Cresco Labs (CNSX: CL), released second-quarter fiscal 2020 earnings today that exceeded street estimates.

The company’s revenue came in at $94.3M, almost 25% above analyst estimates of $75.81M.

The 42% quarterly growth rate was the best in large cap U.S. cannabis which is very impressive considering one of their high-value markets, Massachusetts was completely shut down for much of the quarter.

The company also crushed EBITDA estimates by 113%, with $16.5 million of EBITDA.

However, this is much higher than our own calculated EBITDA for the quarter which was actually a loss of ($4.5) million, though this was a much smaller loss than last quarter’s ($24) million.

Nonetheless, if Cresco can keep up their sales growth, they are likely a quarter away from achieving both positive cashflow and EBITDA, a significant milestone.

How Does Cresco Stack up Against Peers?

Cresco’s negative cashflow and high debt load may present concerns at the moment but the company’s peer leading growth metrics and discounted valuation make it stand out amongst the other large-cap cannabis stocks.

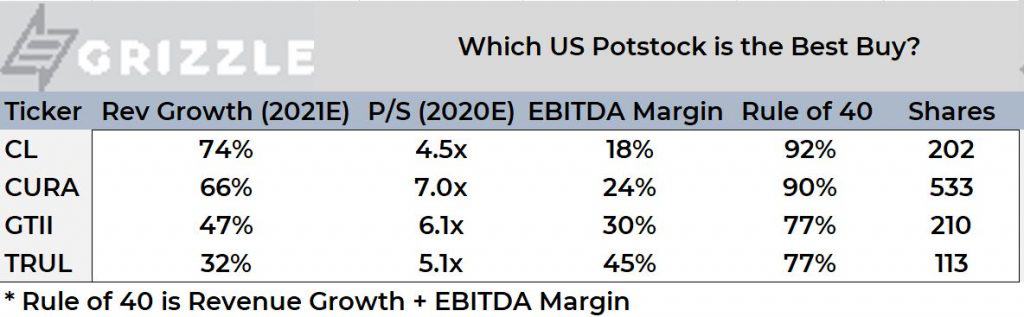

Consider the following comps analysis between the top four multi-state operaters (MSO) in the industry, including Cresco:

U.S. MSO Comp Sheet

Cresco leads with the highest revenue growth but as a result of all this growth spending, the EBITDA margin trails everyone else.

However, if you use our Rule of 40 which adds growth and margins together, Cresco still screens the best in the industry.

Companies like Trulieve and Green Thumb Industries outperform Cresco’s EBITDA margin, but much lower revenue growth makes their Rule of 40 values less attractive in comparison.

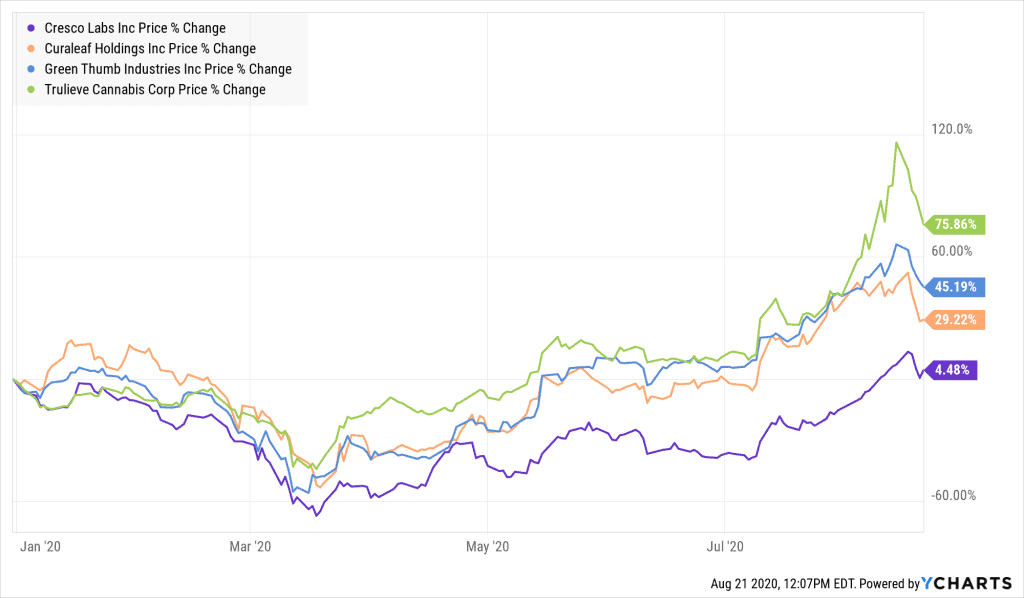

Also Trulieve’s, and Green Thumb’s share prices have done much better than Cresco’s this year which is reflected in their premium price to sales multiples.

YTD U.S. MSO Stock Price Performance

Is the High Debt Load a Problem?

The major concern we’ve had in the past that kept us from recommending Cresco was the low cash balance and large amount of debt.

Looking closer we see Cresco has $116 million of debt due in June of 2021.

However, we think Cresco likely has certain tools at their disposal to handle this debt without diluting shareholders, namely sale and leasebacks of additional growing facilities.

They also have another $100 million borrowing base on a term loan that could potentially be used, though the key term is “potentially”.

There are tons of restrictions on their ability to draw the additional $100 million including a minimum cash balance they must carry which was redacted in the loan document.

Give that management and insiders are among the lenders in the $100 million loan we think the company will figure out a way to get access to the other $100 million at the end of the day, though it will cost them dearly.

Cresco is already paying an astounding 24% interest rate on their debt or $38 million a year in interest.

We think it’s much less risky to own Trulieve, Curaleaf and Greenthumb as your core, but if some investors are looking for juice in their cannabis portfolio, Cresco as a 10%-20% weighting just to see if they can grow through the debt problems makes perfect sense.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.