussed in this column recently (see The big winner of China housing fears? The stock market, 18 November 2021).

That is that the Chinese government induced the current liquidity squeeze facing the most leveraged developers, such as Evergrande, when it announced its Three Red Lines policy back in August 2020 and therefore should be prepared to deal with the fallout; though it must be admitted that the existence of US$152bn of Chinese property developer dollar bonds offshore is a complicating factor.

The offshore bondholders are certainly not the priority of the China central government which is much more concerned that the existing projects where Evergrande and others have sold pre-sales flats are completed which may mean SOE developers taking over the projects.

Chinese Currency is Surprisingly Resilient

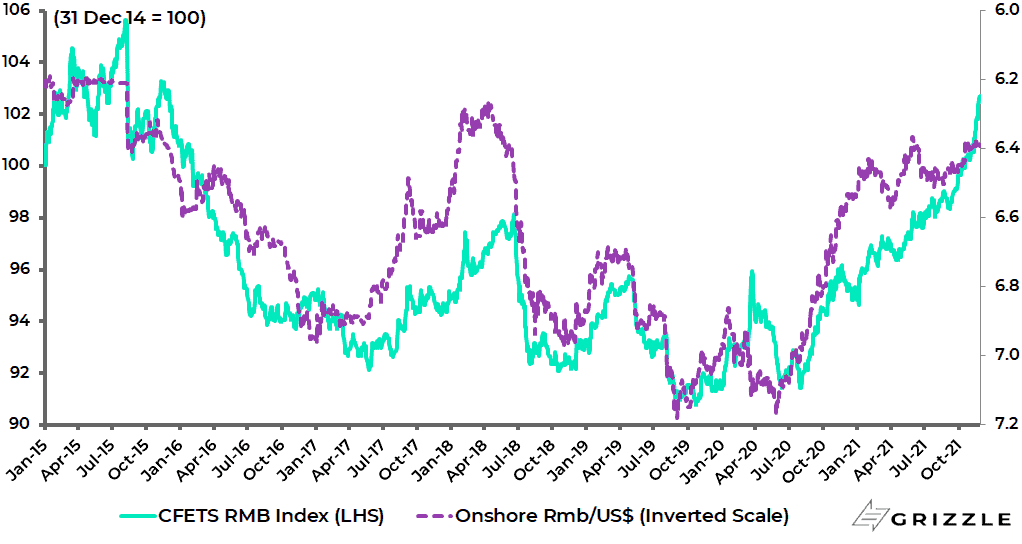

Meanwhile, it is worth highlighting again the continuing resilience of the renminbi despite continuing talk of China’s “Lehman moment” and despite recent US dollar strength against most other currencies.

The renminbi has appreciated by 2.1% against the US dollar so far this year while the PBOC’s trade-weighted Renminbi Index against 24 currencies is up 8.3% year-to-date to its highest level since December 2015.

China CFETS trade-weighted Renminbi Index and Rmb/US$ (inverted scale)

The renminbi strength prompted the PBOC to issue a reminder on 18 November about the risks of betting on one-way appreciation of the Chinese currency, with the statement saying that the renminbi may in the future “either appreciate or depreciate” (see Bloomberg article: “PBOC Warns Against One-Way Yuan Bets After Rally to 6-Year High”, 19 November 2021).

The central bank statement comes at a time when the likelihood, going forward, is for incremental targeted easing in China.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.