Whether the U.S. and China agree on a trade deal this quarter continues to dominate the market narrative. It is a little bit inconvenient that the Asia-Pacific Economic Cooperation (APEC) Summit in Chile on Nov. 16-17 has been cancelled since this is where President Trump and President Xi Jinping were scheduled to meet. Still, another venue can always be arranged.

Both China and the U.S. Do Not Want a Stronger Dollar

Meanwhile, it is intriguing that, in addition to renewed hopes of a trade deal, there has also been talk of late of a “currency pact” between the U.S. and China. True, the most recent announcement regarding currency issues was bland in the extreme. Treasury Secretary Steven Mnuchin said on Oct. 11 that China and the U.S. now “have an agreement around transparency into the foreign exchange markets and free markets” and that the U.S. will be “evaluating” rescinding China’s “currency manipulation designation”.

Is anything more significant brewing? I have no inside track, but it certainly could be. Indeed, if I were advising the 45th American president, the advice would be to negotiate some kind of currency pact with China which could also give Donald Trump a face-saving “out”; in terms of declaring victory in trade negotiations where he has clearly overestimated his leverage for the simple reason that the Chinese leadership has more tolerance to take pain than does America’s. Remember Xi Jinping’s comment in May on preparing for the new “long economic march”.

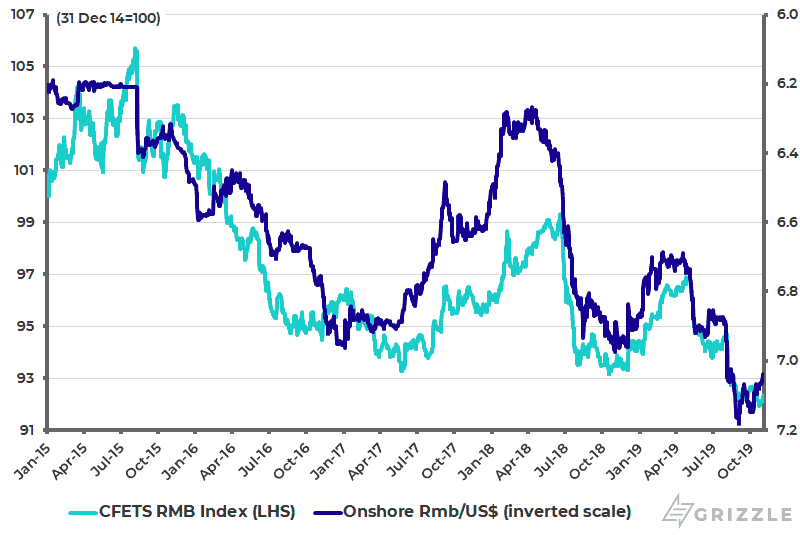

The reason the currency approach makes sense is that both Washington and Beijing want the same thing. Trump does not want a stronger U.S. dollar and nor does China’s leadership. This is why there is a potential deal whereby Beijing would agree not to engage in competitive devaluation of the renminbi against the U.S. dollar. This would be in the context of the U.S. Treasury’s continuing criticism that Beijing is a “currency manipulator” even though such a stance is more than ten years out of date. Quite how such a commitment could be made is not clear, and it could mark a change from Beijing’s current approach of the renminbi tracking, more or less, the PBOC’s trade-weighted renminbi index (see following chart).

China Trade-weighted Renminbi Index and Rmb/US$ (Inverted Scale)

How Would a Currency Pact Help China?

Still, the allure for Beijing is that such an agreement could end an escalation of the trade war and even, conceivably, end it outright if, best case, existing tariffs were removed as a consequence of any deal. One possible way forward could be a repeat of what was agreed with Mexico on the currency-related issue. The U.S.-Mexico-Canada Agreement (USMCA), signed last November, requires the signatories to refrain from currency devaluations to seek trade advantage, and also increases transparency of information sharing about government foreign exchange operations such as currency market interventions.

