One recommended trade here for global bond investors has been to sell US Treasury bonds, and indeed all G7 government bonds, and own Chinese government bonds instead.

This is so far working in 2021.

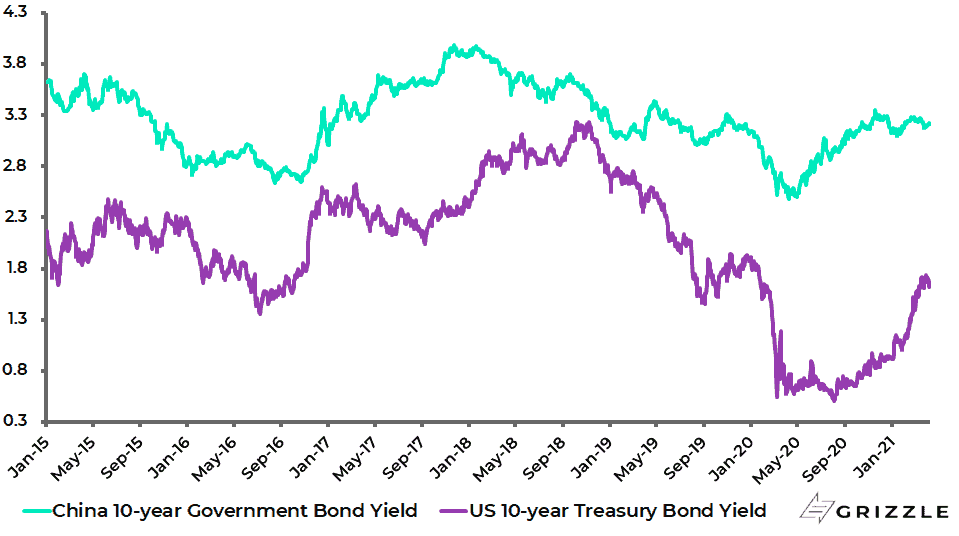

The 10-year Treasury bond yield has risen by 75bp year-to-date to 1.66% while the Chinese ten-year yield is up 7bp to 3.21%.

China and US 10-year Government Bond Yields

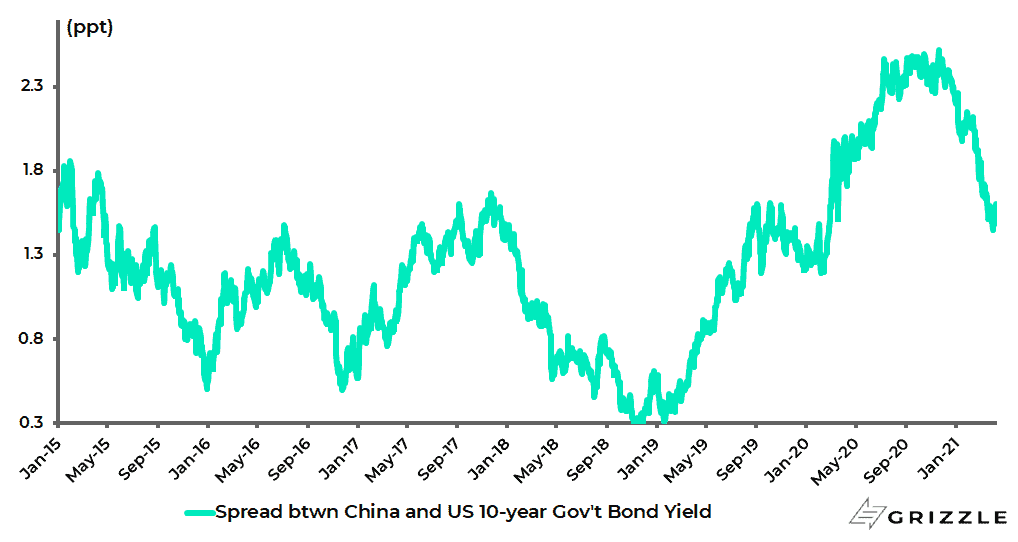

As a result, the spread between the Chinese 10-year and the US 10-year has declined from 2.23ppt to 1.55ppt.

