There has remained continuing newsflow on the US-China trade war. What about the condition of the Chinese economy? The view here remains that Beijing is in control, while trying to avoid being panicked by trade war concerns and the like into a potentially destabilizing aggressive stimulus.

It is a concern that producer price inflation fell back into nearly negative territory in June. PPI inflation slowed from 0.6%YoY in May to 0.0%YoY, the lowest level since August 2016. Still, set against this, nominal GDP growth accelerated last quarter, rising from 7.8%YoY in 1Q19 to 8.3%YoY in 2Q19 (see following chart). And the trend in nominal growth, as opposed to real GDP growth, remains the most important point for equity investors since companies’ revenues and profits are in nominal terms.

China PPI Inflation and Nominal GDP Growth

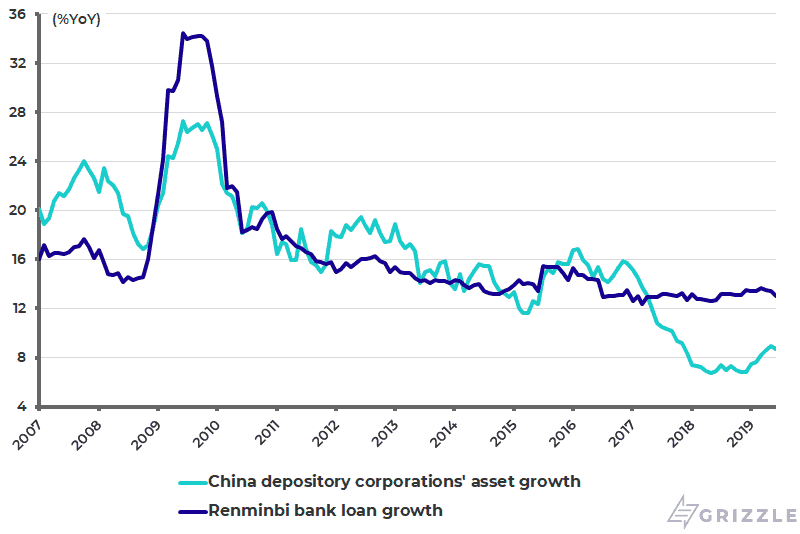

The credit data also continues to support the base case for a U-turn pickup, though the potential risk remains an L-shaped outcome. A V-shaped recovery will not happen precisely because of the lack of an aggressive stimulus. Renminbi bank loan growth moderated from 13.4%YoY in May to 13% in June. Meanwhile, bank asset growth decelerated slightly in June after accelerating for five straight months.

Depository corporations’ asset growth slowed from 9%YoY in May to 8.7%YoY in June, compared with the recent low of 6.8% reached in December; though it still looks like an uptrend on the chart (see following chart). This remains critical to monitor because the asset growth data series has best captured the macro impact of the squeeze on shadow banking since 2016, as discussed here previously (China’s Erratic Housing Market and the State of its Credit, May 7, 2019).

