It remains obvious that events of late have continued not to move in the direction of the base case here, namely that Donald Trump will, sooner or later, turn on a dime and do a trade deal with China.

US Steps up Attacks on China

There have been two negative developments of late. The first is a clause in the new trade deal agreed at the beginning of this month between America, Canada, and Mexico that states that if any of the three intends to commence trade negotiations with a “non-market economy” then they need to give three-month notice to the others. The aim here would seem to be to limit the ability of Canada or Mexico to do separate trade deals with China.

The second development concerns the high profile speech made by Vice President Mike Pence earlier this month that amounted to a full frontal attack on China covering not only the trade issue but China’s military escalation and alleged Chinese interference in American domestic politics with Pence stating: “What the Russians are doing pales in comparison to what China is doing across this country”.

Pence also raised the Taiwan issue saying that “Taiwan’s embrace of democracy shows a better path for all the Chinese people”, while he called on Google to immediately end development of a Chinese search platform, known as “Dragonfly”, that “will strengthen Communist Party censorship and compromise the privacy of Chinese customers”.

The Pence speech adds an ideological dimension to the trade war agenda being openly promoted by Trump’s two main trade warriors, US Trade Representative Robert Lighthizer and his accomplice White House National Trade Council Director Peter Navarro. The above-mentioned clause in the new NAFTA deal, now formally known as the United States-Mexico-Canada Agreement or USMCA, bears the stamp of Lighthizer and seems part of a strategy to unite the rest of the world against China’s trade practices.

The trade warriors in Washington are also allied with the national security hawks where they are not one and the same. Their combined agenda includes both targeting China as a threat to American hegemony in the world both militarily and economically, and disrupting corporate America’s supply lines in China built up over a period of 20 years and more. Their agenda presumably also involves keeping Trump busy on doing trade deals and declaring “wins” with other trade partners while keeping the pressure on China in an attempt to isolate it. This is also presumably viewed by the Donald as a vote-winning strategy in the mid-term elections in November.

Still another point to consider is what should be viewed as the Achilles heel of the Lighthizer strategy, which seems to view China as more vulnerable economically than it actually is. In this respect, a bit of a history lesson is in order.

US Trade Warriors vs Japan

Lighthizer, who is now 71 years old, was the Deputy US Trade Representative between April 12, 1983 and August 16, 1985 during the Ronald Reagan administration. At that time he was one of the trade warriors targeting Washington’s then prevailing obsession with Japan’s huge trade surplus with America. He also shared the national security hawks’ obsession then that Japan’s economic success threatened American global hegemony, an obsession highlighted by such books as “Japan as Number One” published by Ezra Vogel back in 1979.

This obsession, and resulting pressure from the likes of Lighthizer, led to efforts at international economic diplomacy culminating in the Plaza Accord in September 1985 and the Louvre Accord in February 1987, which had the practical effect of causing Japan to ease monetary policy aggressively. This stimulated domestic asset prices dramatically, culminating in the collapse of the Bubble Economy when the Bank of Japan commenced tightening from 1989 on.

