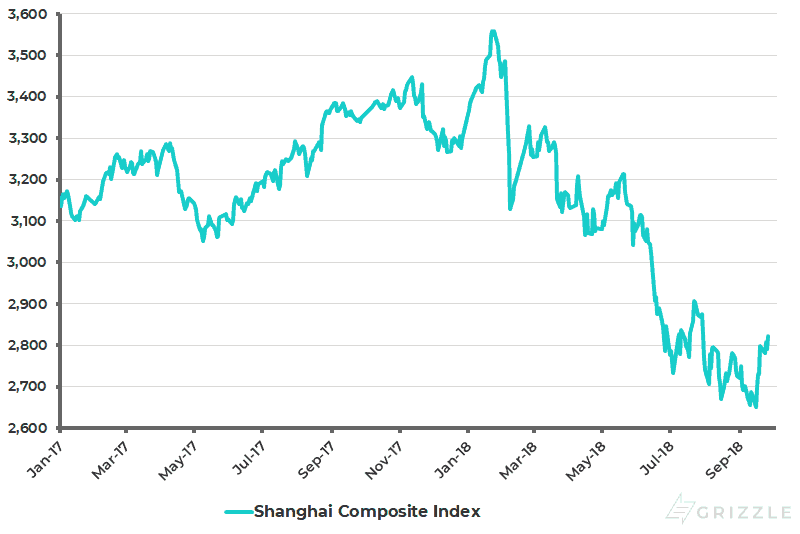

This year the Chinese stock market has been very weak with the Shanghai Composite Index declining by 15% year-to-date, and by 20% at the bottom last month (see following chart). Sentiment has been very weak among local investors, but more for reasons of domestic deleveraging than “trade war” concerns as China’s government has been squeezing the previously out-of-control shadow banking sector.

Shanghai Composite Index

Weak Chinese Stock Market and Slowing Consumption

The result is that China is the area in Asia where there is the greatest divergence between stock market action and real-world data. It is also the case that the Chinese stock market only really turned down after the authorities started targeting monetary easing in April, which is the opposite of what would normally happen. What is the explanation for this? It is clearly partly related to the “trade war” issue given that in May markets as well as Beijing were confident that a deal could be done before Trump decided to back the trade warriors in his administration and not Treasury Secretary Steven Mnuchin. But, ultra-bearish sentiment on China has returned as investors look for reasons to explain the bad performance of Chinese stocks.

Maybe such stories are true. But the base case is that this is a typical cycle where sentiment on China goes from one extreme to another and that investors should now be looking to add to China, most particularly in the cyclical area. Still, the reality is that most will be scared to do so in front of Donald Trump’s tariff announcements.

Meanwhile, one fundamental concern in China is slowing consumption. Still, so far the consumption trend does not look so weak if car sales are excluded and car sales appear to have been weak for a specific reason since President Xi Jinping announced in early April that import tariffs on autos would be reduced in July. The result was that consumers have postponed their purchases with the expectation that car prices will decline.

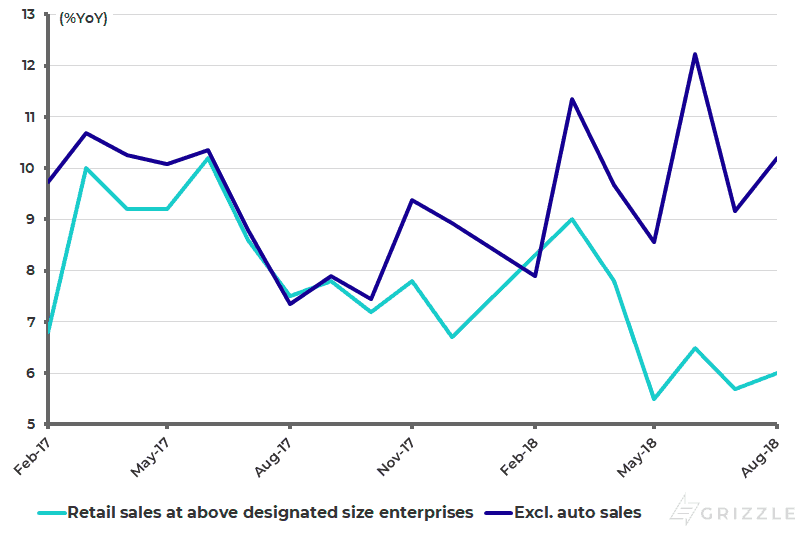

China retail sales growth at the “above designated size enterprises”, a category of outlets which have relatively larger sales revenue and account for more than one-third of total retail sales, slowed from 9%YoY in March to 6%YoY in August, with auto sales declining by 7%YoY in June and down 4.1%YoY in the three months to August. By contrast, retail sales at the above designated size enterprises excluding autos rose by 10.2%YoY in August and 10.6%YoY in the three months to August (see following chart).

