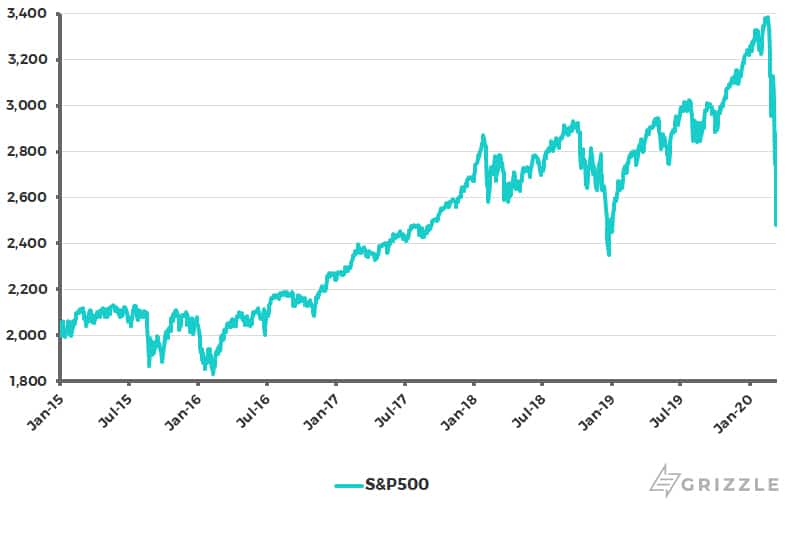

The Coronavirus has continued to drive market sentiment with the S&P500 testing its late 2018 low last Thursday (see following chart).

So long as the number of cases is rising in Western Europe and North America, and they clearly are, there is every risk of more panic selling.

Meanwhile China’s example has made clear that to slow the spread of the virus requires drastic action which has now finally begun to be taken in the Western world.

S&P500

One reason China took this approach so aggressively is because the virus had become a test case of the Communist Party’s ability to manage a crisis, most particularly given the increasingly centralized nature of government under President Xi Jinping and the renewed Leninist-style prioritizing of the Communist Party over other organs of central government.

The growing official media coverage of Xi’s personal management of the crisis in recent weeks has suggested growing confidence on the part of Beijing that it has the virus under control.

This culminated with Xi’s visit to Wuhan on March 10, though it should be noted he was still wearing a mask. Still there have been the highest political stakes involved, as there was considerable criticism on the internet in China on the initial handling of the health emergency, and the criticism has not just been targeting the local authorities in Wuhan and Hubei but also the central government.

In Xi’s China any criticism of the central government is criticism of Xi himself.

Still, that criticism is now receding given the dramatic collapse in the number of new cases in China and the contrasting surge in cases in Europe and North America.

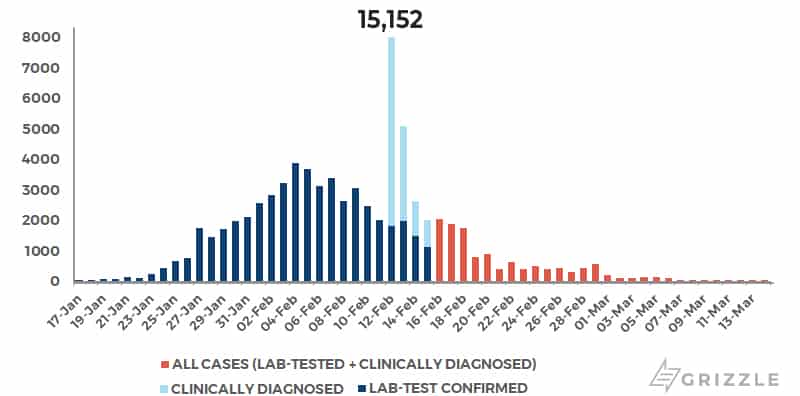

The number of daily new cases in mainland China has collapsed from a peak of 3,887 cases on Feb. 4to 20 cases on March 14.

