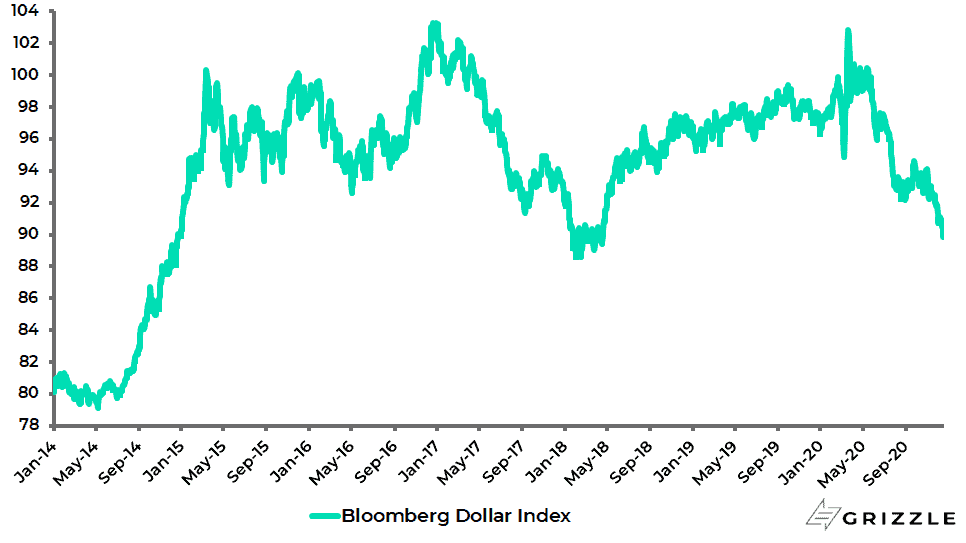

The US Dollar Index has over the past week fallen to its lowest level since April 2018.

US Dollar Index

This writer remains long-term US dollar bearish.

There remain two fundamental reasons for long-term dollar weakness.

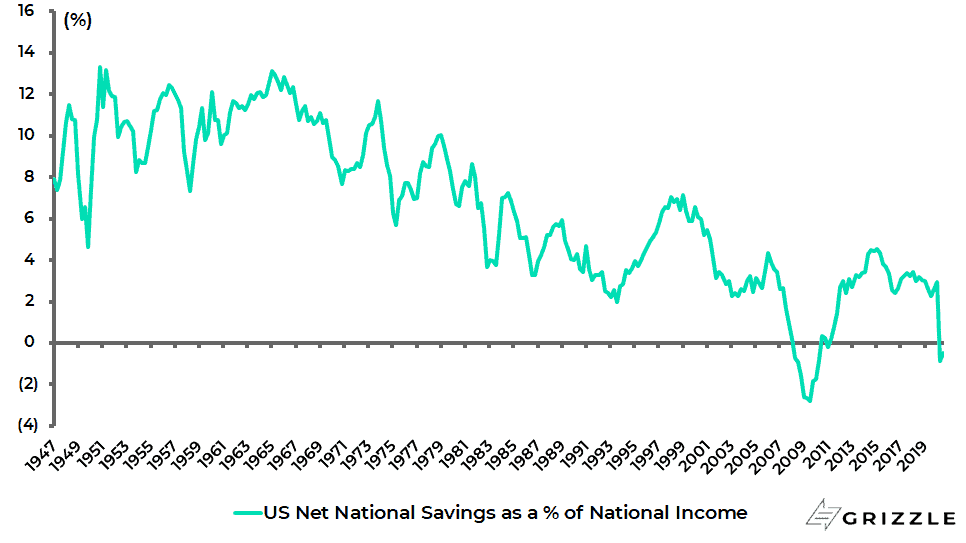

The first is the collapse in the US national savings rate.

US net national savings; measured as the sum of savings by businesses, households and the government sector, adjusted for depreciation, declined from 4.5% of national income in 1Q15 to a negative 0.9% in 2Q20 and a negative 0.5% in 3Q20.