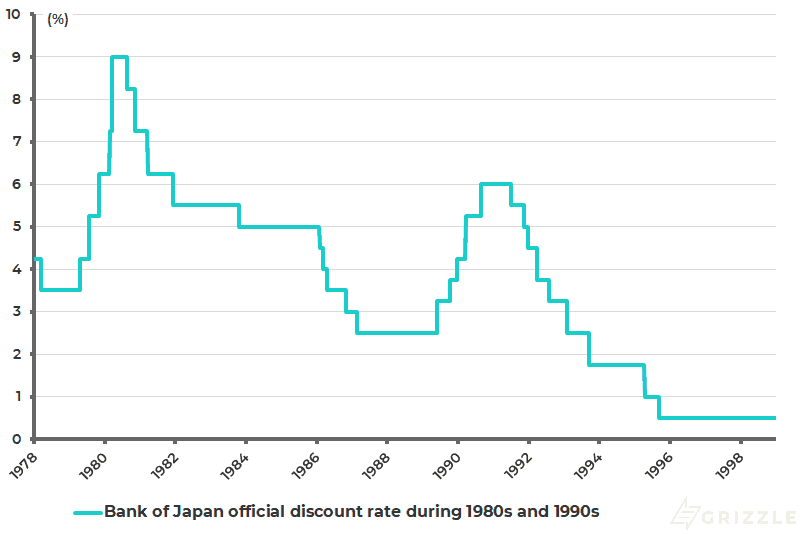

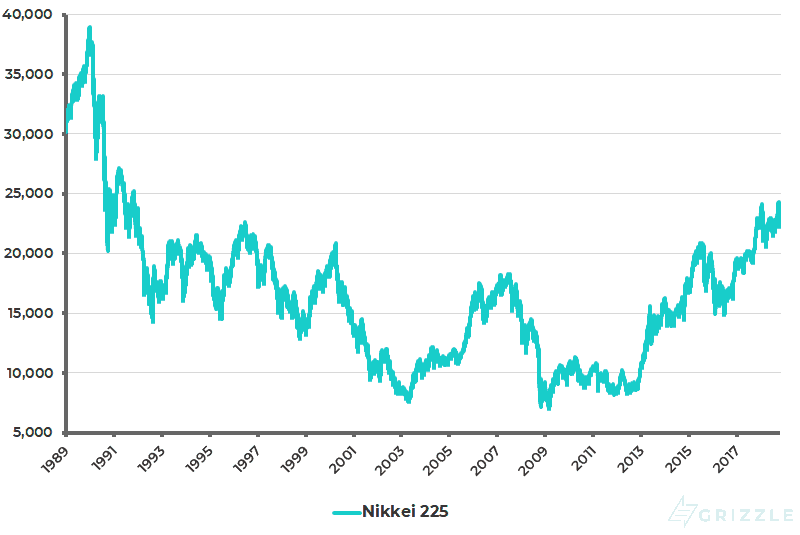

The trigger for Japan’s epic bear market was when then BoJ Governor Yasushi Mieno on Christmas Day 1989 raised the discount rate by 50bp to 4.25%, just eight days after he took over as governor. The discount rate was then raised by a further 175bp in the first eight months of 1990 to 6% (see following chart). The Nikkei 225 was 38,424 on that Christmas Day and subsequently reached an all-time high of 38,957 at the end of 1989. It has never recorrected to that level since and is now 22,532 (see following chart).

Bank of Japan official discount rate during 1980s and 1990s

Japan Nikkei 225 Index

US Didn’t Change Japan, and They Won’t Change China

All of the above is recorded because the danger is that Lighthizer and his ilk actually think their policies triggered the resulting financial implosion in Japan and the removal of any threat from Japan, if there ever was one, to American hegemony — whereas in this writer’s view Japan’s vulnerabilities were primarily domestic in nature. See book The Bubble Economy: Japan’s Extraordinary Speculative Boom of the ’80s and the Dramatic Bust of the ’90s by Christopher Wood, Atlantic Monthly Press, 1992.

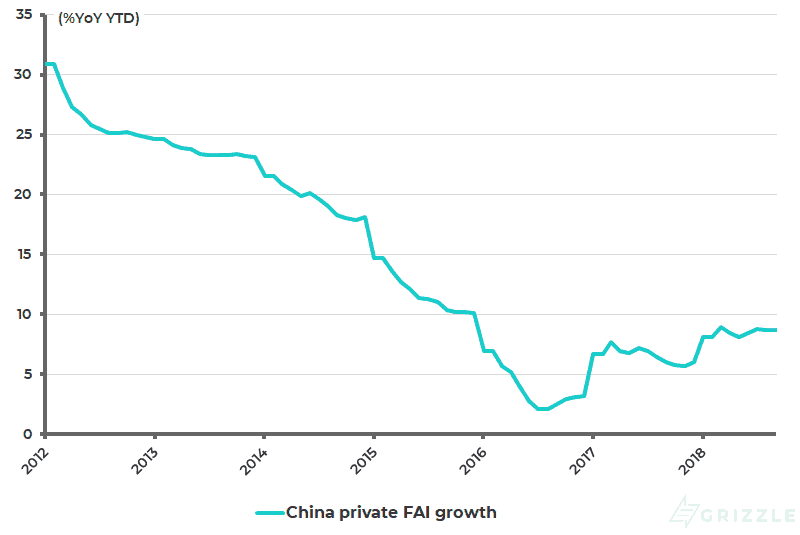

Indeed it should probably be assumed that this is what Lighthizer and those of similar views actually do think. This is suggested by continuing references from senior figures inside the Trump administration to China’s weakening economy and weakening stock market. For example, White House National Economic Council director and former Bear Stearns chief economist, Larry Kudlow, stated in August that China’s “business investment is just collapsing”.

