“They are on their knees.” This is a comment I heard attributed to Donald Trump, and made to another G7 leader with reference to China in Biarritz during the G7 Summit in late August. If such a comment was really made, and it is clearly quite possible, the hope must be that it reflects bravado rather than the 45th American president’s actual thought process.

For the American president’s decision in late August to increase the existing 25% tariffs on US$250 billion worth of imports from China to 30% from Oct. 1, and to implement a 15% tariff on the remaining US$300 billion of Chinese exports from Sept. 1 and Dec. 15 (up from the previously threatened 10%), seemingly made securing a deal with Beijing that much harder. This is because China will likely demand in any agreement that all existing tariffs are dropped.

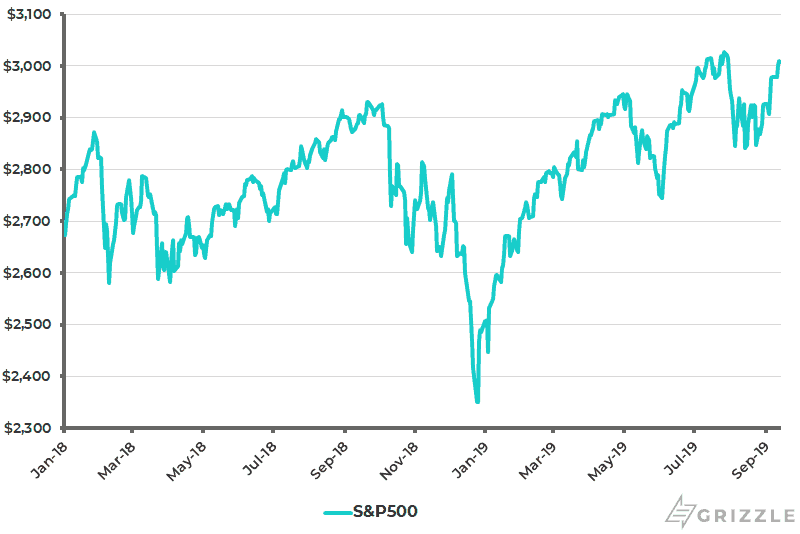

Still nothing is ever too predictable with the Donald, and of late Trump has again made positive comments about a “mini trade deal” with China. The U.S. stock market has also rallied this past week on news that U.S. and China trade negotiators will resume talks early next month (see following chart).

S&P500

Under What Terms Will China Make a Deal?

I maintain the longstanding base case here that Trump will again at some point turn on a dime and “do a deal”. The political reality is that with the American presidential campaign nearing, a choice faces Trump. Does he run as the President who secured the “best deal” with Beijing since China’s entry into the WTO in 2001, or does he give up on securing a deal and run on anti-China tweets? That his tone keeps changing in the tweets suggests he has not yet made up his mind on this critical point. Still, it should always be remembered that he likes to do deals.

Meanwhile, I continue to believe that China will not agree to any bilateral deal which includes a formal monitoring mechanism since that would in effect make Beijing answerable to the demands of a U.S. compliance officer. A multilateral deal, including the Eurozone, Japan and the rest, pegged around reform of the WTO, would be a different matter altogether. In such a context a formal monitoring mechanism based in some neutral location, such as Geneva or Singapore, would probably be acceptable to Beijing. Unfortunately, such an approach is not yet on the table. Trump’s preference has always been on the bilateral, as reflected in his obvious discomfort in multilateral forums such as the G7 Summit.

China Avoid Macro Stimulus

The Chinese government remains determined to avoid destabilizing macroeconomic stimulus despite the threat to the mainland economy posed by America’s actions. On this point, President Xi Jinping called on people to prepare for a “new Long March” in a speech in May. There has also been minimal easing in terms of the residential property market. For example, there are now about 40 cities in China, including all Tier One and Tier Two cities, where only legally registered residents can buy property.

If this commitment to macroeconomic stabilization is laudable relative to the willingness in Beijing to press the stimulus button under previous leaderships, it must be asked how long this can be maintained if the trade war deteriorates further. This is because of the obvious risk to employment in the context of China’s supply chain infrastructure.

This is why perhaps the key variable to watch in China in coming months, from a macro perspective, will be the employment data. In recent years the employment market has been supported by the boom in the service sector accounted for by digitization. Thus, a recommended IMF working paper on digitalization published in January estimated that digitalization has accounted for one third to half of total employment growth in recent years (see IMF Working Paper – China’s Digital Economy: Opportunities and Risks, by Longmei Zhang and Sally Chen, Jan. 17, 2019). This, and the demographic reality that China’s labour pool peaked several years ago has to date absorbed the job losses from China’s so-called supply-side reform and the shutting down of excess capacity.

But going forward the benign impact on employment of the e-commerce explosion has to a large extent already happened. This is why the risk to employment from a further trade war cannot be dismissed out of hand. For now it is clear that employment is deteriorating even in the official statistics.

