China will continue to be run primarily around politics not economics.

This is the chief conclusion following the end of the seven-day National Congress of the Chinese Communist Party in October.

The extraordinary, and in this writer’s view shocking, political theatre concerning former leader Hu Jintao was presumably designed to send the strongest of signals that a new era has begun.

Under the former era, growth was prioritised over all else but, based on President Xi Jinping’s view, corruption was out of control during that period and the legitimacy of the PRC had begun to be questioned.

Such a view has some merit in the sense that Xi undoubtedly remains popular among ordinary people and the party’s legitimacy was under threat.

Still for investors the formal ending of the reform era, signalled by the removal of all representatives of the Communist Youth League from the leadership, including outgoing Premier Li Keqiang and Vice Premier Hu Chunhua, can only be considered a long-term negative.

It is also not so reassuring that Xi used the Maoist-like term “struggle” (斗争) 22 times in his speech at the Party Congress.

If this is the big picture, it is also a potential concern that the major technocrats who presided over the sensible deleveraging policies of recent years are seemingly now due to retire and there is no clarity, as yet, on who will replace them.

Examples are Vice Premier Liu He (age 70), the head of the China Banking and Insurance Regulatory Commission (CBIRC), Guo Shuqing (66) and PBOC Governor Yi Gang (64).

They have all been dropped from the list of members of the party’s new Central Committee.

But being dropped from the party lists does not necessarily mean the officials will leave their government posts. This may only become clearer in March 2023, when the national legislature meets, in terms of whether they will remain or, if they leave, who will replace them.

Meanwhile, the chief characteristic of the new Politburo Standing Committee appears to be personal loyalty to Xi.

Still the new Premier Li Qiang has a track record as Party Secretary of Shanghai of being supportive of private business, though he appears to have got the number two job by demonstrating his loyalty by enforcing the ultra-aggressive Covid-related lockdown in Shanghai earlier this year.

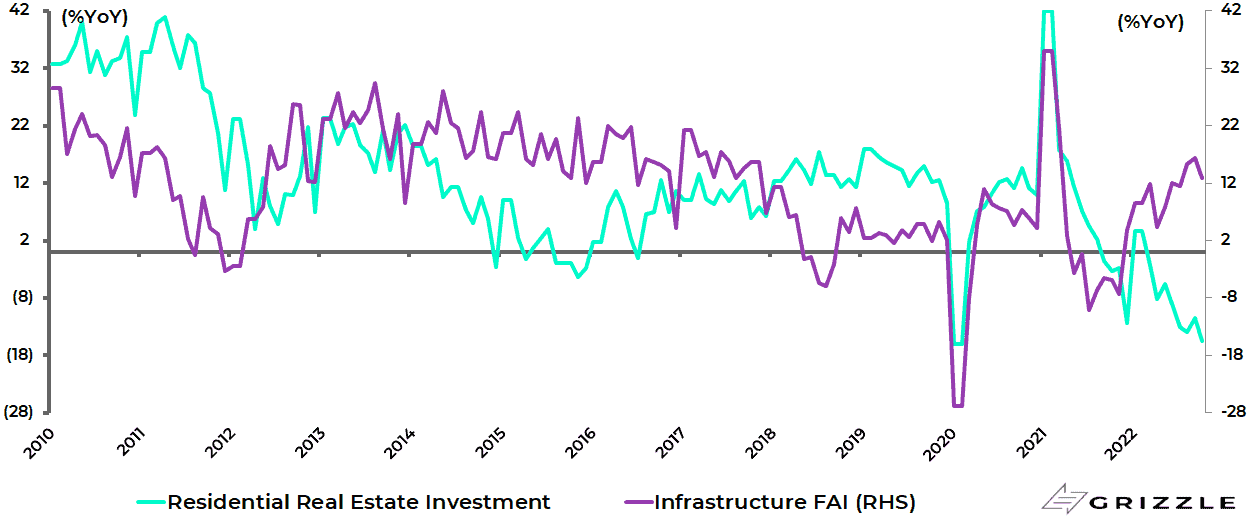

As for the economy, the latest Chinese data could have been worse with infrastructure investment providing some support, rising by 12.8% YoY in October.

China infrastructure fixed asset investment and residential real estate investment %YoY

But this is more than offset by the continuing downturn in residential property where Covid suppression remains the major driver as discussed here previously (see Can Anything Stop China’s Property Meltdown?, 23 September 2022).

The only positive is that the rate of year-on-year declines in most of the property-related data has started to moderate, save for residential property investment which fell by 15.5% YoY in October.

