Due to the rising demand from electric vehicles and the underinvestment in new copper mining globally, copper prices are on the rise, but are really just getting started.

Copper stands alone with its ability to provide both an inflation hedge as well as solid commodity investment.

An Inflation Hedge

Typically when we think of commodity investing to protect your wealth, we think of gold or silver. Not often do you hear of someone stocking up on copper and expecting to make big bucks if inflation rears its ugly head.

However, copper prices are on the rise and are all set to blow past their last peak in early 2011 of ~$457.

But just like gold and silver, copper is impacted by inflation (inflation impacts purchasing power and is really important when considering a commodity play).

So let’s talk about economics.

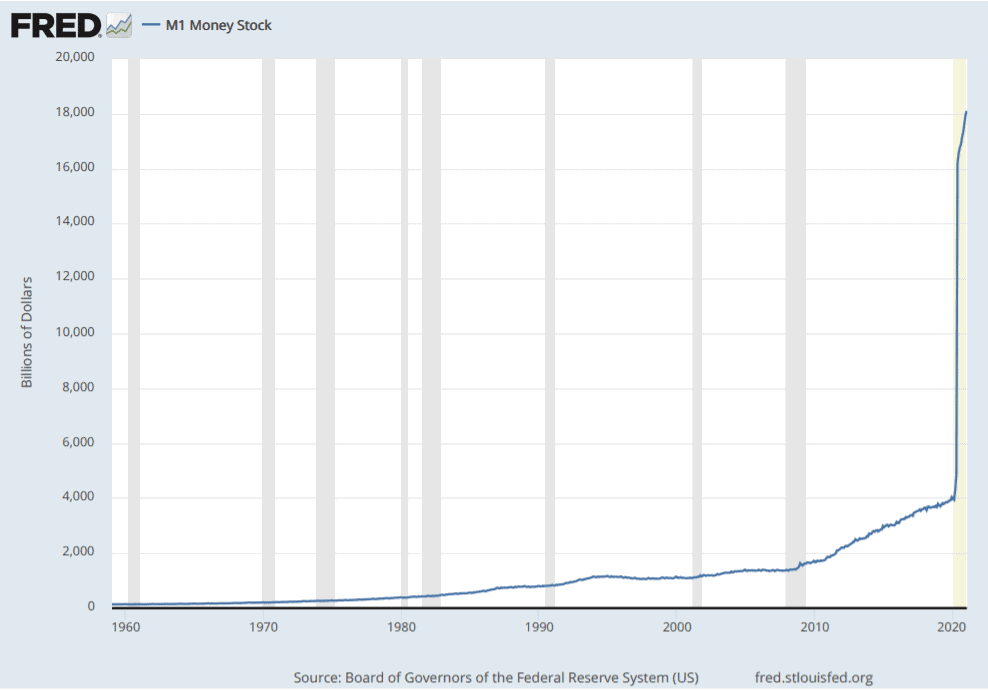

M1 Growth (Growth of Money in the Economy)

This chart shows the unprecedented increase of money in circulation (M1), an astounding 355% yoy growth.

And while it seems a decent amount of this money may be sitting within the banks, once those flood gates open and people start spending, prices will rise.

In other terms, the more money being spent, the more demand, the more prices go up = inflation.

While gold is a great defensive commodity to guard again inflation, copper looks as attractive as ever as both an inflation hedge and an attractive commodity investment to play economic growth.

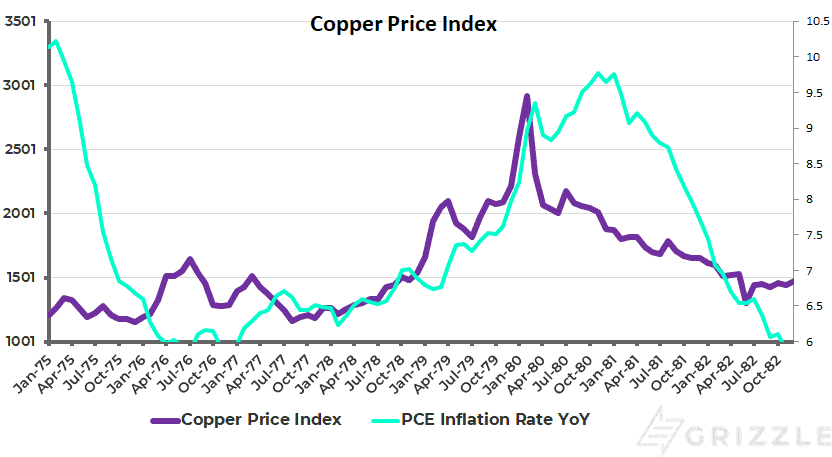

The chart below looks at how copper prices performed the last time inflation truly got out of hand, over 45 years ago.

