Goodbye Trump Stock Market Pump, Hello War

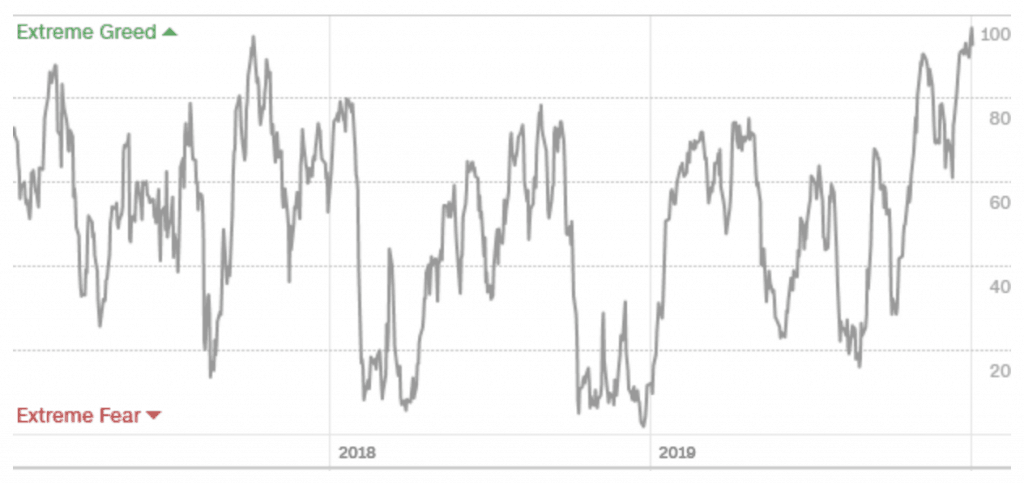

Investors entered 2020 assuming a continuation of the Federal Reserve and Donald Trump’s stock market “pump” — everyone was primed for the bet on beta (nothing can go wrong) trade. CNN’s ‘Fear & Greed Index’ was at its highest ‘Greed’ reading in over 3 years.

CNN Fear & Greed Index

The good times stock market party came to an abrupt halt on evening of Jan. 2 when the U.S. government announced that it had killed Iranian General Soleimani in a targeted attack in Iraq.

Iran has vowed a harsh retaliation for the killing of its general, raising the spectre of a full blown war in the Middle East. Iran also announced that it will no longer observe any limits on uranium enrichment, as the country no longer considers itself bound by the 2015 nuclear deal.

Grizzle’s strategist Chris Wood wrote a prescient bullish 2020 call on oil 2 weeks ago on the back of slowing shale oil production growth. The death of General Soleimani has added a very real layer of political risk to the upside in the commodity.

In today’s note we examine what commodities and stocks to own during conflict — it’s your financial insurance policy.

Middle East Wars: How Oil, Gold, and the S&P 500 Performed

We analyzed the performance of S&P 500, oil and gold during each of the major Middle East conflicts over the last 30 years: Persian Gulf War, Iraq Wars, and the Libyan Civil War.