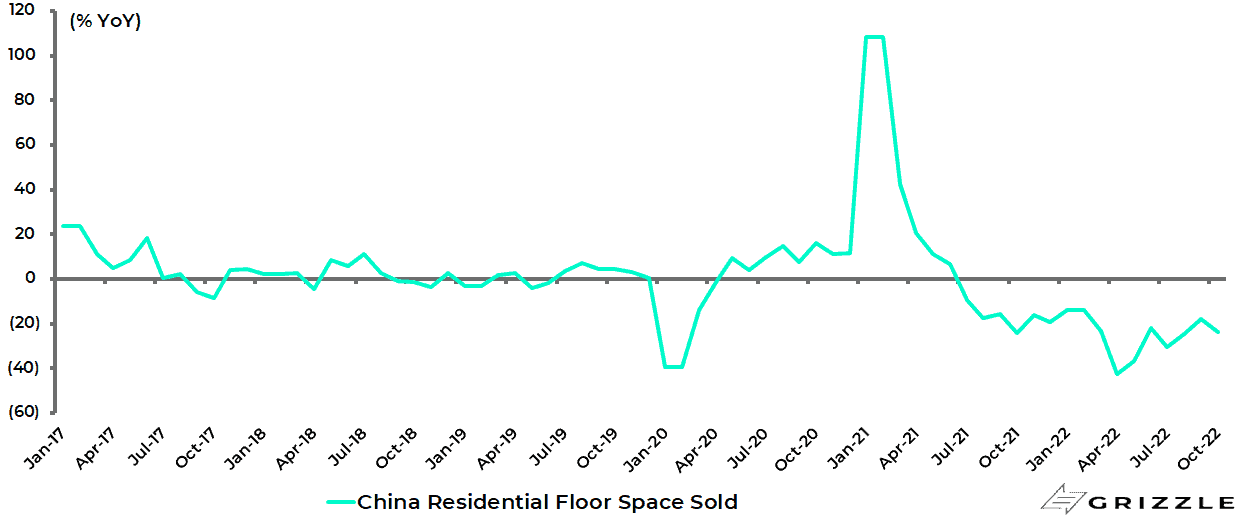

Residential floor space sold declined by 23.8% YoY in October, compared with a 42.4% YoY decline in April,

China residential floor space sold %YoY

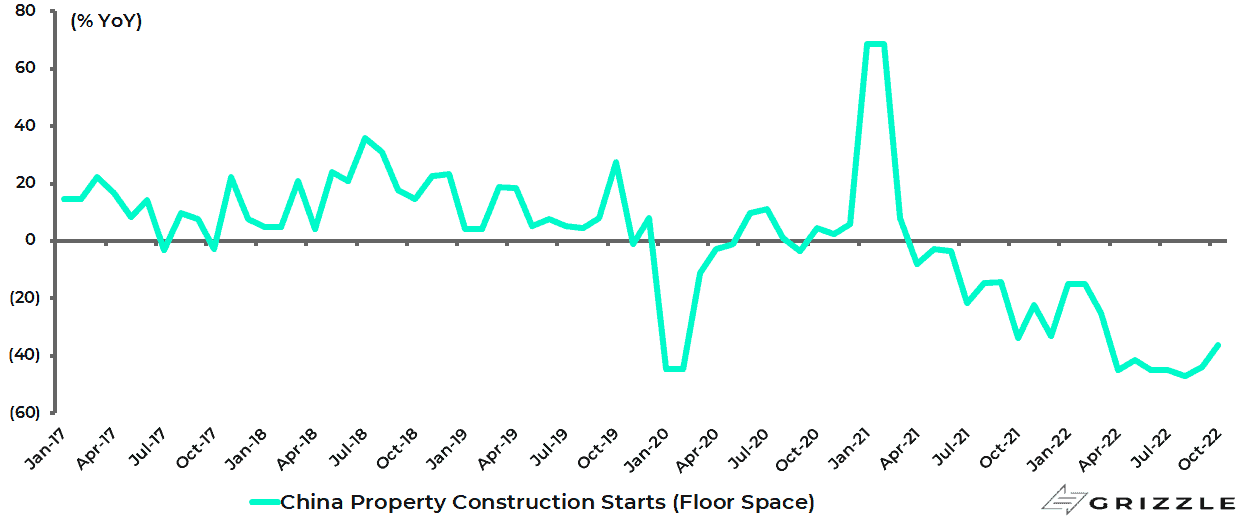

while residential floor space started fell by 36.2% YoY, compared with a 47.2% YoY decline in August.