We can see as inflation increased so did copper, almost tripling in price in two years.

So we’ve definitely confirmed copper is an inflation hedge.

Copper Price vs Inflation in The 1970’s

As depicted above, when inflation rates go up and the market is booming, copper prices goes up. This is because copper is used in everyday life (e.g., electric vehicles, construction of homes, etc.).

As depicted above, when inflation rates go up and the market is booming, copper prices goes up. This is because copper is used in everyday life (e.g., electric vehicles, construction of homes, etc.).

Slight nuance is that if rates hit a point so high that they choke off economic growth and the economy begins to decline, then copper prices will also decline.

That being said, with inflation as low as it is, we expect to see copper prices rise as inflation begins to rise.

Commodity Economics

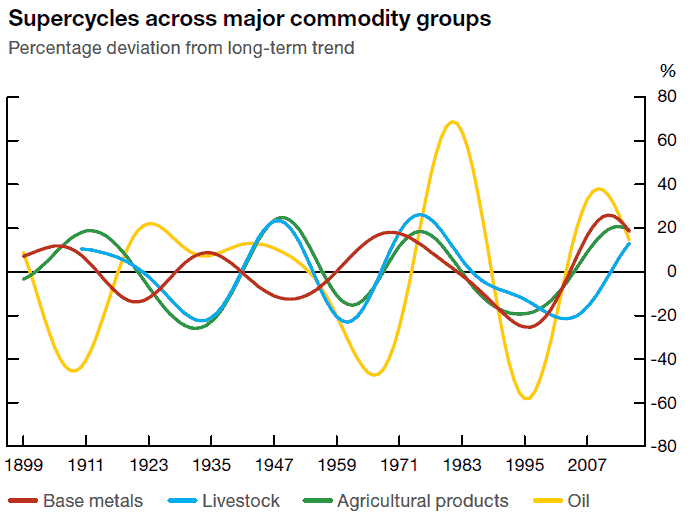

Another interesting economic factor to consider is commodity supercycles.

The chart below is provided by the Bank of Canada and shows deviations of long term trends (the 0 line on the chart).

Why do these cycles happen? Because no one knows the exact right supply to meet demand.

So often, at some point in time there is not enough supply and too much demand so prices increase.

When prices increase, too many suppliers get involved and supply increases beyond demand, at which point prices go back down and some suppliers leave the market.

Then supply goes back and prices go back up, and so on and so on, hence a cycle.

But what drives demand?

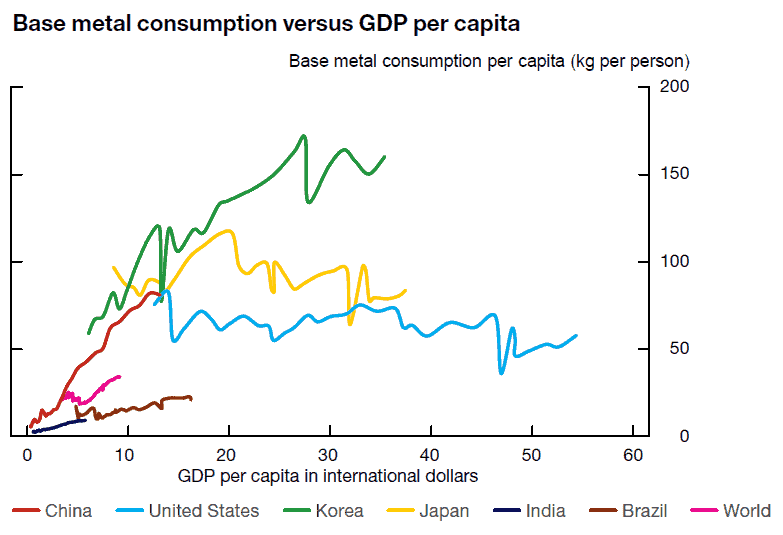

Above we stated that because copper is used in everyday life, as the economy improves the demand for copper increases.

This chart below confirms that as GDP (a metric for the health of an economy) increases the consumption (a.k.a. demand) of base metals increase as well, and that this is true worldwide.

More importantly many countries such as India and Brazil are still way below the US and other developed countries in their use of metals.

Demand for metals will continue to be strong as the world develops.

Again, slight nuance is that after a certain per capita GDP, consumption hits a steady state and growth tapers off.

This can be seen in the chart above for the US and Japan.

We are still far away from plateauing for many larger developing countries.