China retail sales growth at above designated size enterprises

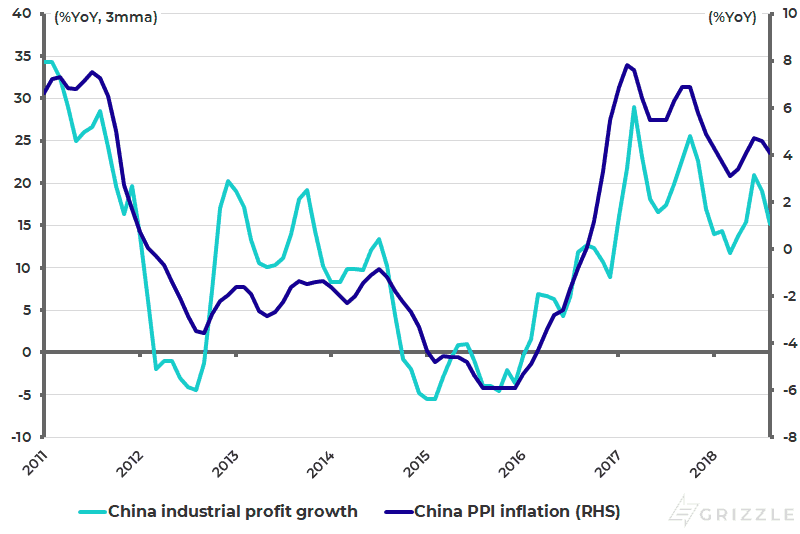

Staying on a more micro level, industrial profits were up 9.2%YoY in August and 16.2%YoY in the first eight months of 2018, which hardly looks like a disaster (see following chart). Meanwhile, Chinese stocks, excluding expensive internet names, are trading around only 7x 2018 forecast earnings.

China industrial profit growth and PPI inflation

Markets Calm Despite Capital Outflow Pressure

Meanwhile, the biggest risk in China remains what it has always been. That is not a domestic-driven collapse of the economy. Rather it is renewed evidence of capital outflow pressures. So far the markets remain calm about this despite recent US dollar strength because of the benign foreign exchange reserve data.

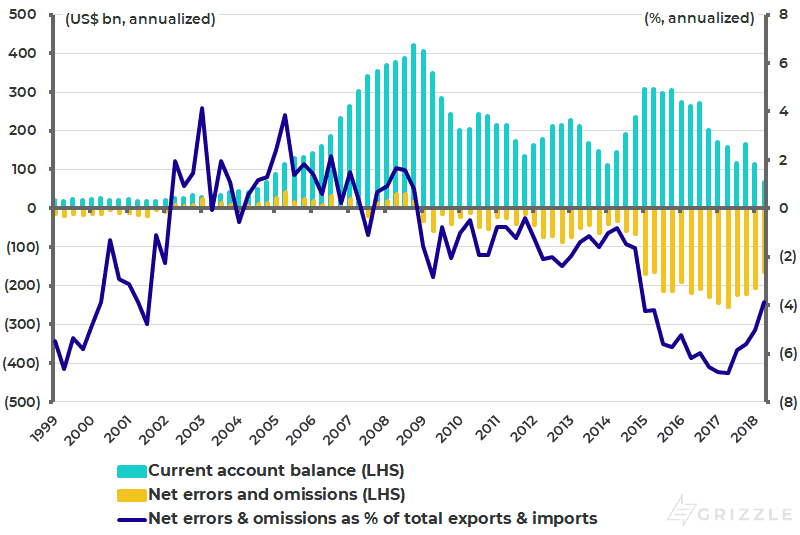

China’s foreign exchange reserves declined by US$8.2 billion in August to US$3.11 trillion, following a US$5.8 billion increase in July. This contrasts with the big declines in 2015 and 2016 when there was a renminbi devaluation scare (see following chart). Still, any renewed surge in the US dollar threatens to make life uncomfortable again since the net errors and omissions item in China’s balance of payments data continues to suggest capital outflow pressure. This is the item in the balance of payments data that does not add up.

On an annualized basis, net errors and omissions were a deficit of US$165 billion in the four quarters to 2Q18 or an annualized 3.9% of total import and exports, down from 6.8% in 2Q17 (see following chart). It is also the case that the current account surplus is in structural decline precisely because China is a now a domestic demand-driven economy. The annualized current account surplus declined from US$308 billion or 2.8% of GDP in 2Q15 to US$68 billion or 0.5% of GDP in 2Q18 (see following chart).

China foreign exchange reserves

China balance of payments: Annualized current account and net errors and omissions

It is this potential capital outflow risk, despite the closed capital account, which means China will not want to pursue an aggressive devaluation strategy in response to the Trump trade threat. For a rapidly weakening renminbi would invite capital outflow pressure. Also as a domestic demand-driven economy, China wants to preserve the purchasing power in dollar terms of Chinese consumers.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.