China residential floor space construction started %YoY

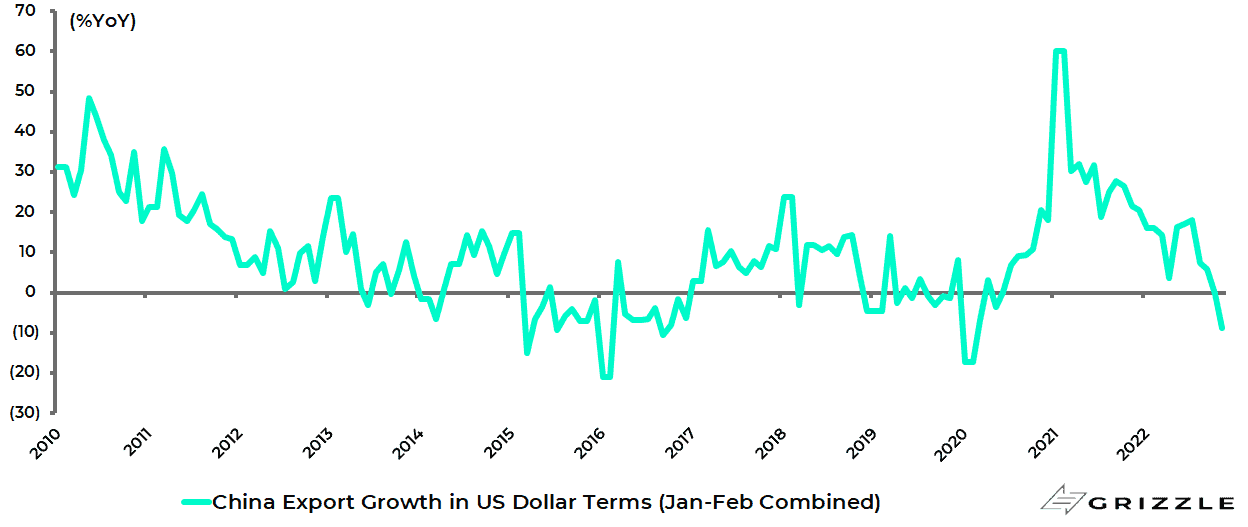

Meanwhile, exports have also clearly turned down, declining by 8.7% YoY in November, compared with 18% YoY growth in July.

China export growth in US dollar terms

Hard Landing has Been Averted for Now

Meanwhile, fears of a hard landing in China have for now been averted by the long-awaited China central government package to support the all-important residential property market, as well as growing evidence that China’s Covid policy is being relaxed in reality even if there is no formal admission of such as yet.

The long-anticipated property package, details of which were reported by the mainland media on the weekend of 13 November, three weeks after the Congress, involves an estimated Rmb1.3tn injection by the central government to ease the extreme liquidity concerns plaguing private developers.

This should largely cover private developers’ public bonds and trust products maturing before the end of 2023.

The prime aim of the package is clearly to ensure that stalled residential property projects are completed, though it is a positive for the relevant shareholders and bondholders that the authorities are helping private developers rather than getting SOE developers to take over the projects.

Will Middle Class Buyer Confidence Recover?

The key medium-term issue is now whether the property market will recover in terms of whether Chinese middle-class people, whose confidence has been shaken if not shattered, will be willing to buy flats from private developers again.

Residential floor space sales are down 25.5% YoY in the first ten months of 2022.

This will likely require more meaningful relaxation of the Covid suppression policy since the downturn in property, the steepest since China’s property market was privatised in the mid-1990s, is an unintended consequence of Covid suppression. Such a closet relaxation seems to be happening.

Meanwhile, it is worth highlighting some of the details of the rescue package.

The grace period for banks to fulfill the property lending cap requirement, a critical move to reduce banks’ concerns when they increase mortgage and property development loans, is to be extended.

China began imposing caps on banks’ property lending as a proportion of total loans at the start of 2021, capping both loans to developers and mortgage lending.

For the large state-owned banks, the ratio of outstanding property loans (including mortgages) to total loans is capped at 40% while the ratio of outstanding mortgages to total loans is capped at 32.5%.

For joint-stock banks and other medium-sized banks the same ratios are capped at 27.5% and 20% respectively, while the ratios for smaller banks are even lower.

Banks which have breached the cap will now be given extra time to meet the requirement.

Joint-stock banks were also reportedly asked to increase property-related loans by Rmb400bn in the final two months of 2022, after six SOE banks were guided in September to extend another Rmb600bn of loans.

The PBOC and CBIRC also issued a statement on 14 November giving “quality” property developers access to up to 30% of so-called “pre-sale funds” with letters of guarantee from banks.

This is the money held in escrow accounts which home buyers have paid to developers in advance of their property being completed.