US Net National Savings as % of Gross National Income

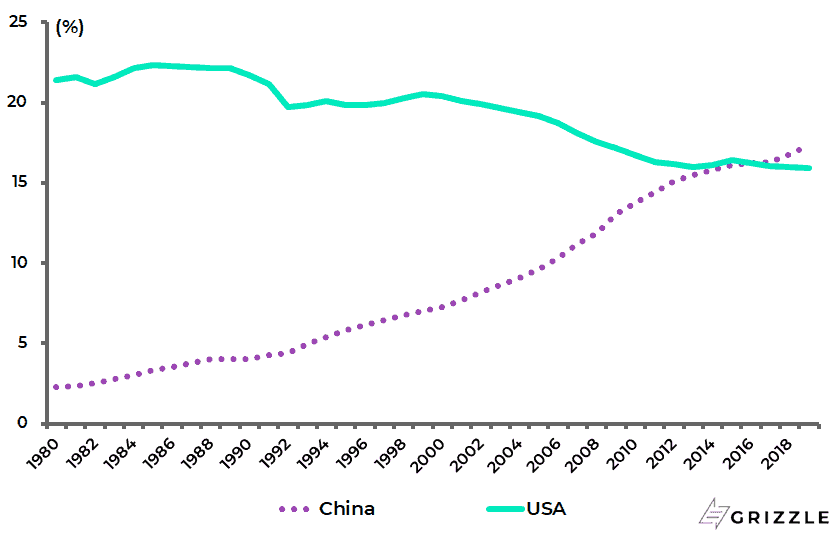

The second was highlighted in an article last month by Kenneth Rogoff (see Project Syndicate article: “The Calm Before the Exchange-Rate Storm?”, 10 November 2020).

That is what Rogoff describes as the “fundamental inconsistency” in the long run between an ever-rising share of US debt in world markets and an ever-falling share of US output in the global economy.

The US share of world GDP on a PPP basis has declined from 20.5% in 1999 to 15.9% in 2019, while China’s share has risen from 7.0% to 17.4% over the same period, according to the IMF.

US and China Share of World GDP (PPP basis)

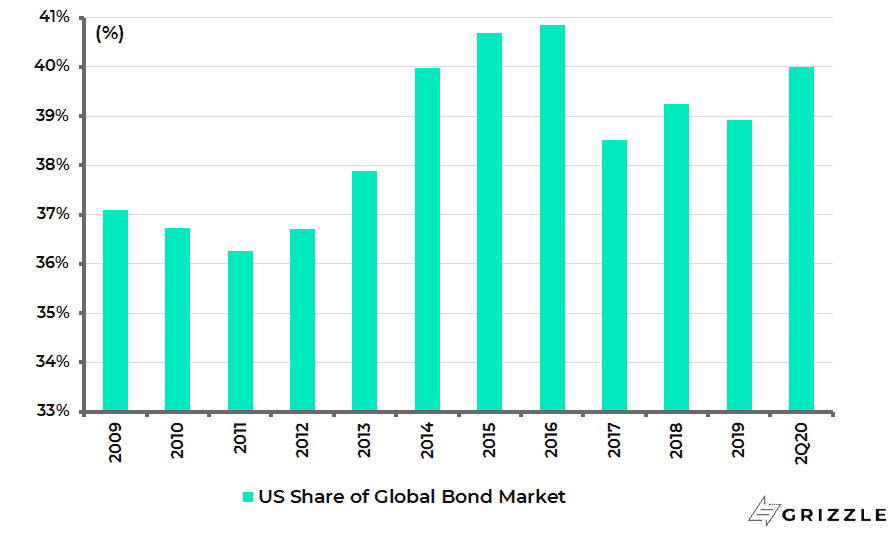

While the US share of outstanding global bonds has risen from 36% in 2011 to 40% in 2Q20, according to the Securities Industry and Financial Markets Association (SIFMA).

US share of Global Bond Market Outstanding

In this respect, China’s share of the world economy has got even larger this year because of its much greater success in combating COVID-19.

This is another reason why the advice to macro investors again is to remain long the renminbi against the US dollar, a trade that can only be further supported by any hint of monetary tightening in Beijing which is entirely possible in 2021.

The renminbi has appreciated against the US dollar by 6.8% so far this year.

China’s commitment to monetary and fiscal orthodoxy this year is paving the way for a different reference currency from the standpoint of both bond investors and central banks.

In this respect, a hint of the dollar’s diminishing status could be provided by the latest data for Swift transactions.

By contrast, the euro’s usage for global transactions rose from 31.69% to 37.82% over the same period, overtaking the US dollar as the top global payment currency for the first time since 2013.

This is an interesting development and needs to be monitored going forward.

Manufacturing Shift Out of China is Way Overblown

Meanwhile, the final weeks of the Trump administration continue to see measures targeting China.

Outgoing Secretary of State and aspiring future Republican presidential candidate, Mike Pompeo, has been in a hurry to come up with measures which, once enacted, Biden might find it hard to retreat from for fear of looking soft on China.

Still, the approach to China by the Biden administration should be much less confrontational, if only because the focus is likely to be primarily on domestic issues.