A chart on Chinese private business investment shows it actually bottomed back in 2016 and has been turning up since (see following chart). China’s private sector fixed asset investment rose by 8.7% YoY in the first nine months of 2018, up from 2.1% YoY in January-August 2016.

China private fixed asset investment growth

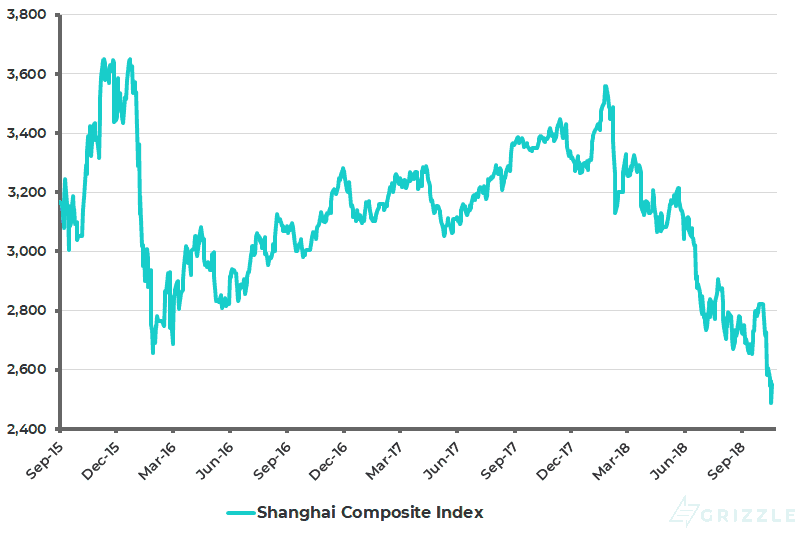

Donald Trump has been on much firmer ground with his references to the weak Chinese stock market this year. The mainland’s stock market is down 23% year to date (see following chart). As previously discussed here, the so-called A-share market has been weak primarily because of continuing collateral damage from Beijing’s deleveraging campaign to squeeze shadow banking and not because of trade war concerns.

Shanghai Composite Index

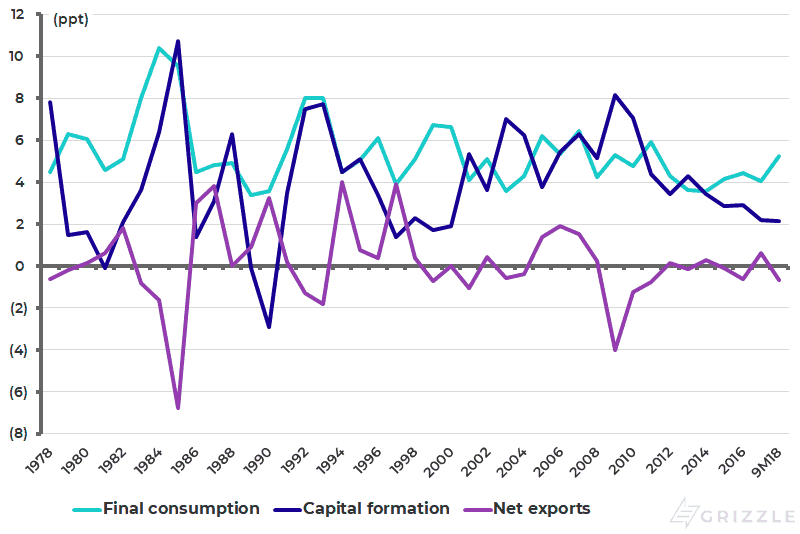

This is not to say that China will not be hurt in a trade war. There are, for example, an estimated up to 3 million people working in the Apple supply chain in China. Still the fundamental point is that China is by now a far more domestic demand-driven economy than it used to be. Net exports contributed a negative 0.7ppt to real GDP growth in the first three quarters of 2018 (see following chart). By contrast, final consumption (including private and government) contributed 5.2ppt to real GDP growth over the same period.

Contribution to China real GDP growth

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.