Cisco Systems (NASDAQ:CSCO) reported their earnings for Q2 2020.

Revenue was $12.0 billion which was in-line with analysts’ expectations of $11.98 billion.

EPS was $0.77 which is roughly in-line with analysts’ expectations of $0.768.

Overall it’s been a volatile year for the stock. The stock hit the high 50s range in summer of 2019 before quickly crashing back down to its current levels of around $49 per share, which is right around where the stock traded this time last year. Investors were unsettled by its past couple of earnings reports which showed slowing sales and repeated guidance cuts.

A War on Too Many Fronts

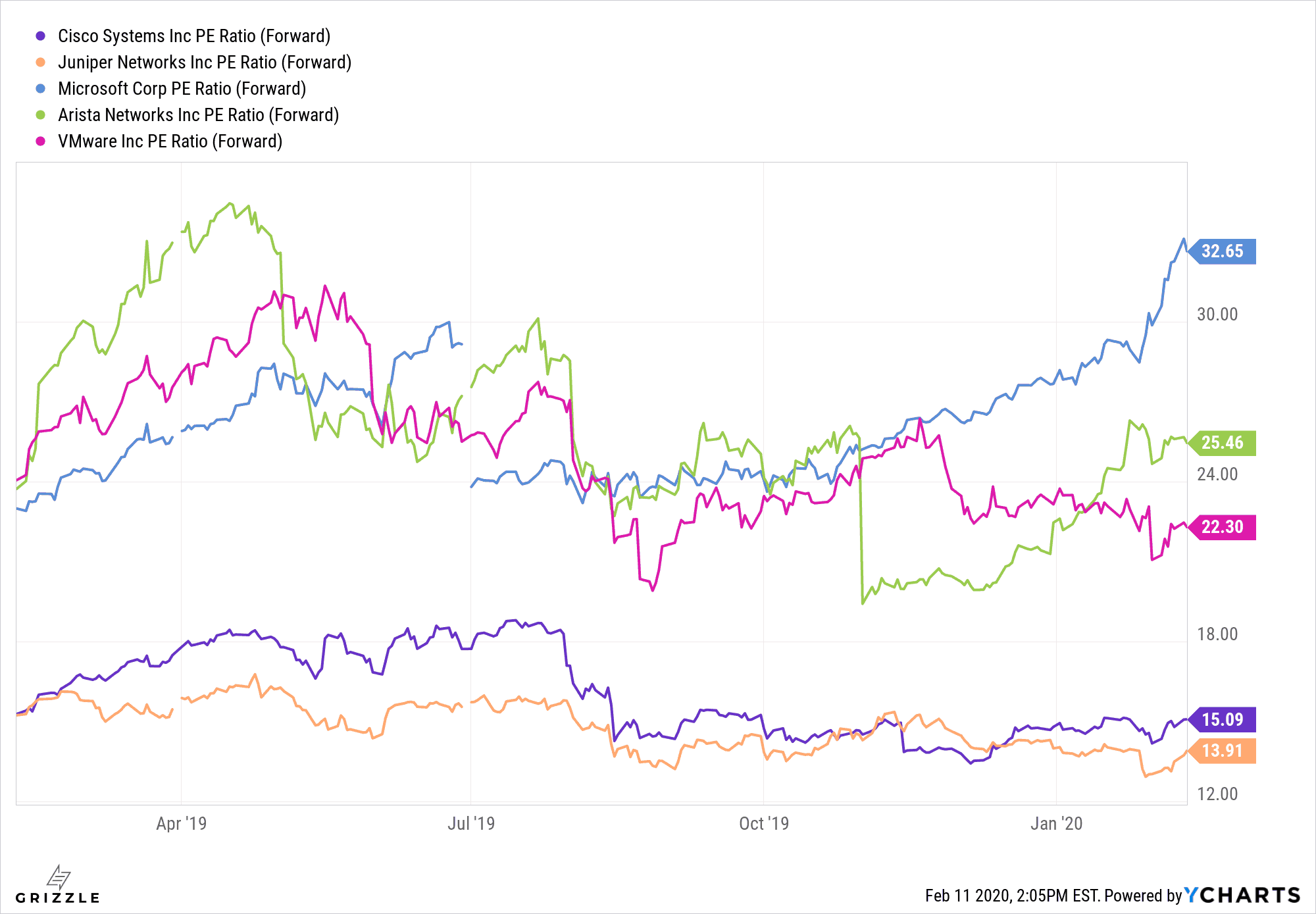

The main reason that analysts have cited for the stock’s lacklustre performance is increasing competition from the following companies: Juniper Networks, which competes with Cisco on routers and network security; the Chinese behemoth Huawei, which competes with Cisco’s telecommunications technologies; VMWare which competes on cloud computing and virtualization; and even companies like Microsoft which compete on instant messaging services.

Not to mention Zoom Video Communications (NASDAQ: ZM) which does video conferencing and just had their IPO last April and has quickly become the favourite conferencing platform among younger and smaller companies and beating out Cisco’s WebEx which has been the long-time favourite. To add insult to injury, Zoom even poached the CFO of Cisco’s WebEx division to be their own CFO.

It seems like Cisco is simply fighting a war on too many fronts and not doing particularly great on any of them. Cisco is still a huge company with boatloads of cash ($28.04 billion of cash on hand with $19.64 billion of total debt) so in the short term they are not in any immediate trouble.

However, if this trend of being out-competed continues, it may spell trouble for the company down the line. Cisco needs to find one or two business segments that they can truly excel above the competition and use their huge cashload to bulldoze through.

Cisco Looks Cheap, But Growth Remains A Concern

Source: ycharts.comCisco looks cheap at this levels with one of the lowest forward P/Es in the industry. According to SeekingAlpha, Cisco stands at a forward P/E difference to sector of -35%. However, it is still too early to tell whether or not the company has turned the corner and whether they can experience good growth again.

On a Year-over-Year (YoY) basis, revenue has only grown by 3.43% compared to the 6-7% YoY revenue growth that is typical in this sector. Right now it seems like growth is stagnating and the stock price has suffered as a result.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.