Spread between China 10-year and US 10-year Government Bond Yields

There were two main thoughts behind this trade.

In the case of shorting the 10-year Treasury, the motive was clearly the potential for a powerful cyclical rebound in America coming out of the pandemic.

What about China?

Its bond market continues to be favoured by this writer over any government bond market globally.

This is because China remains in targeted tightening mode and eased less last year than almost any government globally in response to the epidemic, and dramatically less in the case of the G7 governments.

A reminder of the conservatism of current Chinese policy at the macro level came when Premier Li Keqiang set a target for 2021 real GDP growth of only “above 6%” at the opening of the National People’s Congress in early March.

This is way below the IMF’s official forecast of 8.4% growth for China this year.

Similarly, China also published its latest five-year plan at the NPC for the period 2021-2025.

For the first time ever, in terms of the 14 five-year plans announced by the PRC, the latest plan contains no average growth target.

Both developments highlight again that prioritizing short-term growth is no longer a priority of a China ruled by President Xi Jinping.

Rather the priority is pursuing long-term stable growth, which means managing ongoing concerns about excess leverage, as well as of course upgrading the quality of growth and ending dependence on foreign technologies. That does not mean that growth is unimportant.

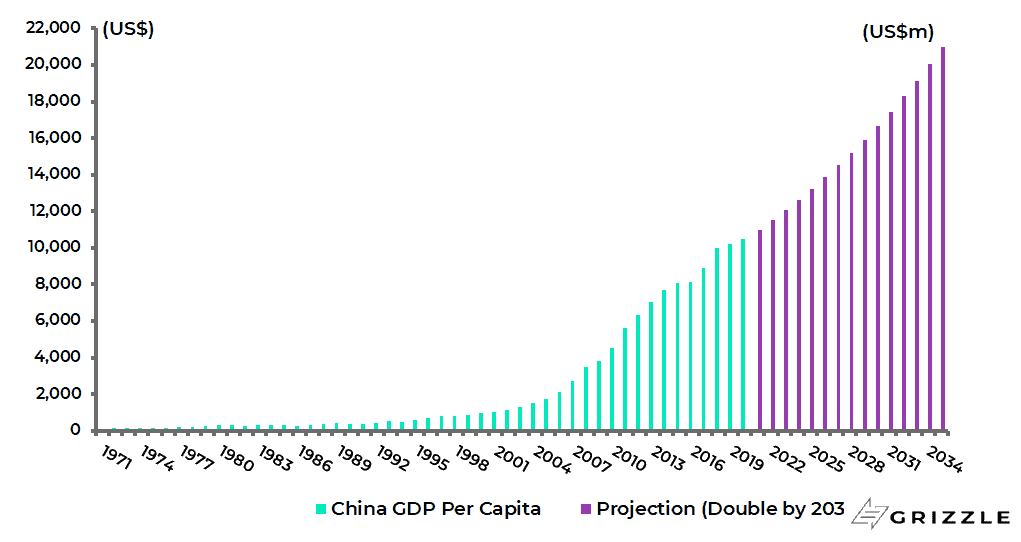

The plan’s target is for China’s GDP per capita to reach parity with so-called “moderately developed countries” by 2035.

With GDP per capita currently at US$10,500 that would suggest annualised growth of at least 4.7% to put China on a par with countries like Greece and Portugal at their 2019 levels.

This assumes China GDP per capita will double in US dollar terms to US$21,000 by 2035, a goal unveiled by President Xi last November when he said that it is “completely possible” for China to double economic output or per capita income by 2035.

China GDP Per Capita

This conservative policy stance is also reflected in the policymakers’ desire to bring credit growth back in line with nominal GDP growth this year.