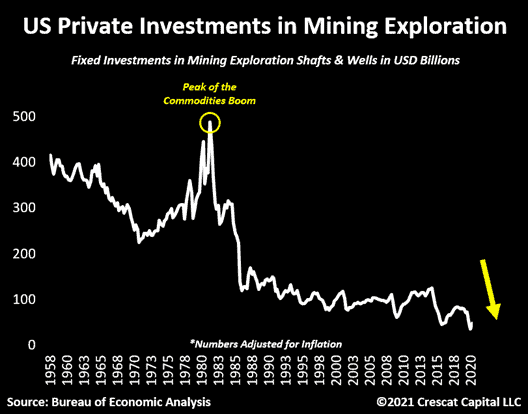

Mining Investing

Investment in mining is at all-time lows…

But demand continues to grow.

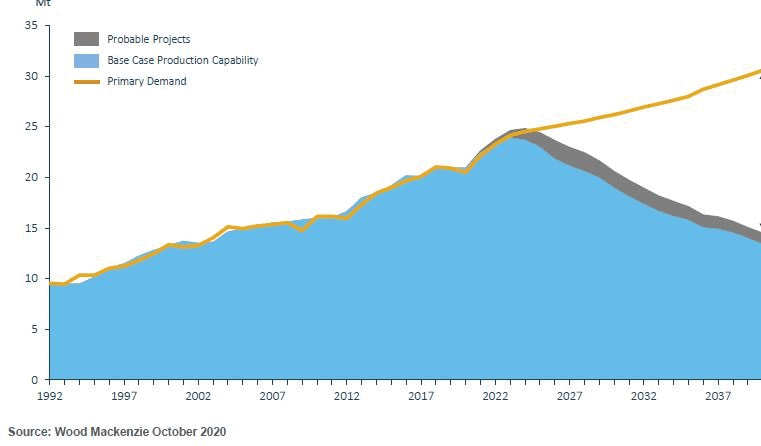

The world needs more copper than the industry plans to produce.

The larger the wedge between probable projects/supply and demand, the more likelihood of price increases (not enough supply = increase in prices).

The larger the wedge between probable projects/supply and demand, the more likelihood of price increases (not enough supply = increase in prices).

We expect that in the next 3-4 years we will experience a large gap between supply and demand.

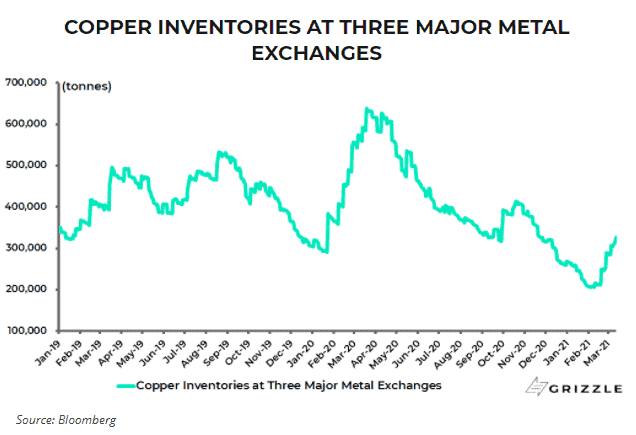

Furthermore, copper inventories today are at a decade low.

So if an inflation hedge is not enough to entice you to invest in copper, perhaps the anticipated price run due to supply vs. demand mismatch sweetens the deal.

Valuations

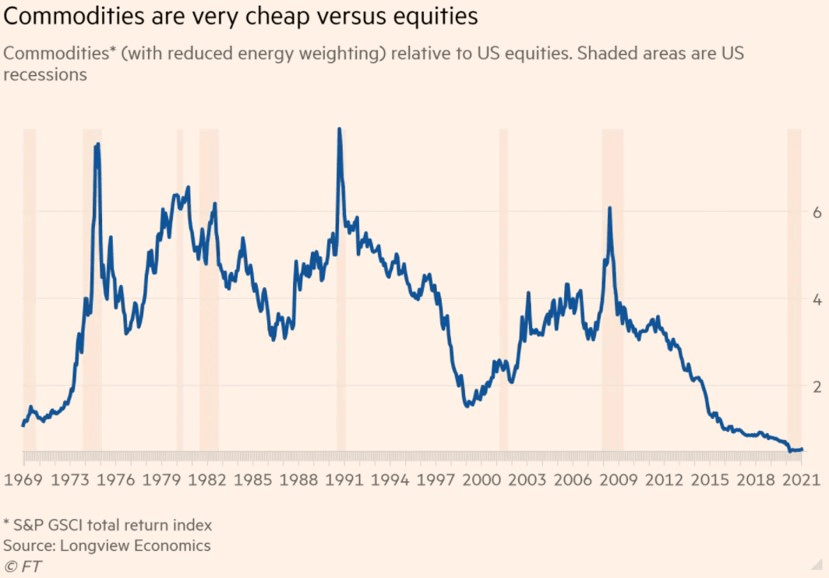

Looking at commodities’ valuations overall, this next chart does a good job of showing the relation between buying commodities vs equities.