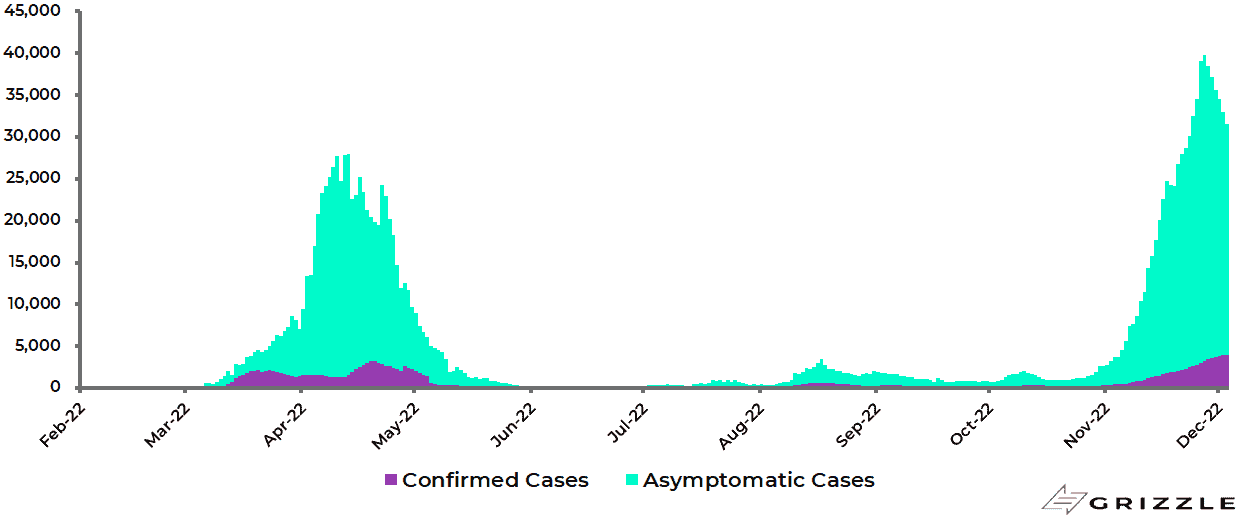

Finally, the closet relaxation as regards Covid is all the more significant because it has come at the same time as China has lost control of Covid with cases surging.

The number of daily new Covid cases surged from 719 in early October to a peak of 40,347 on 27 November though it has since declined to 10,815.

China daily new Covid cases

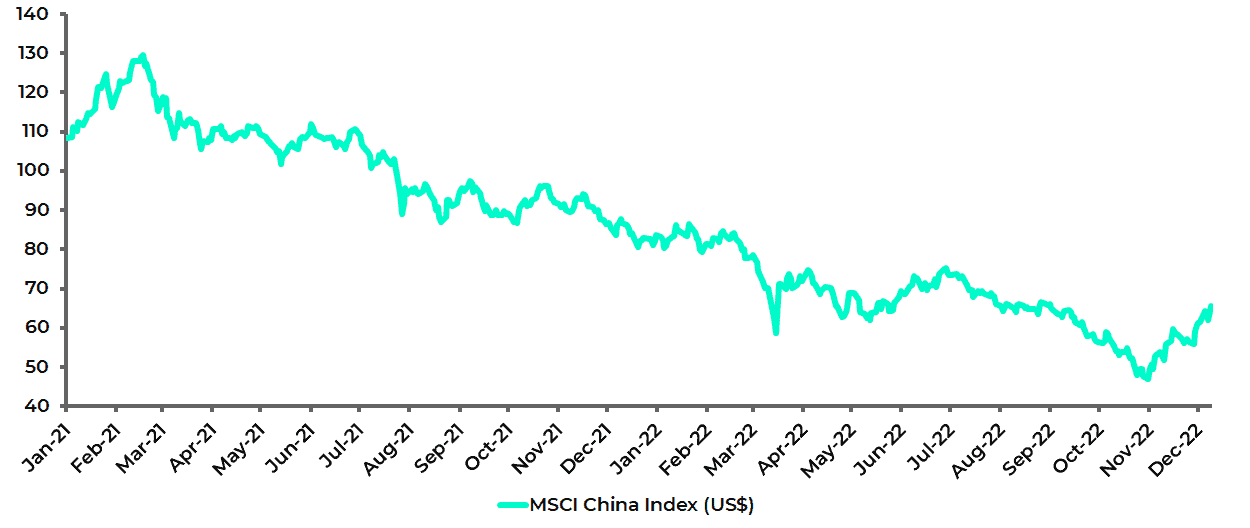

Meanwhile, the MSCI China Index is now up 26.4% since the property package was announced.

MSCI China Index

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.