China Depository Corporations’ Asset Growth and Renminbi Bank Loan Growth

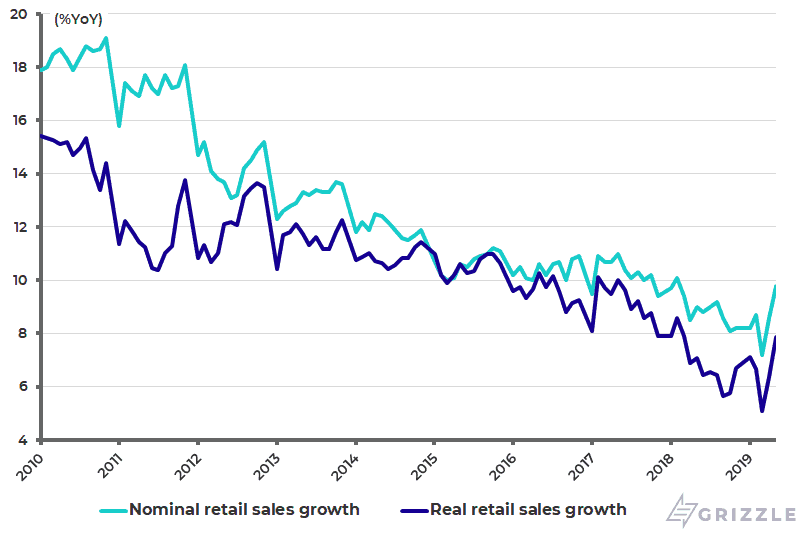

As for consumption data, retail sales growth picked up. Nominal and real retail sales growth rose from 8.6%YoY and 6.4%YoY respectively in May to 9.8% and 7.9% in June, the highest level since March 2018 (see following chart). Urban retail sales rose by 9.8%YoY in nominal terms in June while rural retail sales were up 10.1%YoY.

China Retail Sales Growth

Since retail sales only measures consumption of goods, it is also worth noting that consumption expenditure per capita growth also increased in nominal if not real terms. The household survey’s consumption expenditure per capita growth, which includes spending on services, rose from 7.3%YoY in 1Q19 to 7.5% in 1H19 in nominal terms (see following chart).

China Household Survey: Consumption Expenditure per Capita Growth

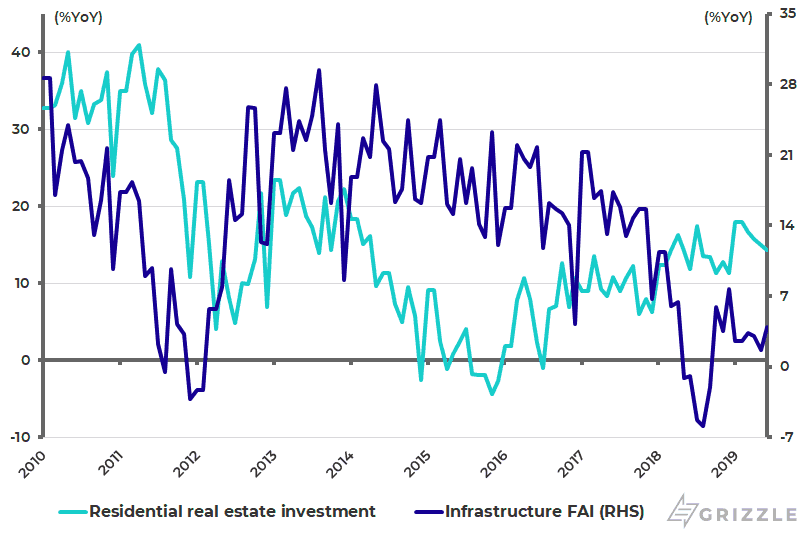

What about the investment data? Residential property investment remains for now resilient while infrastructure investment has picked up again. Residential real estate investment rose by 14.3%YoY in June and was up 15.8%YoY in 1H19, compared with 13.4% growth in 2018.

Infrastructure fixed asset investment growth rose from 1.6%YoY in May to 3.9%YoY in June and was 3.0%YoY in 1H19, compared with a 1.8% increase in 2018 (see following chart). Still, perhaps most promising was that manufacturing and private-sector fixed asset investment stabilized after the declines registered in recent quarters. Thus, manufacturing and private-sector investment growth rose from 2.7%YoY and 5.3%YoY respectively in the first five months of 2019 to 3%YoY and 5.7%YoY in 1H19, after declining from 9.5% and 8.7% in 2018 (see following chart).

China Infrastructure Fixed Asset Investment and Residential Real Estate Investment Growth

China Private and Manufacturing Sector Fixed Asset Investment Growth

On balance it is a positive that the data is not worse given the severe deleveraging signaled by the sharp decline in bank asset growth since 2016 and the blow to sentiment created by the ongoing trade and tech wars. Meanwhile, if there is a risk of more of a China growth scare in the second half of this year, it is most likely to come from the hitherto resilient property market where residential floor space started is running ahead of residential floor space sold. Residential floor space started rose by 10.5%YoY to 780m sqm in 1H19, after rising by 19.7%YoY to 1.53 billion sqm in 2018. By contrast, residential floor space sold declined by 1%YoY to 662m sqm, following a 2.2% increase to 1.48 billion sqm in 2018 (see following chart).