The value of commodity stocks vs non-commodity stocks is at a 40 year low.

Commodity stocks don’t need to get anywhere close to where they’ve been in 2003-2008 for you to make some stellar returns.

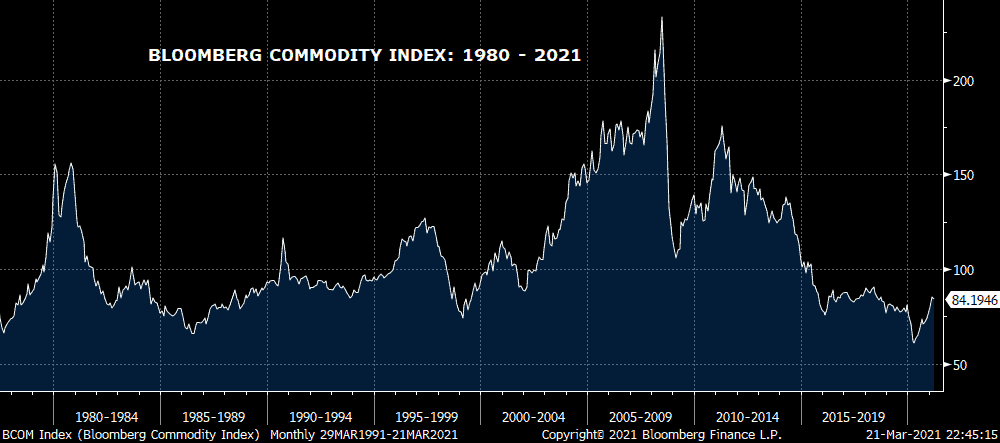

The Bloomberg Index chart below reaffirms that now is a relatively good buying opportunity for copper given the relatively low prices vs. historical levels.

Commodity Basket Since 1980

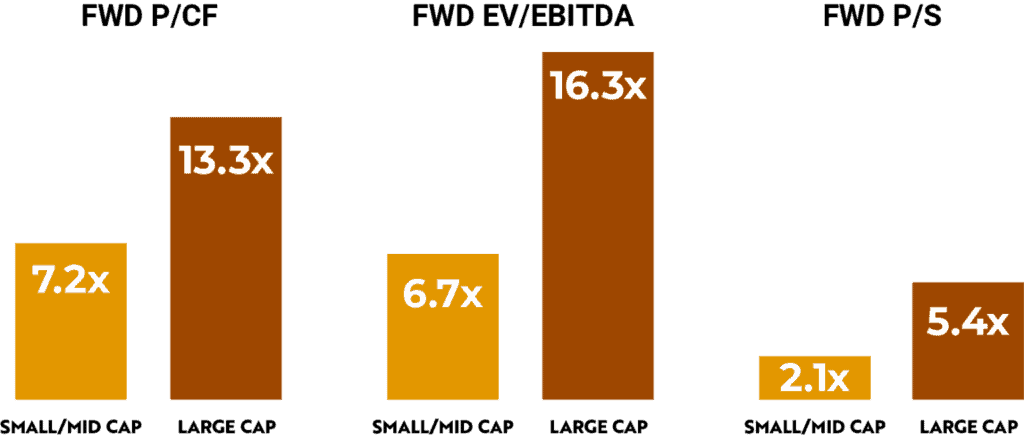

Next, let’s look at valuations for small/mid cap vs large cap producers’ valuations.

We have excluded exploration companies with no production for comparison purposes.

Multiples of Copper Miners

Very simply, there is a disconnect between small/mid-cap and large-cap producers in terms of multiples.

Small/mid-cap are so much cheaper as compared to large-cap, sometimes less than half!

This is interesting because in order to get a copper mine up and running it takes a lot of time and lots of money.

So if there is increased demand for copper and prices continue to rise, for some of the larger mining companies it will be cheaper and more efficient to just buy up smaller producers at these discounted multiples, rather than investing in new mining projects that will potentially take a decade or more to yield any copper.

Putting It All Together

Given the economic factors discussed, it is safe to say we are in the early stages of a commodities supercycle.

