There were significant developments out of China last quarter. The most important was the announcement by state media in late February that term limits will be ended for the Chinese presidency.

Then almost simultaneously there was the announcement by the China Insurance Regulatory Commission (CIRC) that it will take over the management of Anbang, the Chinese insurance company famed for its aggressive acquisition strategy overseas. Both decisions are connected in the sense that they reflect the trend towards increasingly strong centralized leadership in the past five years since President Xi Jinping assumed power in November 2012.

Xi’s Legacy: Supply-Side Reform and Infrastructure

The news on ending terms limit is not a surprise in the sense that it confirms growing rumours in Beijing over the past year that Xi’s term in power would be extended beyond the usual 10 years. This is a positive development if it is believed, as is the case here, that Xi’s major policies in the economic sphere, namely supply-side reform and One Belt One Road, are positive. Supply side reform is all about cutting excess capacity. One Belt One Road is about building infrastructure links between China and Europe, recreating the old Silk Road.

While many will view the return to what could be described as ‘Great Leader politics’ as increasing the risk of political instability longer term, the practical reality for investors focusing on the short to medium term, which should be defined as one to five years, is the opposite. This is because investors can assume the continuation of policies the direction of which is now clear.

Anti-Corruption Campaign Provided ‘Shock and Awe’

Meanwhile, President Xi has already secured one extremely important condition required for ongoing stability in China. That is that he has restored the legitimacy of the PRC in the eyes of the population in terms of the sheer scale of the anti-corruption campaign over the past five years.

The Central Commission for Discipline Inspection (CCDI) reported in January that 527,000 officials were punished for corruption in 2017, including 58 provincial or above level leaders. That anti-corruption campaign moved in the past year into the financial services area, a development which has also been complemented by an intensifying crackdown on so-called shadow banking.

Reigning in Speculative Risk

One aspect of this crackdown was the change of leadership at the CIRC. Indeed, the former head of the CIRC, Xiang Junbo, was expelled from the Communist Party last year for allowing insurance companies like Anbang to finance their overseas acquisitions via ultra-aggressive fundraising techniques domestically. For example, Anbang bought the Waldorf Astoria hotel in New York, among many other assets. Meanwhile, the message sent has been all the more dramatic given that Anbang’s chairman Wu Xiaohui, now under arrest, was once married to the granddaughter of Deng Xiaoping.

A constructive view should be taken of the crackdown on shadow banking because financial spivvery in China’s private sector had run amok as the Anbang example illustrates. Still, the obvious risk from the Chinese Government’s current deleveraging policy remains that it creates collateral damage in the real economy. In this sense, the authorities are still involved in a delicate balancing act. The positive interpretation from the latest Anbang development is that they are seeking to control the domestic fallout while Anbang’s numerous foreign assets will be put up for sale.

Beijing Focused on Crisis Containment Rather than Crisis Management

This columnist will continue to give the benefit of the doubt to Beijing that it can maintain this balancing act. This is because it is much easier to manage a problem if it is dealt with proactively rather than if a government only reacts after it has become a crisis. This is the key difference, though far from the only difference, between China’s ‘shadow banking’ and related debt problem and the implosion of asset-backed securitization in the Western world 10 years ago when the United States’ housing market blew up.

Meanwhile, further evidence of Beijing’s ongoing commitment to reform and related deleveraging last quarter, was provided by the speech given by Xi’s top economic adviser Liu He at the World Economic Forum in Davos in late January. In this case it is significant that Liu, who led the Chinese delegation at Davos, was the only policymaker who was not a state leader to speak at one of the annual event’s 10 main sessions. In this sense Liu was given the same status as other speakers at the event, be it The Donald, Frau Merkel, Emmanuel Macron or Narendra Modi.