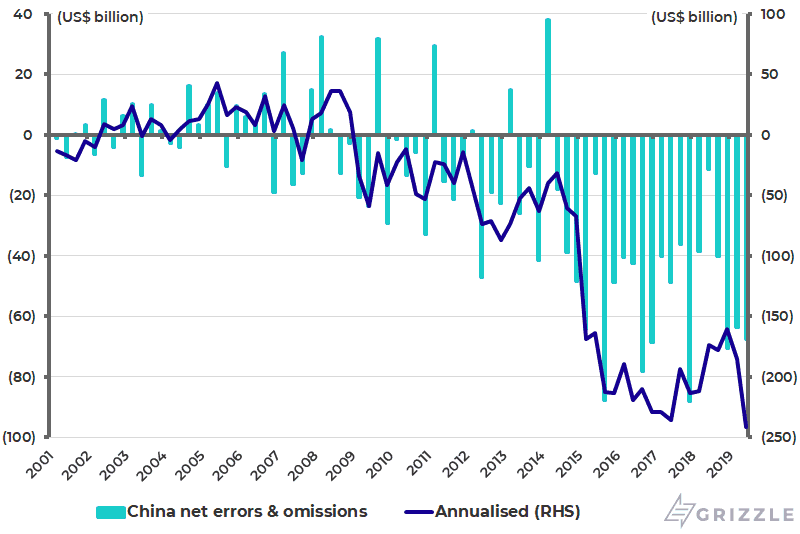

One point is clear. Beijing has no desire to see a major devaluation of the renminbi against the U.S. dollar. First, it would be very destabilizing as it would encourage accelerating capital outflow pressure at a time when such pressures are rising, as reflected in the errors and omissions item in China’s balance of payments. Thus, China’s net errors and omissions deficit rose to US$67.5 billion in 2Q19, up from US$63.7 billion in 1Q19 and a recent low of US$11.3 billion reached in 2Q18 (see following chart). On an annualized basis, the net errors and omissions deficit has now risen to a new record high of US$241.6 billion in the four quarters to 2Q19.

China Balance of Payments: Net Errors and Omissions

Second, a, say, 10% devaluation of the renminbi would make Chinese consumers ten percent poorer in U.S. dollar terms, thereby undermining the strategic role of turning China into an ever more consumption-driven economy. In this respect, it is worth restating that a central challenge facing the PRC, given the country’s demographics, is whether China can get rich before it gets old.