This is important because during a supercycle there is always an associated M&A boom.

The best way we think to play the M&A boom is to own small cap producers trading at cheap multiples.

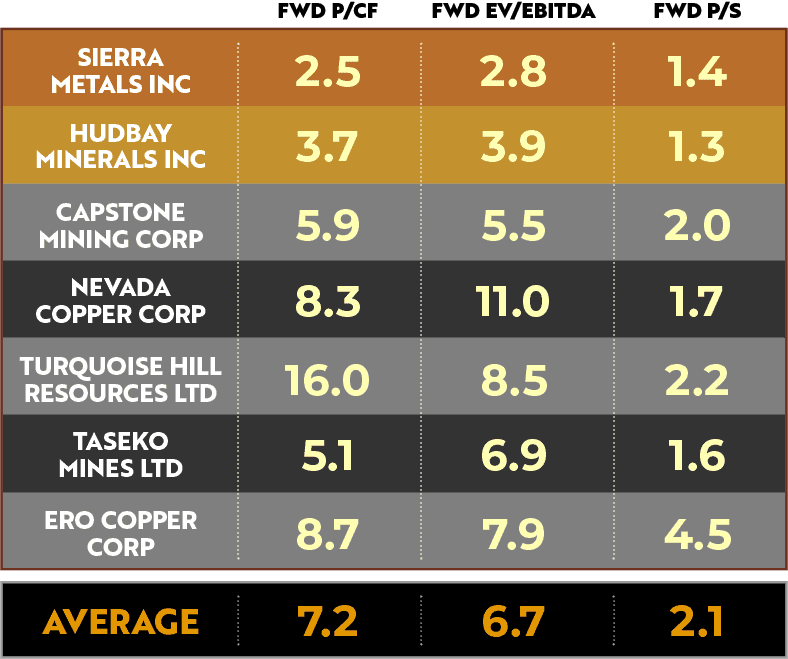

Clearly, two stocks stand out as the cheaper of the bunch – Sierra Metals Inc (SMT.TO) and Hudbay Minerals Inc (HBM.TO).

And while one strategy may be to buy up shares in the entire lineup, a better strategy may be to buy the cheapest of the cheap.

Small/Mid Cap Producer Valuations

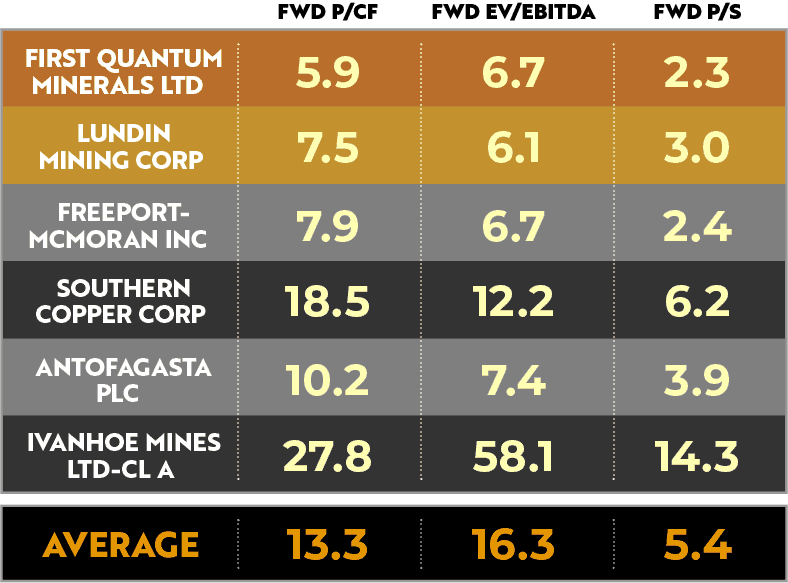

The same strategy can apply to the large-cap universe but for different reasons.

It is important to mention that while small-caps are cheaper, a big part of playing commodities is keeping in mind where the money will flow.

Large Cap Producer Valuations

Big institutions will first buy into the large-cap copper miners before they look at the smaller players.

This could push large-cap values up even higher than they are now relative to small-caps.

This isn’t necessarily a bad thing if you own a Sierra or Hudbay.

As such, we recommend investing in the cheapest of the cheap (SMT.TO) for value or investing bit by bit through the small-cap names if you want diversification.

But either way, copper will remain the king of commodities in what is shaping up to be a commodity supercycle.

Disclosure: The author does not have a position in any of the company’s mentioned in this article. Employees of Grizzle may own securities mentioned in this article.

Our full disclaimer can be found HERE

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.