Chipotle Mexican Grill (NYSE: CMG) has posted their results for Q1 2020.

Revenue was $1.4B which was in line with analysts’ estimates of $1.4B

EPS was $2.70 which beat analysts’ estimates of $2.66

Some Highlights include:

- Comparable restaurant sales increased 3.3% with a 1.4% decrease in transactions including a 1.3% leap day benefit

- Through the end of February, comparable restaurant sales increased 14.4% with 10.7% transactions growth including a 2.1% leap day benefit and a restaurant level operating margin of 21.8%

- Comparable restaurant sales during the month of March were negatively impacted by the impact of COVID-19, resulting in a decline of 16.0%

- Digital sales grew 80.8% and accounted for 26.3% of sales for the quarter

- Restaurant level operating margin was 17.6%, a decrease of 340 basis points

As a restaurant chain Chipotle is expected to be hit hard by the current crisis, the company has been forced to shutter its dine-in areas, although it still remains in operation as a delivery and takeout restaurant.

The same store sales growth figure reported this quarter slowed to 3.3% growth year-over-year. For reference, in Q1 of 2019, the company posted a year-over-year same store sales growth of 9.9%.

However, it is impressive that the company has still posted positive year-over-year same store sales growth despite the entire coronavirus situation.

Investors would be very pleased to hear about CMG’s excellent liquidity at $909.2 million in cash, restricted cash, and short-term investments as of March 31, 2020 and no debt.

CMG has withdrawn its previous guidance for fiscal 2020 and has not issued any new guidance in light of the current situation of the COVID-19 outbreak and increased economic uncertainty.