As expected, Liu was also appointed as a vice premier in March at the National People’s Congress. Liu, who was a ‘middle school’ classmate of Xi, is widely credited with the ‘supply-side reform’ and related ‘deleveraging’ agendas. He is also much more aware about the risks of rushing capital account liberalization than the now retired POBC Governor Zhou Xiaochuan, who indeed had always been a champion of capital account liberalization.

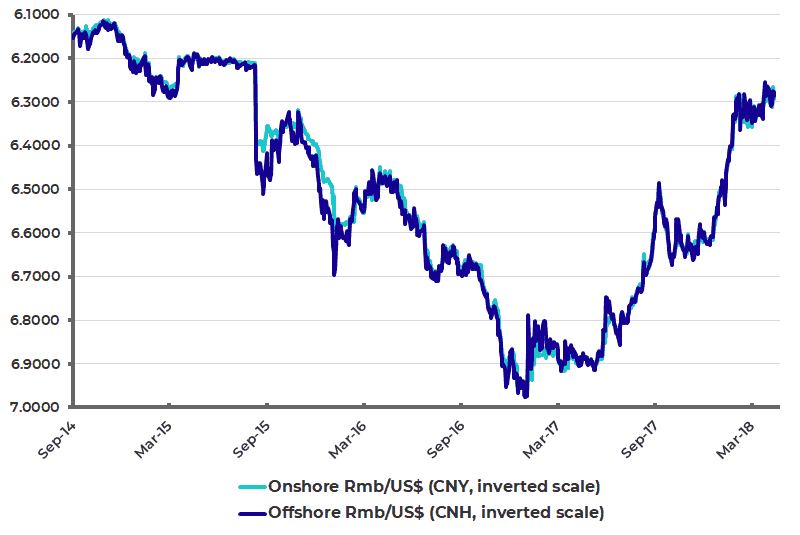

This is ironic since the former PBOC Governor warned last October of the risk of a ‘Minsky Moment’ in China. Yet the real risk of such a Minsky moment was created by Zhou’s promotion of the offshore renminbi market which enabled the speculative attack on the Chinese currency in the autumn of 2015, thereby giving a devaluation signal to 1.4 billion Chinese (see following chart).

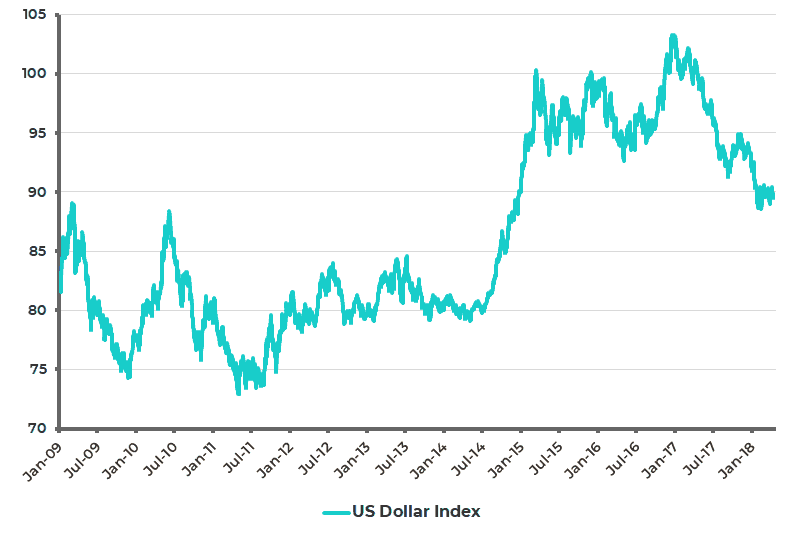

The Beijing authorities are now much more aware of that risk which is why there has been much more focus since then on enforcing the rules of China’s closed capital account; though this task has definitely been aided over the past 15 months by the renewed depreciation of the US dollar (see following chart). The renminbi has risen by 6% against the US dollar since the start of 2016 when fears of a renminbi collapse were at their greatest among international investors.

Onshore and offshore renminbi against the US dollar

US Dollar Index

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.