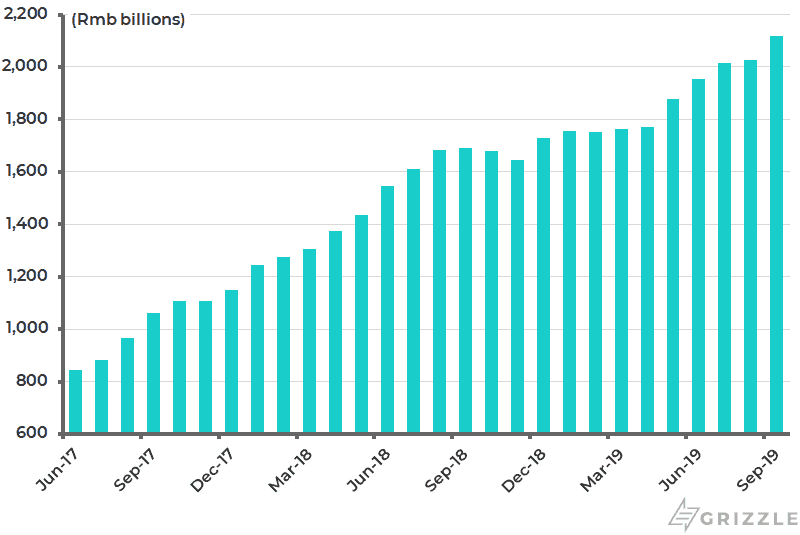

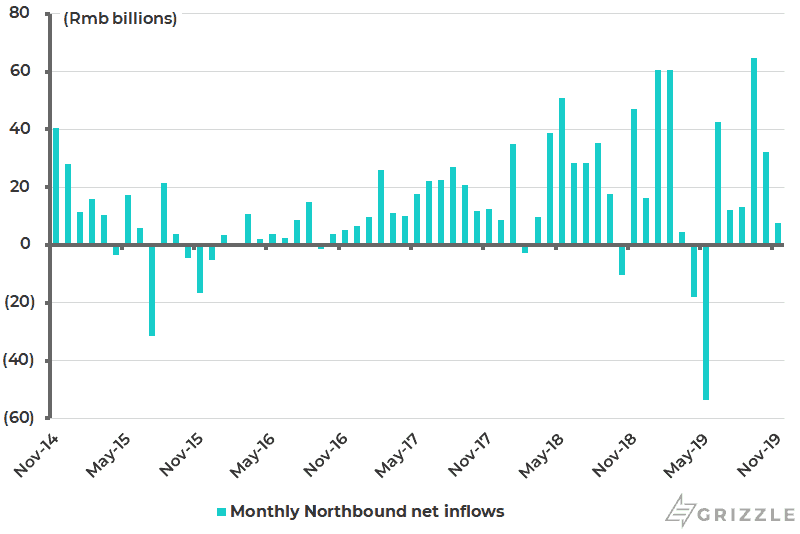

Third, a major devaluation would undermine the current successful policy of attracting foreigners to invest in China’s domestic stock and bond markets, with those inflows helping to offset capital outflow pressures. Such a dynamic has certainly been at work this year. Foreign holdings of Chinese bonds have risen by Rmb387 billion or 22% so far this year to Rmb2.12 trillion at the end of September (see following chart). As for the stock market Hong Kong, Stock Connect northbound net inflows have totalled Rmb226 billion so far in 2019 (see following chart).

Foreign Holdings of China Bonds

Hong Kong Stock Connect Monthly Northbound Net Inflows

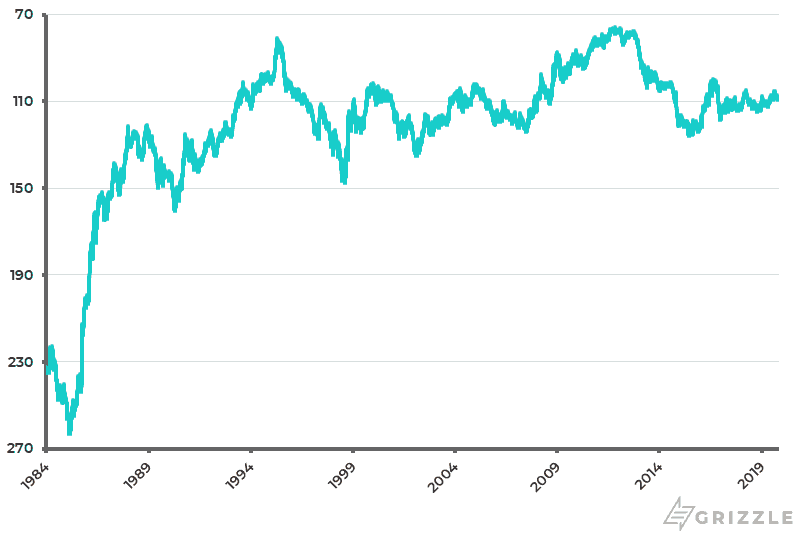

Would such a theoretical deal amount to a repeat of the 1985 Plaza Accord, as some commentators have theorized? The answer is: not really. The 1985 Plaza Accord was all about getting the yen to appreciate against the U.S. dollar. On this point, the yen rose by 101% from ¥243.6/US$ at the time of the agreement in September 1985 to ¥121.2/US$ by the end of 1987 (see following chart). However, the hypothetical U.S.-China deal would be more about stopping the renminbi depreciating against the U.S. dollar.

Yen/US$ (Inverted Scale)

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.