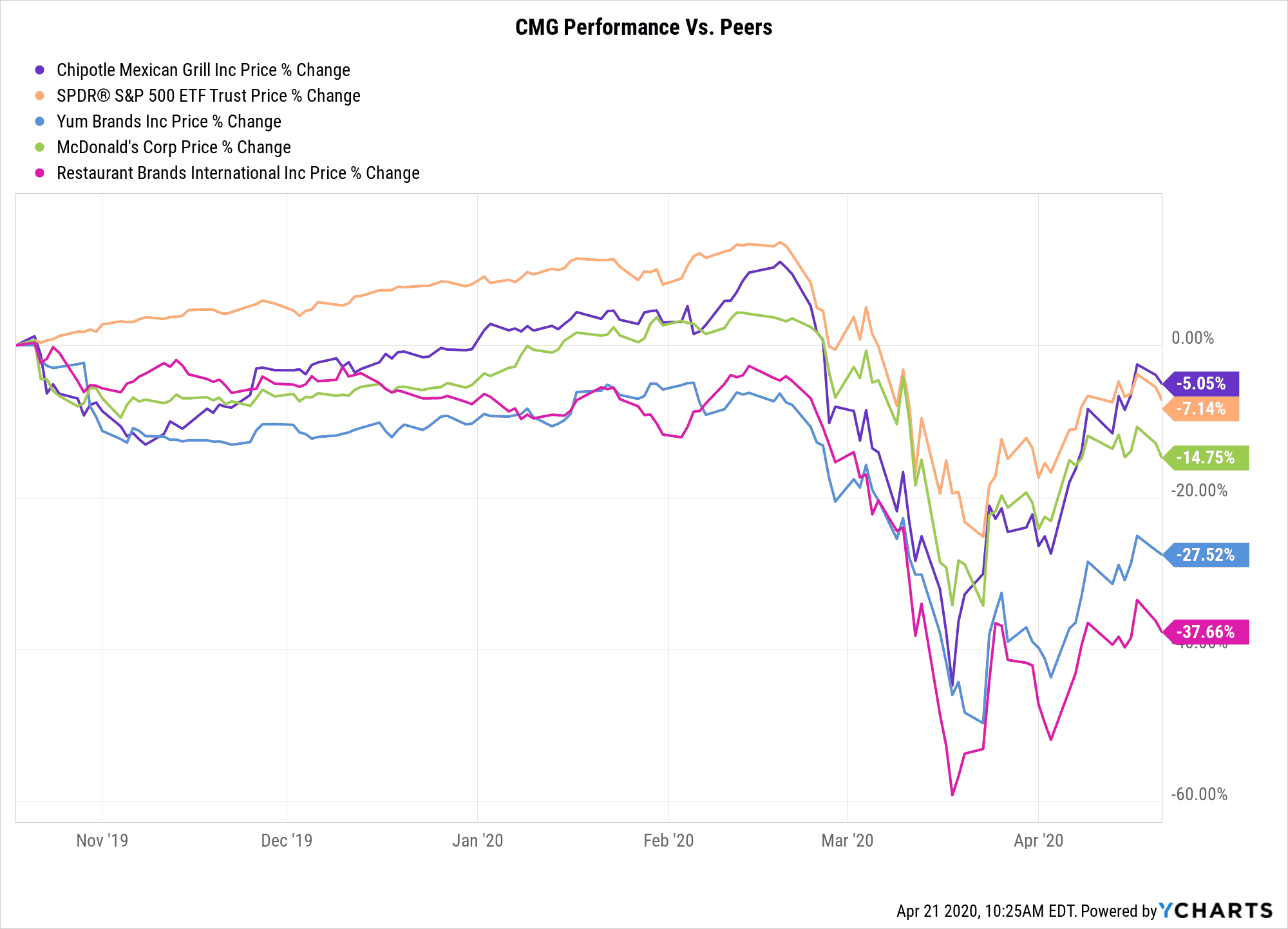

The stock is also priced like a champion, outperforming many major peers in the food industry as well as the S&P500 over the past 6 months.

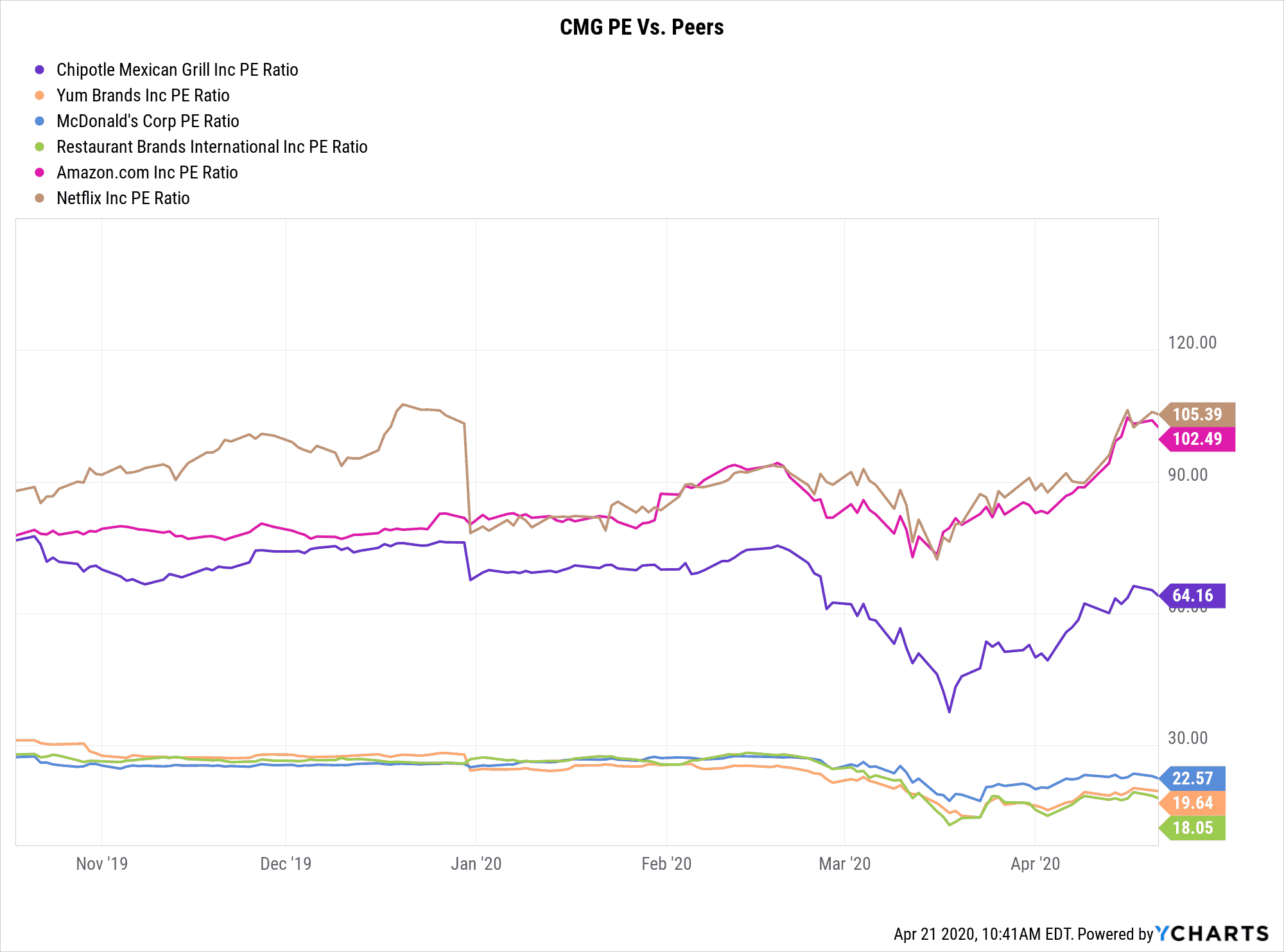

Chipotle Is Priced Like a Tech Stock

Looking at the valuation of CMG versus other restaurant chains, it looks like from a trailing P/E basis, CMG is more similar to a big name tech company than it is to the other restaurant chains.