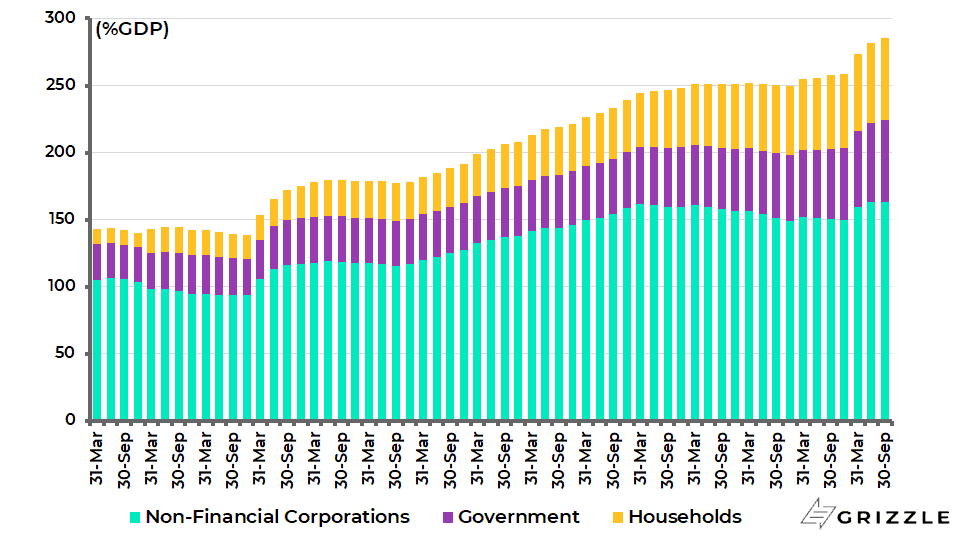

Another way of describing this is that the PBOC wants to keep what it calls the macro leverage ratio (i.e. the debt to GDP ratio) stable after the response to Covid caused an uptick in credit growth relative to nominal GDP growth last year.

The non-financial sector debt to GDP ratio rose from 259% at the end of 2019 to 285% at the end of 3Q20, according to BIS data.

China Non-financial Sector Debt as % of GDP

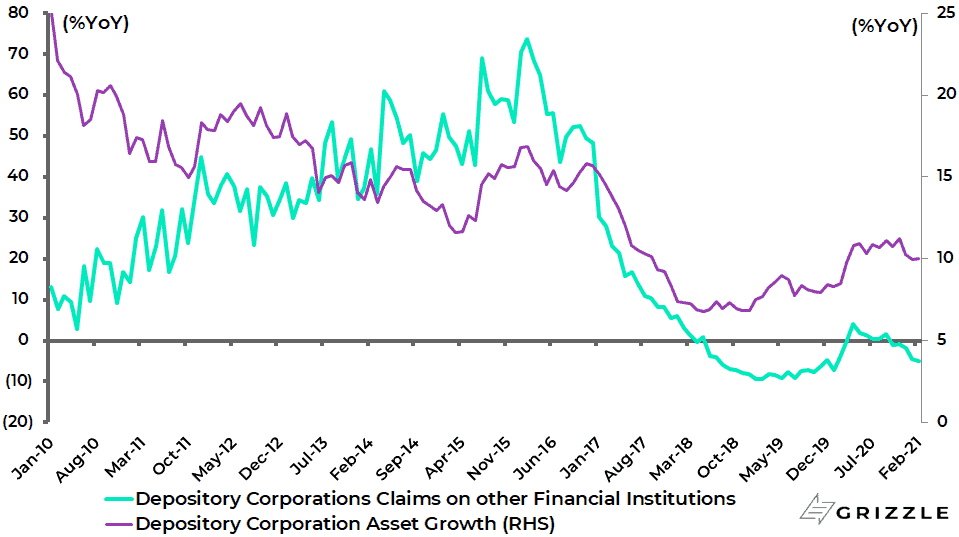

While depository corporations’ assets rose by 10.3% YoY in 2020, a year when nominal GDP increased by only 3% YoY.

Depository Corporations’ Asset Growth and Claims on other Financial Institutions

There is already evidence that this squeeze is happening.

Bank asset growth has slowed in recent months, as has M2 growth.

Depository corporations’ asset growth decelerated from 11.2% YoY in November to 10% YoY in February.