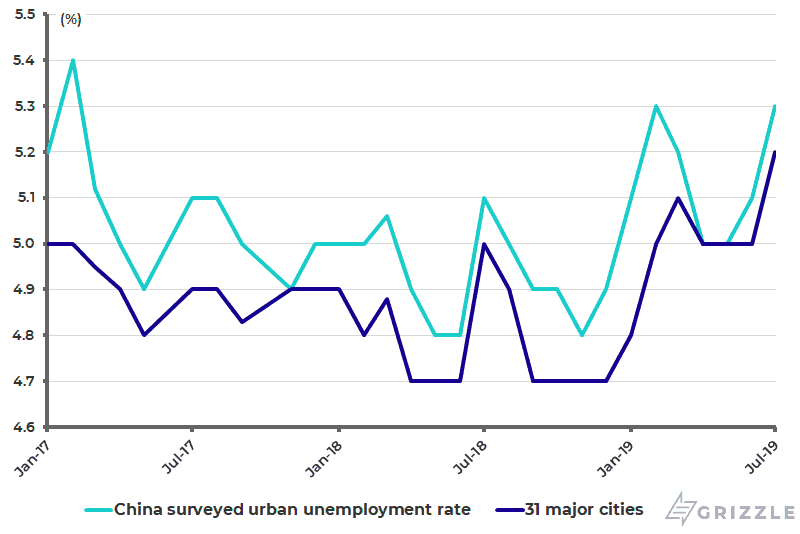

Thus, the official surveyed urban unemployment rate rose to 5.3% in July, up from 5.0% in May (see following chart). This may not look that big a deal. But that translates into a lot of jobs given the massive base effect in a country of China’s size with a working-age (15-59) population of 911 million.

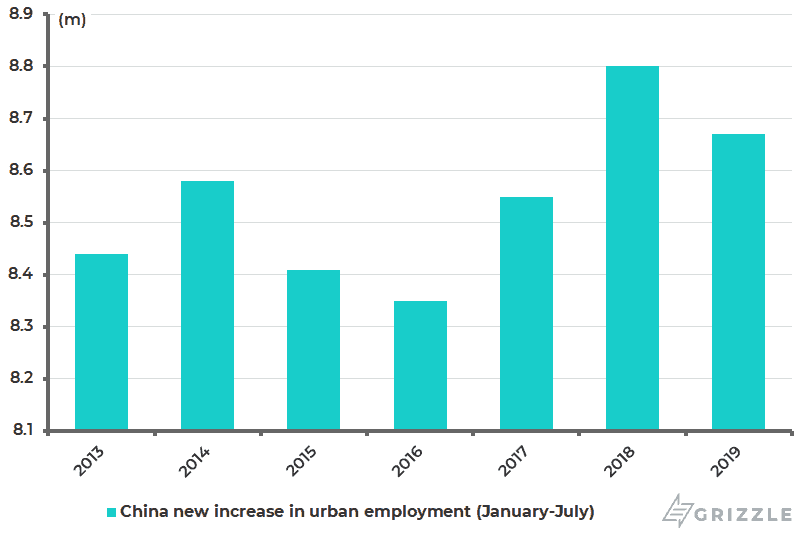

Meanwhile, data from the Ministry of Human Resources and Social Security shows that new employment in urban areas totalled 8.67 million in the first seven months of this year, or 1.5% YoY below the 8.8 million recorded in the first seven months of 2018 (see following chart).

China Surveyed Urban Unemployment Rate

China New Increase in Urban Employment (January-July)

This is an economy which has a notable lack of official labour market-related data. All this means that market driven surveys will continue to gather a lot of attention. If the labour market looks set to deteriorate further, though not dramatically so, the base case here remains that the central government will continue to refrain from aggressive destabilizing stimulus. But clearly the situation is highly fluid.

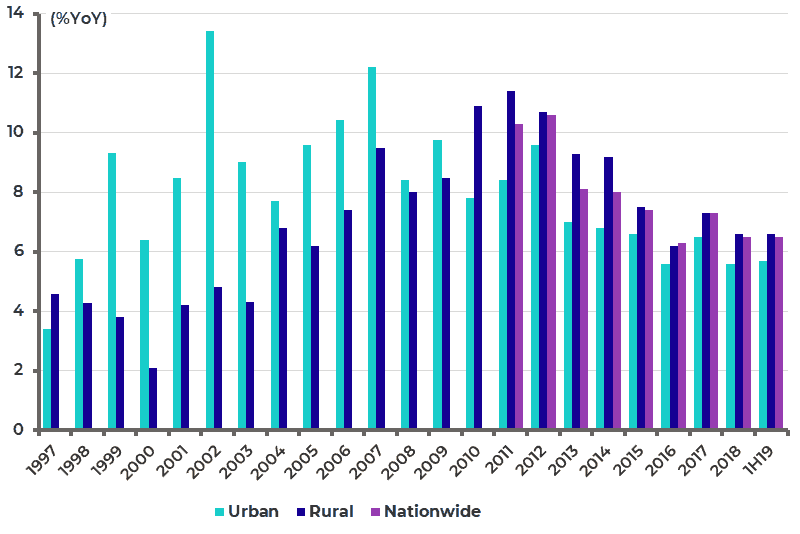

Meanwhile if employment is the key area to monitor, given the mainland government’s traditional obsession with stability, the other area is income growth (see following chart). Here again the data points to a continuing weakening trend, though far from a disastrous one. In this respect, the real income growth of urban residents is still running at 5.7% YoY in 1H19, which is healthy, though urban real disposable income per capita growth has slowed from 9.6% in 2012 to 5.6% in 2018 and is likely to slow further.

China Real Per Capita Disposable Income Growth

Still, 4% real income growth, or even 3% real income growth, for urban middle-class families is hardly a disaster. It should also always be remembered that China has the buffer of its high savings rate in the event of a protracted trade conflict. China’s household savings rate rose from 27% of disposable income in 2002 to a peak of 39% 2010 and is now 36%.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.