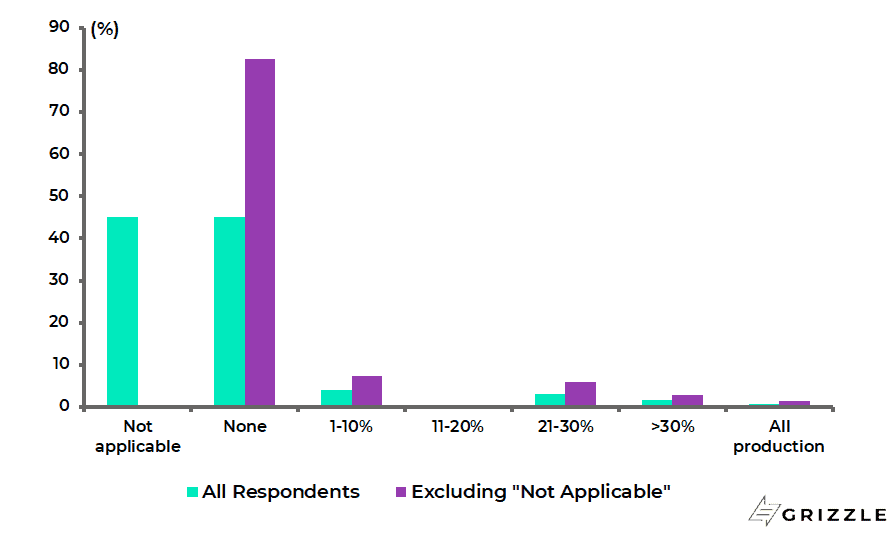

Meanwhile, a survey by the American Chamber of Commerce in Shanghai carried out after the US presidential election showed that a majority of US businesses are now feeling more optimistic about doing business in China.

More importantly, a majority of companies with manufacturing operations in China intend to keep production in the country in the next three years.

The survey, conducted between 11-15 November with 124 companies responding, showed that 82.4% of those with production capacity in China do not plan on moving production offshore in the next three years.

AmCham survey: What % of Production are You Planning to Move Offshore Over the Next 3 Years?

This is clearly of note given all the fashionable talk of production shifting out of China because of US tariffs and extended supply lines in the context of lockdowns.

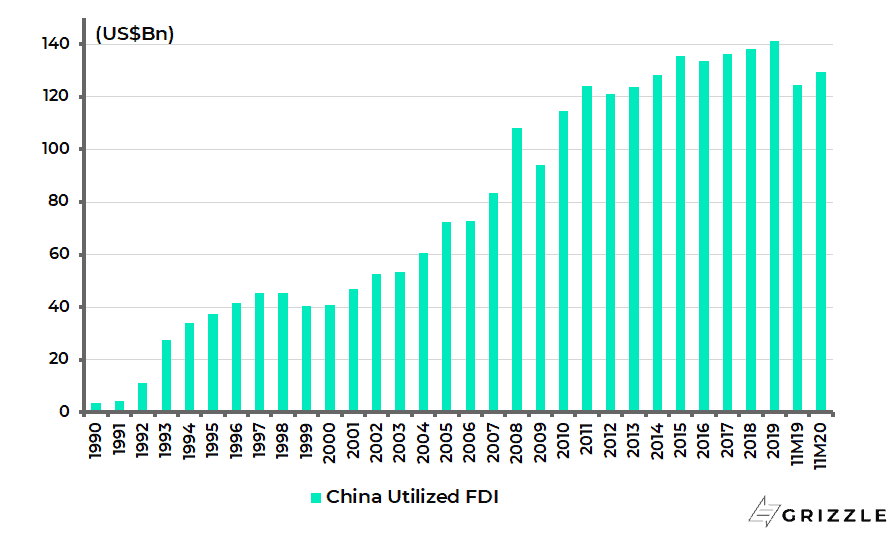

The latest Chinese FDI data is also another indication that there is no rush to shift production out of China.

Rather the reverse.

China utilised FDI rose by 4.1% YoY to US$129bn in the first 11 months of 2020, following a 2.1% increase in 2019.

China Utilised FDI

China Remains the World Manufacturing Leader

All this is a reminder that China remains at the centre of world manufacturing and has this year actually increased its share of world exports.

China’s share of annualised world exports has risen from a recent low of 12.9% in February 2019 to a new record high of 14.3% in September.

As for access to the domestic Chinese market, this will remain a focus of multinationals everywhere since China accounted for 30% of world GDP growth in 2019 and is on course, along with Taiwan, to be one of the few countries in the world to report positive growth this year.

China’s Share of World Annualised Exports and Rmb/US$ (inverted scale)

The contrast with the predictions made by the Western chattering classes in the first quarter of this year, namely that COVID-19 would trigger the collapse of the Community Party, could not be more glaring.

This is not to mention the related predictions of a collapse in the renminbi. Instead, the renminbi has appreciated by 6.8% against the US dollar year-to-date and will appreciate much more going forward.

Indeed, it is truly incredible how wrong the bearish predictions on China have been over the past 10-20 years and how stubbornly they have been maintained, with most of the prominent bears situated in America.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.