China Residential Floor Space Sold and Started (annualized)

If there is any sign of a real weakening in demand, Beijing has plenty of room to relax property tightening policies, particularly in the bigger cities where experience shows there is always pent up demand. Meanwhile, headline writers have, unsurprisingly, focused on China’s real GDP growth of 6.2%YoY in 2Q19 being the slowest since the quarterly data series began in 1992. Still, to me, it is extremely encouraging that the Chinese Government is no longer fixated on calendar year GDP growth targets. Indeed, this is one of the positives of the extension of Chinese President Xi Jinping’s term in government since it reduces the short-term political need for stimulus. Indeed the message out of Beijing of late to its people has been to prepare for the economic equivalent of “The Long March” in terms of the threat from the U.S. posed by trade wars, tech wars, and the like.

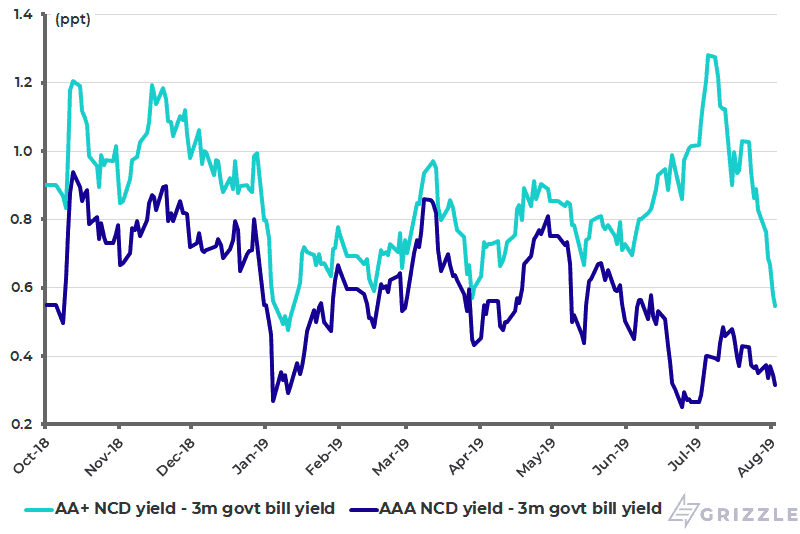

It is also worth mentioning an interesting development of late. That was the decision by the mainland authorities not to cover all liabilities when the government took over Baoshang Bank in Inner Mongolia in late May. The regulators, in the form of the China Banking & Insurance Regulatory Commission (CBIRC) and the People’s Bank of China (PBOC), said they would not guarantee all of the liabilities of Baoshang, which was based in Inner Mongolia and had assets of Rmb576 billion. True, all household depositors were fully guaranteed but corporate depositors and interbank creditors with over Rmb50 million (US$7.2 million) exposure were only paid out up to 70-90%.

This laudable attempt to impose some discipline in a banking system where blanket state support is assumed could easily have triggered mass panic in what was the first bank takeover by the authorities since the early 2000s. It is, therefore, reassuring that the PBOC was seemingly able to manage the fallout by an injection of liquidity. In the meantime, credit spreads narrowed for the negotiable certificates of deposits (NCDs) of high-quality banks and rose for lower-rated banks until of late, which is as it should be. Thus, the AA+ rated NCD yield spread over the 3-month government bill yield rose from 77bp in late May before the PBOC announcement to 128bp in early July but has since declined to 55bp. By contrast, the AAA rated NCD yield spread has declined from 65bp in late May to 31bp (see following chart).

China Banks’ NCD Yield Spread Over 3-month Government Bill Yield

The Baoshang takeover has been used, therefore, to advance structural reform in the fight against moral hazard. That this was attempted so soon after the stock market-driven fallout last year from the deleveraging squeeze on shadow banking shows that the relevant authorities remain committed to reducing risk in the financial sector and, more importantly, continue to have the necessary high-level political support to do so. This effort continues to be led by CBIRC chairman Guo Shuqing, who was quoted in March as saying that “high risk financial institutions should be allowed to exit the market”. Guo is also, importantly, the Communist Party secretary of the PBOC.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.