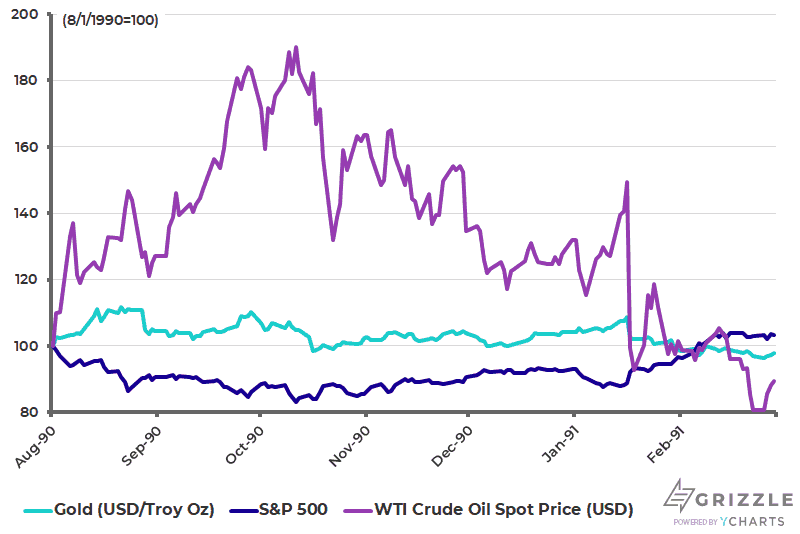

The First Iraq War

During the first Iraq War (Persian Gulf War) oil rallied nearly 80% in the first 2 months. However, oil’s early gains were given back over the remainder of the war — oil was down more than 10% over the duration of the war, gold was down 2% and the S&P 500 rose 3%.

Persian Gulf War: S&P 500, Oil & Gold

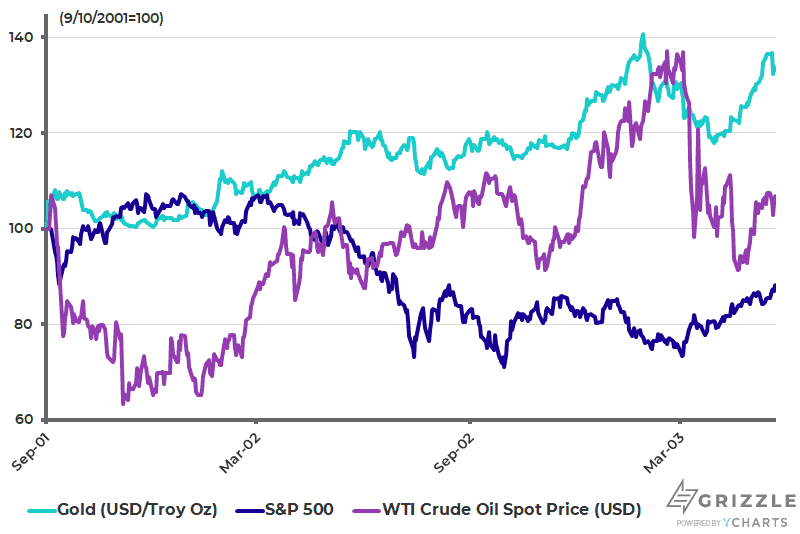

9/11 & the 2nd Iraq War

The fallout from the 9/11 attacks and the subsequent War in Iraq was very interesting, crude oil fell over 35% in the immediate 2 months after the attacks.

The potential negative economic impact related to potential future terrorist attacks and the prospect of a prolonged war weighed on the global economy and the related consumption of oil.

Gold was the best performing asset over the period, rising over 30%. Oil was up marginally 7% by the end of the war and the S&P 500 was down 12%.

9/11 & Iraq War: S&P 500, Oil & Gold

The Libyan Civil War

The Libyan Civil War was another period of extreme stress for the global oil markets. Oil rallied meaningfully during the first 5 months of the conflict, rising over 25%.

However these gains for oil were again all given back during the remainder of the conflict, oil ended up 3%. Gold was the asset to own during this period of uncertainty — up over 27%. The S&P 500 underperformed both oil and gold, down 7% over the period.

Libyan Civil War: S&P 500, Oil & Gold

Bottom Line: Gold is the Asset to Own During Conflict

While oil might seem the obvious no-brainer Middle East conflict play, the numbers simply don’t back it up. The economic uncertainty related to these wars is a far more powerful force.

When the economic and geopolitical outlook is uncertain gold is the asset that has historically preserved value — the numbers prove this applies for Middle East oil conflicts as well.

Our Preferred Way to Play the Yellow Metal: Gold Stocks

We’re longstanding gold bulls at Grizzle, as Chris Wood stated in his inaugural outlook piece — gold is the only practical way to hedge the inflationary risks associated with central bank quantitative easing (i.e. money printing).

