Bottom Line:

Cloudflare (NYSE: NET) put up some good numbers out of the gate in its first quarter as a public company.

Recently investors are shifting their focus from growth to profitability and any tech company losing more money than the market expects is punished regardless of how fast revenue is growing.

Luckily for Cloudflare, the company beat revenue estimates by 6% and generated an earnings per share loss that was less than half what Wall Street was expecting.

The company also put out 2019 guidance for the first time that is 9% above our expectations.

With the stock up 5% after hours to ~$16.75 we think the stock could continue to creep higher with the overall market.

At the current stock price Cloudflare is trading at 13.5x 2020 revenue which is in line with the group average.

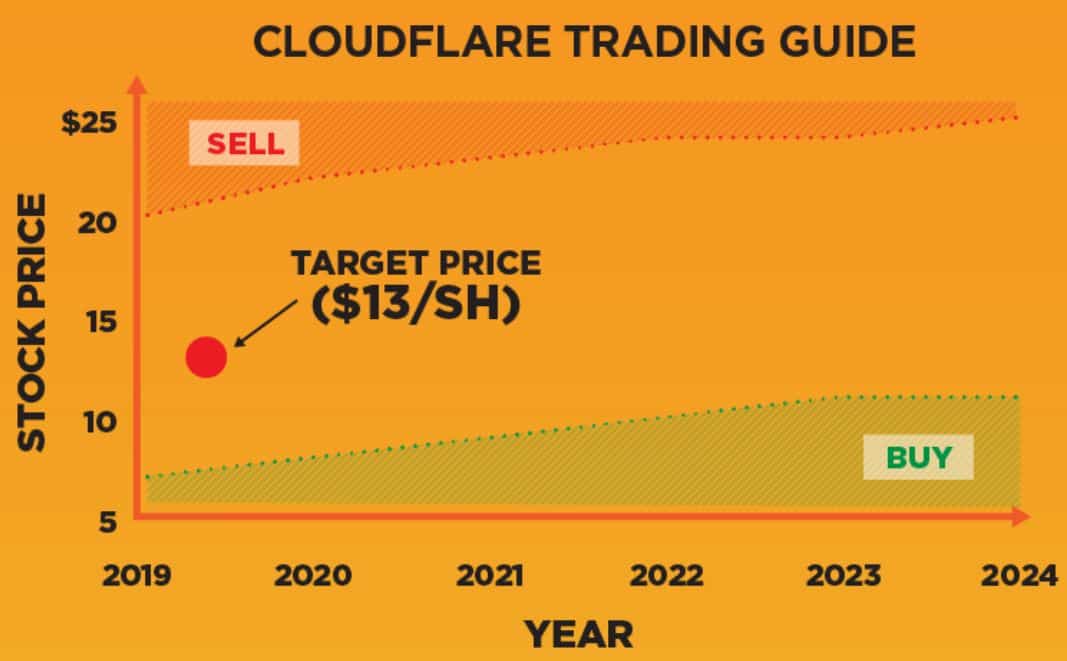

If it approaches $20/sh it will be trading at a premium multiple and we think there is significant risk that any fundamental hiccup will send the stock back to $15 or below.

Based on our long-term assumptions we think Cloudflare is a $13 stock so will struggle to hold a stock price in the high teens or low $20s.

Our trading guide below provides investors with our view on when to add to or pare back a position in the stock longer term.

When to Buy and Sell CloudFlare Stock

Earnings Review

Cloudflare reported third-quarter results that beat on revenue and EPS loss sending the stock up 5% in after-hours trade on Thursday.

Revenue grew 48% from a year earlier to $73.9 million, $4 million ahead of estimates. The GAAP net loss of $40.9 million was slightly higher than a year earlier, but when adjusted for IPO-related stock compensation, results were actually better than expected. The non-GAAP net loss widened to $18.5 million from $13.4 million last year.

Operations and investing burnt $33.64 million of cash during the quarter.

With the post-IPO cash balance of $645 million, Cloudflare has over 6.5 years of cash runway, more than enough to achieve cashflow profitability.

Increased R&D Spend

The gross margin of 78.3% was at the upper end of its tight 2% range over the last two years. Operating expenses of 133% of revenue were sharply higher compared to the second quarter’s 107%, but lower than a year ago. The biggest increase was in R&D expenses which rose 43% from last quarter and 92% from a year ago.

For the fourth quarter, the company expects revenue of $78.5 to $79.5 million, a slight slowdown in sequential growth. The Non-GAAP loss is expected to widen to a midpoint of $21.5 million. A non-GAAP loss per share of $0.06 to $0.07 is expected.

Cloudflare went public at $15 and began trading at $18, giving it a market value of $5.1 billion. The stock traded as high as $22.08 within the first two weeks, before drifting back to test its IPO price. Sell-side analysts remain bullish on the company with price targets ranging from $18 to $23.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.