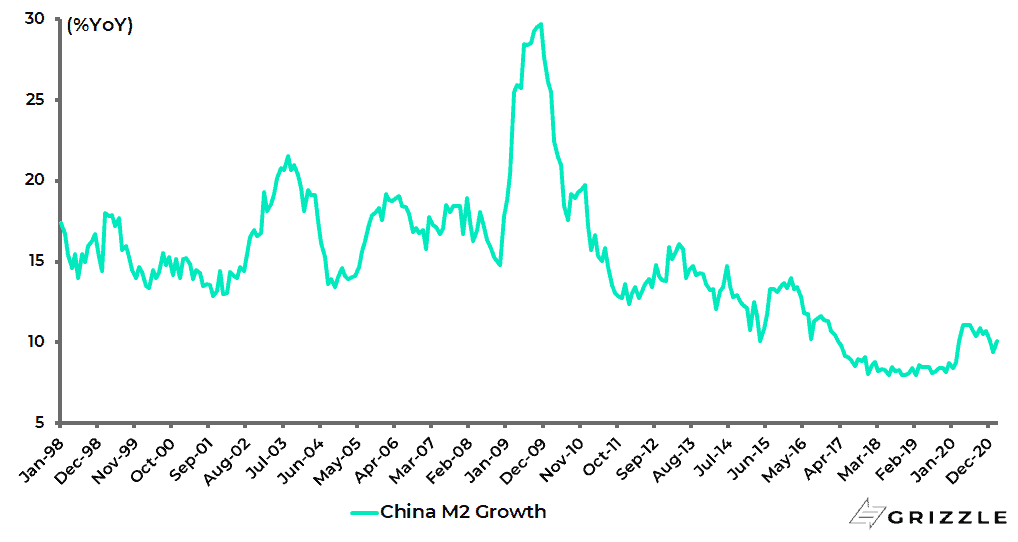

While China M2 growth slowed from 11.1% YoY in June 2020 to 10.1% YoY in February 2021.

China M2 Growth

The best proxy for shadow banking also continues to slow.

Depository corporations’ claims on other financial institutions declined by 5.1% YoY in February, compared with a 1.9% YoY decline in December.

The tightening bias is also reflected in a continuing squeeze of the residential property sector.

The official report to the NPC repeated President Xi’s mantra that “homes are for living in not speculation”.

There are two key elements of the tightening policy towards the property sector.

The first, the so-called “three red lines policy” introduced last August, has forced 12 major leveraged developers to conform to specific financial ratios.

This includes a 70% ceiling on debt to assets, a 100% cap on net debt to equity and a cash to short-term liabilities ratio of at least one. This policy was expanded to more developers in January.

The second policy is quantitative limits on property lending introduced at the start of this year.

These are significant and worth detailing here given the importance of the residential property sector in China, not least in terms of the amount of credit the sector has traditionally absorbed.

Limits were put on both total property lending and also mortgage lending based on bank size.

For the large state-owned banks, the ratio of outstanding property loans to total loans is capped at 40% while the ratio of outstanding mortgages to total loans is capped at 32.5%.

The result of these measures is that mortgage lending is likely to slow from 15% growth last year.