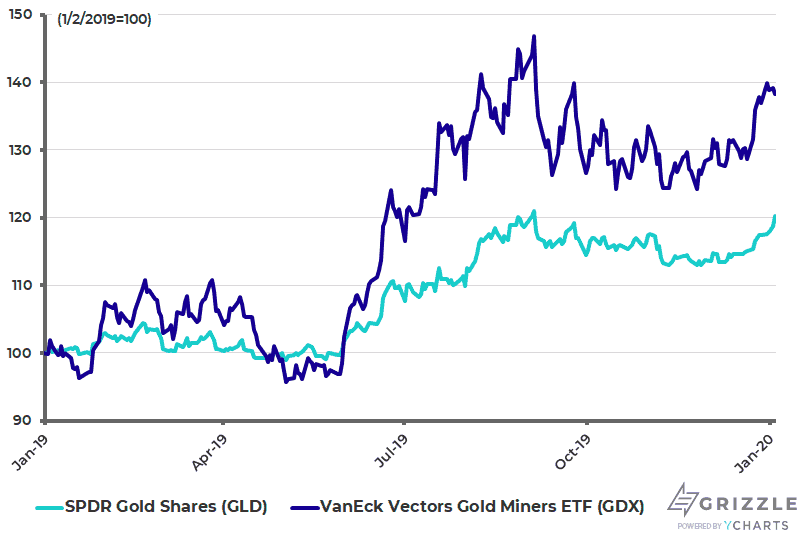

Gold and gold equities performed well in 2019, up +20% and +40%, respectively. This is exactly the performance relationship that gold equity investors want to see, getting compensated for the risks of owning gold mines.

In 2019 Grizzle nailed the call to own gold equities and more specifically we nailed the top stock to own: Detour Gold (TSE: DGC). Detour outperformed gold and gold equities since the beginning of 2019 by 94% and 74%, respectively.

A warrant of caution trading a hot #potstocks sector here, a few more days of downward chop in the S&P 500 ( $SPY) – there's no question other risk asset classes will get pulled down too

A beautiful set up here for #gold ( $GLD/ $GDX/ $GDXJ) in '19, $DGC (Detour) solid value buy

— Thomas George (@thomasg_grizzle) January 28, 2019

For 2020 we’re pounding the table again for gold equities, since the gold price peaked in 2011 at $1,895, gold equities have under-performed gold by -40%. Given the strong performance of gold equities vs. gold in 2019 we believe the market will continue to reward gold mining assets relative to gold in the vault for 2020.

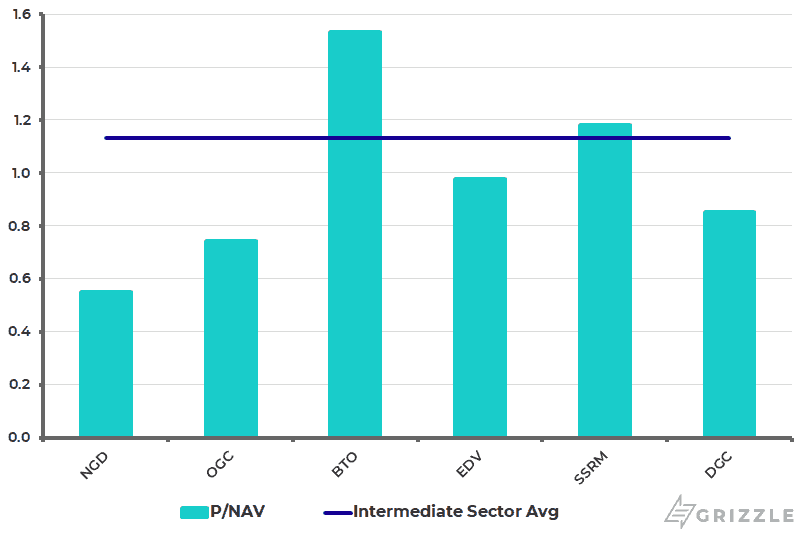

In November Evan Veryard at Capital 10X conducted a deep dive analysis of the intermediate gold mining sector, identifying 5 stocks that quantitatively screen well, unique attributes that senior gold mining companies would desire for M&A: New Gold (TSE: NGD), SSR Mining (TSE: SSRM), OceanaGold (TSE: OGC), Endeavour Mining (TSE: EDV) and B2Gold (TSE: BTO).