As evident by its valuation, CMG is one of the most beloved stocks on Wall Street.

This is mainly due to Chipotle’s high growth rate and good reputation among consumers. Although the company has struggled with a few health scares way in its past, it seems like CMG has been able to shake these concerns and regain the trust of consumers.

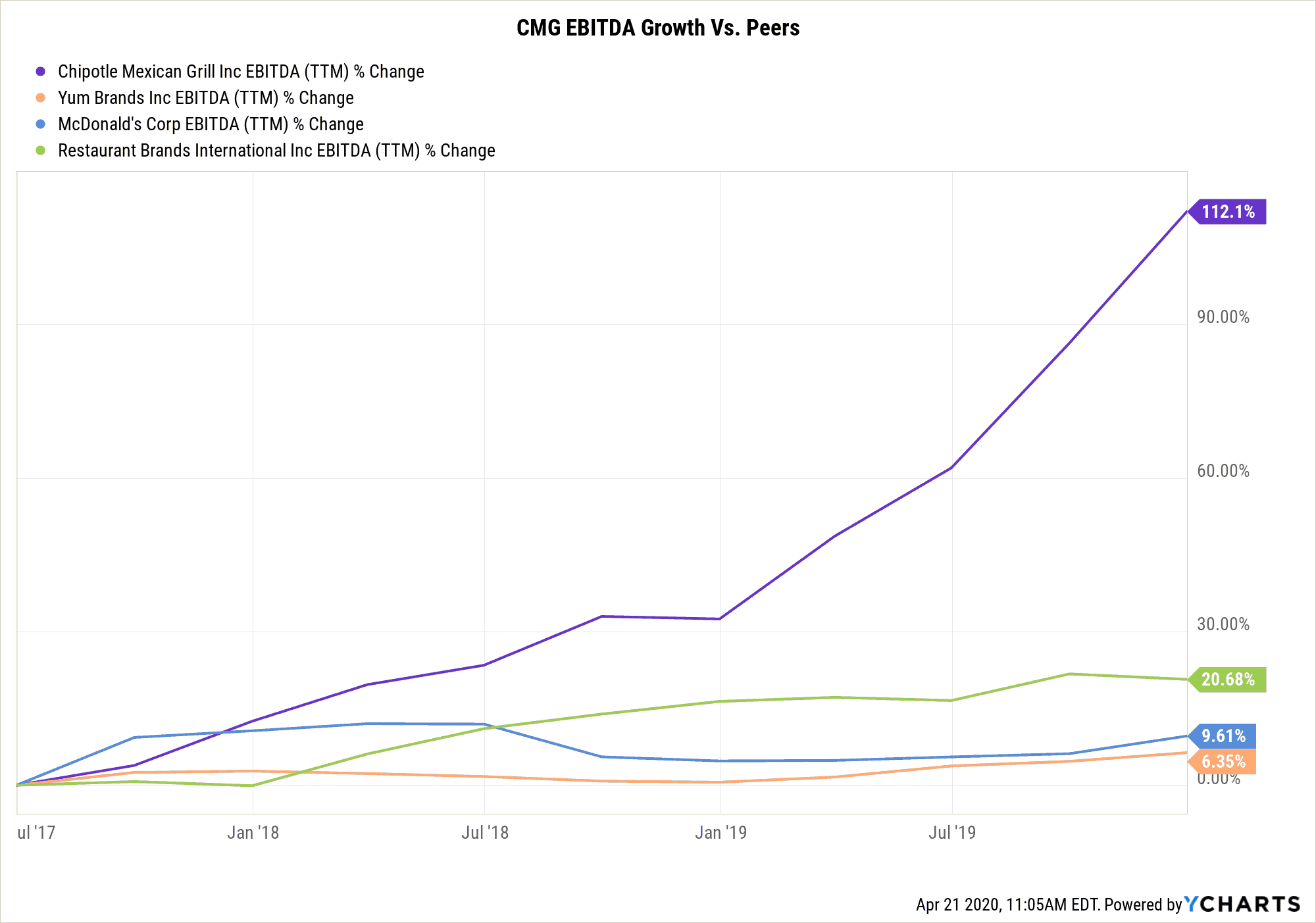

Elaborating on Chipotle’s high growth rate, we can see that on a TTM basis for the past 3 years, Chipotle absolutely wipes the floor with its major peers in terms of EBITDA growth.