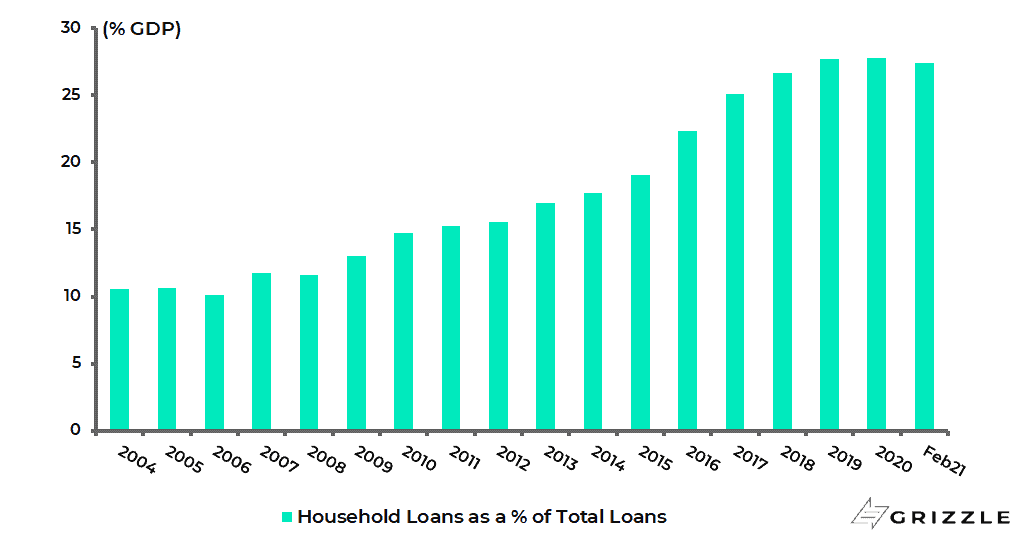

This is of macro importance since credit growth to households has been increasing faster than overall bank loan growth since 2009, and mortgages are a significant part of total household credit.

Mortgage loans accounted for 76% of total household loans at the end of 2020.

While household loans’ share of total bank loans extended has risen from 11.6% at the end of 2008 to 27.8% at the end of 2020 and 27.4% at the end of February.

China Household Loans as % of Total Bank Loans

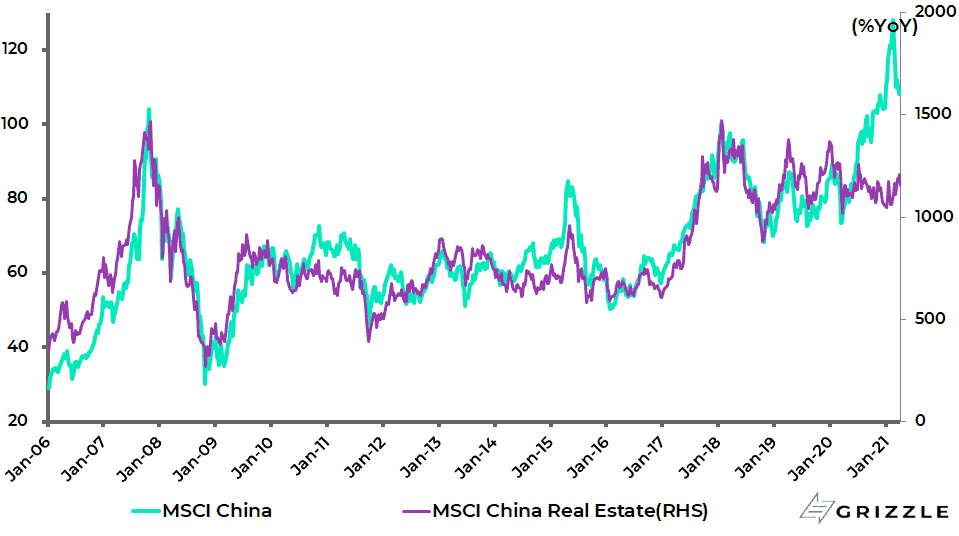

From a stock market standpoint, the impact of Xi’s desire to discourage property speculation can be seen in the divergence between the MSCI China property sector and MSCI China since early July 2020.

The MSCI China Property Index has declined by 10.8% since early July 2020, while the MSCI China Index is up 13.6% over the same period.

Historically, China stocks only rallied when property stocks were rallying.

Clearly, this has ceased to be the case of late.

The correlation between the MSCI China Property Index and MSCI China was 0.90 in the period between 2006 and June 2020, though it fell to a negative 0.34 since July 2020.

MSCI China and MSCI China Property Index

All of the above is why the biggest policy risk to the pro-cyclical back-to-normal trade this writer has been advocating for several months, a trade which clearly includes the commodity complex, remains the lack of stimulus in China.

That said, this trade continues to be advocated because of the extraordinary circumstances of the policy response to the pandemic and the resulting likely explosion of pent-up demand.

Rather the reverse is the case.

Still, there is another way to look at this.

Precisely because Chinese policy currently has a tightening bias, there is the potential for policy to be eased as the year progresses whereas the reverse applies in the G7 world where G7 central banks, led by the Fed, are still clearly underestimating the cyclical rebound potential.

It should also be noted, in this context, that the 100th year anniversary of the Chinese Communist Party will be celebrated on July 1st this year.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.