A visual summary of the analysis is presented below. This was followed up with another in-depth piece on junior gold miners.

Price to Net Asset Value (P/NAV) is one of the most important criteria, as a company with cheap assets would be viewed favourably for NAV accretion by the acquirer.

Price to Net Asset Value (P/NAV) is one of the most important criteria, as a company with cheap assets would be viewed favourably for NAV accretion by the acquirer.

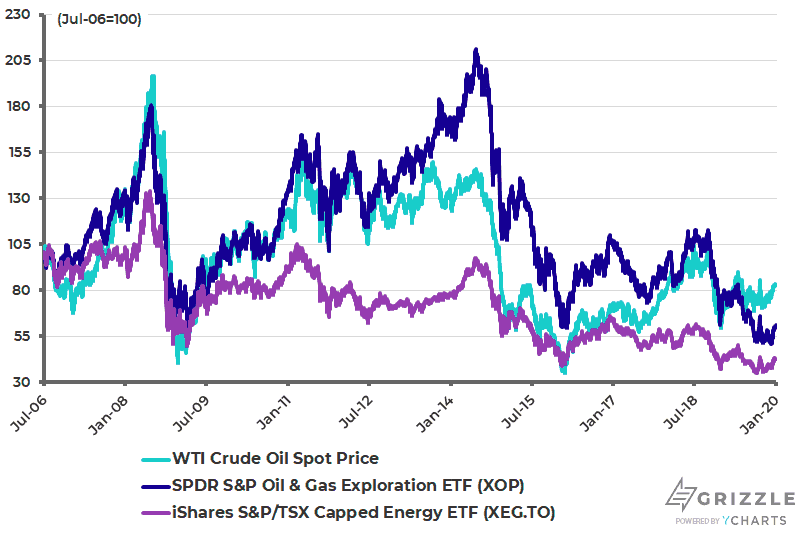

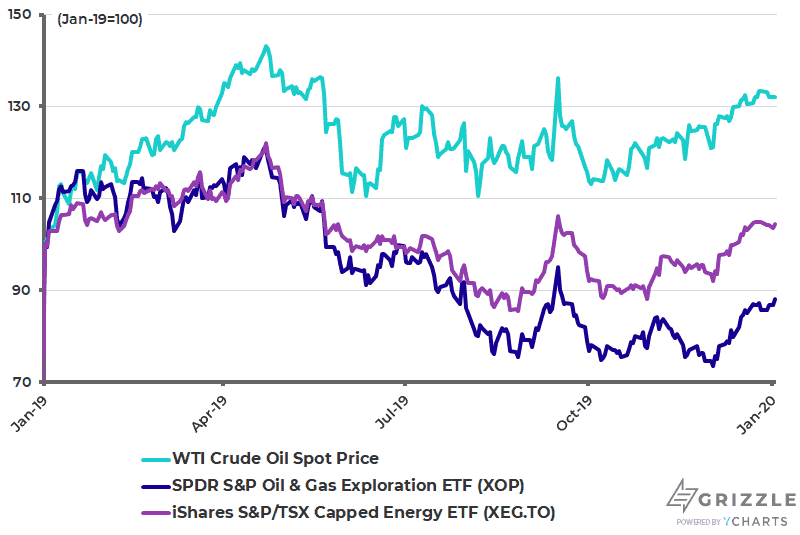

Oil Stocks Have Been Dogs vs Crude, Can They Catch a Bid?

There’s simply is no way around it, oil stocks have been absolute dogs versus oil the commodity on any timeframe you look at — it’s ugly (charts below).

This isn’t the way it should work. Oil stocks have three inherent advantages to a barrel of crude for investors who are bullish:

- Oil companies can grow production.

- Oil companies have operational leverage, the higher the price of crude the higher the margin.

- Oil companies have financial leverage, debt leverages their returns.