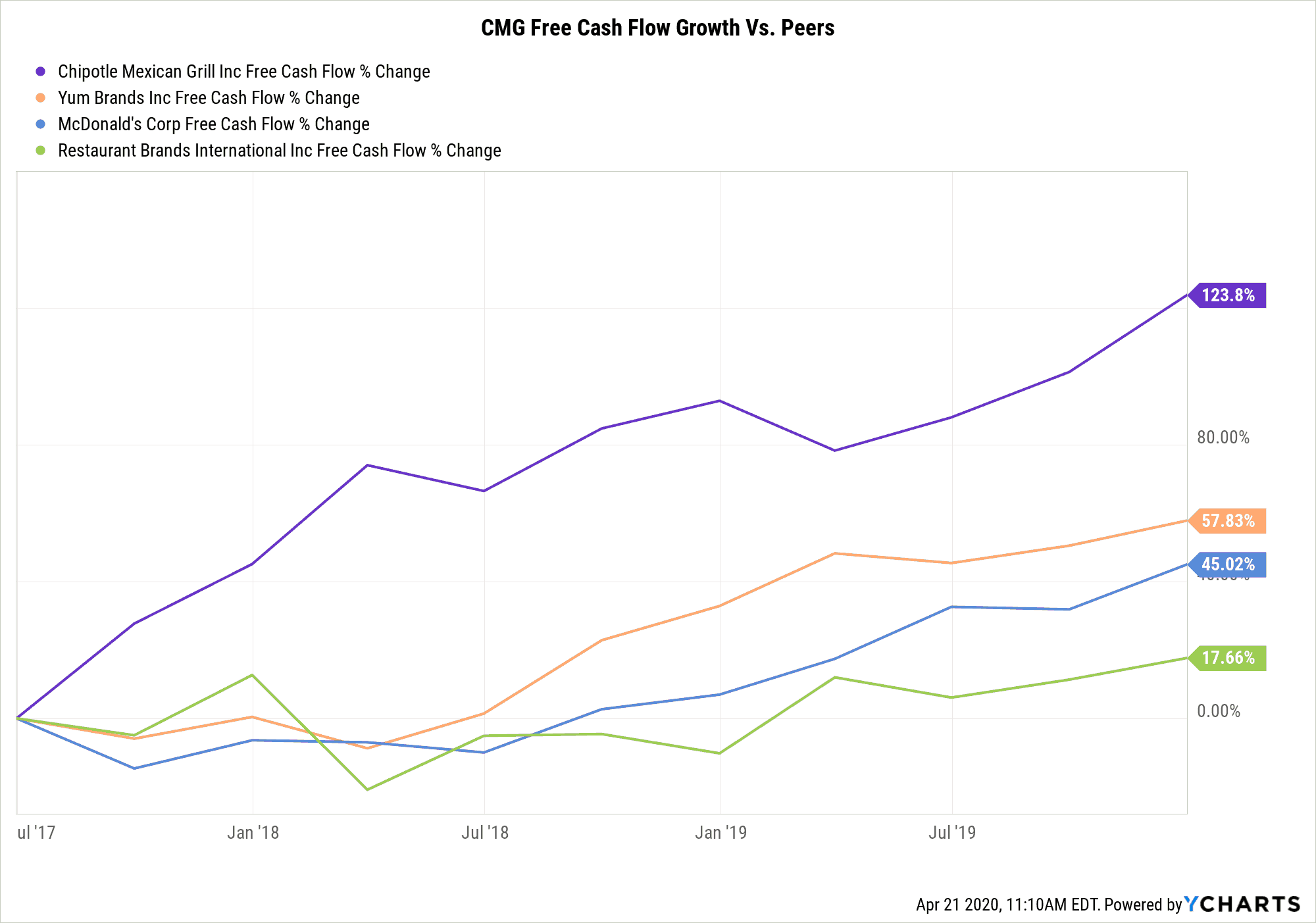

Although CMG’s free cash flow of $387M in fiscal 2019 seems small by comparison to other companies like McDonald’s who boasts over $5B of free cash flow during the same period, CMG’s growth in free cash flow once again blows its peers out of the water.

Chipotle has received widespread endorsement such as from big investment firms like Goldman Sachs who stated that the company is bound to benefit from its strong “footprint across digital and delivery”, and also poised to take advantage of the US economy opening back up once that gets implemented.

Famous CNBC pundit Jim Cramer also said during the lighting round on his show, that “ Chipotle’s good if you can get it under $800,” crediting CMG’s strong balance sheet which states that the company has almost $900M of cash with a current ratio of about 1.6

With all this good news, is CMG a ‘buy’?

Although CMG consistently outperforms its peers in the fast food restaurant space, it will no doubt suffer significant business declines that are disproportionately larger compared to other “stay at home” stocks in industries that thrive online.

At the time of this writing, CMG trades at around $780/share, which is not that far off from its all time highs back in February of around $900/share, which was before the full extent of the pandemic was clear.

Factoring the risk of the global pandemic coupled with CMG’s high valuation, the valuation just seems too frothy and it definitely seems like there are other better deals on the stock market currently.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.