Oil companies simply haven’t been able to actualize the production growth targets they’ve touted. Additionally they haven’t been able to expand operating margins commensurate to rising oil prices, however on the downside they wear the margin contraction.

If Oil Stocks Can Work Again These Are the Stocks to Own

Own U.S. Oil and Gas.

Owning U.S. shale stocks gives investors three big advantages if the world does end up facing a supply shock.

- The U.S. has the least political risk and lower production costs among most developed oil producing countries.

- Shale has the lowest transition time, meaning wells can be turned on and off in only 1-2 months compared to larger oil projects offshore and in the oil sands of Canada that takes years to build and begin production. Shale producers can quickly take full advantage of global price spikes in oil to increase their profits, cashflow, and dividends.

- The U.S. has more than enough export capacity in the Gulf of Mexico to meet demand if lost barrels in the Middle East create a vacuum. Infrastructure is the most important piece of the puzzle.

Even if a producer finds a well just gushing oil, if they can’t move that oil to where people need it, each barrel is almost worthless.

Below are our preferred stocks to own during an oil supply crisis.

Enterprise Product Partners (NYSE: EPD)

Enterprise is one of the largest pipeline operators in the U.S. and owns key oil and gas pipelines that can move production down to the Gulf Coast for export. Enterprise also owns trophy waterfront export real estate, making it potentially the best positioned oil infrastructure stock to benefit from supply disruptions in the Middle East. Note: Enterprise is a Master Limited Partnership and is only suitable for U.S. domiciled investors for tax reasons.

Our other three picks are all shale operators who own acreage in the Permian basin, home to the most oil filled rocks in U.S. shale.

The more productive the rocks, the lower production costs are and the higher the profit as more barrels can be squeezed from each well.

Pioneer Natural Resources (NYSE: PXD)

Pioneer Natural Resources operates some of the most productive shale acreage in the United States.

The company owns lots of land in the Permian basin of Texas, the epicentre of the shale boom.

Due to the productivity of the rocks, Pioneer’s production costs are among the lowest of the shale stocks which translates into higher margins and more upside to cashflow if oil prices spike due to any global outages.

Pioneer has a strong balance sheet and could pay off all outstanding debt with the cashflow they will generate over the next seven months.

Concho Resources (NYSE: CXO)

Concho has the second-largest land package in the Permian basin of Texas.

Disappointing earnings recently have dented the stock price so there could be more of a bounce back with this stock if oil prices continue to trade up on geopolitical concerns.

Concho is sitting on about twice as much debt as peers compared to the cashflow they generate, but the debt levels are still very manageable and do not have us concerned.

EOG Resources (NYSE: EOG)

EOG is also a major operator in the Permian and has a long track record of best in class operations.

EOG is also more diversified than the Permian-focused drillers with amazing rocks in the Eagle Ford play of Texas and solid operations in the Bakken Formation of North Dakota and the D-J Basin of Colorado.

EOG is a leader in bringing technology to the oil industry.

They collect millions of data points about each well’s performance which allows management to be more nimble than peers when it comes to capital allocation decisions.

EOG has less than one times debt to EBITDA, meaning the company could pay off all its debt from the cashflow generated in this year alone.

On the Canadian side these are the two stocks we’d go with:

Cenovus (TSE: CVE)

Cenovus is one of the largest Canadian exploration and production companies.

They have good access to pipelines, which is all important in a Canadian oil market starving for ways to move all the excess oil down to America where it can be refined and sold to consumers.

Cenovus also has a high debt load of 2.5x debt to EBITDA, which means it will see even greater leverage to higher oil prices and rising cashflow.

When oil prices are rising you want to own the producer with the high debt and low expectations. Cenovus ticks both of those boxes.

Canadian Natural Resources (TSE: CNQ)

Canadian Natural Resources is another Canadian producer with excellent access to pipelines to make sure its production can make it to the hub where oil is selling for the highest price.

Debt is 2 times EBITDA which is on the high side and provides investors with solid leverage to rising oil prices.

CNQ has an excellent operating track record so investors don’t have to worry about an operational hiccup derailing the expected cashflow upside from higher oil prices.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.