China daily new Coronavirus cases

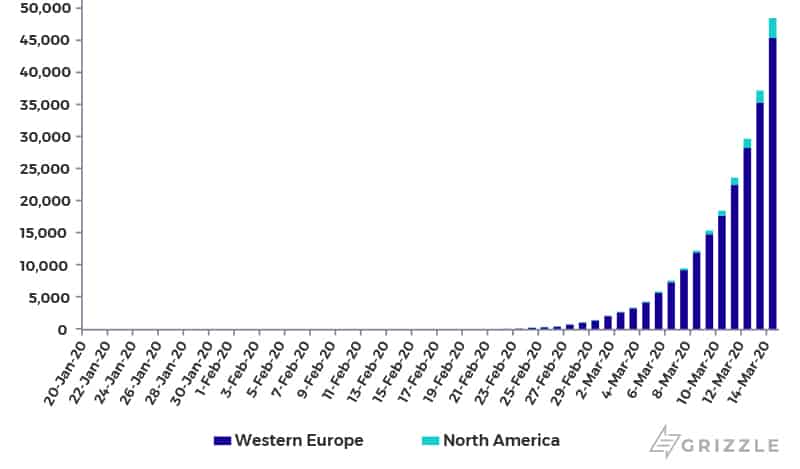

While the number of total cases in Western Europe and North America have risen from 1,427 and 83 cases respectively at the end of February to 45,310 and 3,114 cases on March 14.

Total Coronavirus Cases in Western Europe and North America

What about the nature of pending stimulus efforts in China after a first quarter which, in economic terms, will probably have been a write-off?

The focus will remain on targeted tax cuts and measures to promote consumption.

Aggressive monetary or fiscal easing, however, is much less likely since this would undermine the deleveraging campaign of the past few years which has succeeded in improving the quality of growth over the previous focus on quantity of growth.

Meanwhile, one “positive” consequence of the Coronavirus was a news article last month reporting that carbon emissions are down sharply in China (see Bloomberg article: “Virus Cuts China’s Carbon Emissions by 100 Million Metric Tons”, Feb. 19,2020).

The article quoted a recent analysis by the climate non-profit website Carbon Brief which looked at carbon emissions during the two-week period beginning 10 days after the start of the Chinese New Year festival.

According to the report, China emitted 400m metric tons of carbon dioxide over that period in 2019, while this year’s figure is estimated to be closer to 300m metric tons.

This news item highlights the growing focus among investors, as well as of course the media, on all things carbon related.

Asset Shift to ESG Funds is Accelerating

I was interested, though not surprised, to read recently that a prominent U.S. investment bank has now declared that ESG (Environmental, Social, and Governance) will be the “defining theme” of the current decade, just as TMT was in the 1990s, BRICS in the 2000s and FAANG in the last decade.

This could well prove to be the case; though I remember no one so confidently, or accurately, picking the decade’s winner at the start of the previous decades.

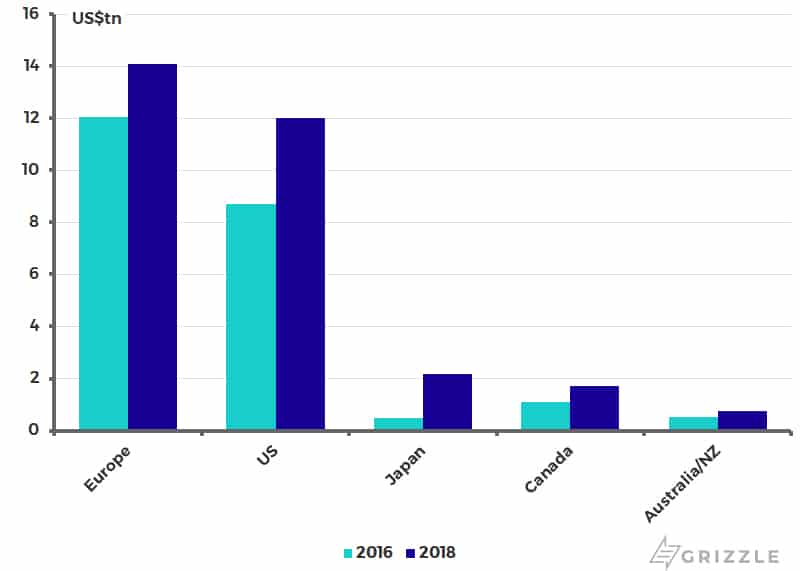

Still there is no doubt ESG has momentum, with estimates of nearly US$15 trillion in ESG assets in Europe, US$12 trillion in America and nearly US$3 trillion in Asia.

Global Sustainable Investment Assets

My own view remains that the emerging ESG boom is likely to culminate in a massive misallocation of capital, though most likely with a green “bubble” interlude in between.

Still it is hard to say how fossil fuels can be easily replaced given the world’s continuing massive dependence on them, most particularly from the standpoint of developing countries.

Oil Slump a Threat to the Sustainability Story

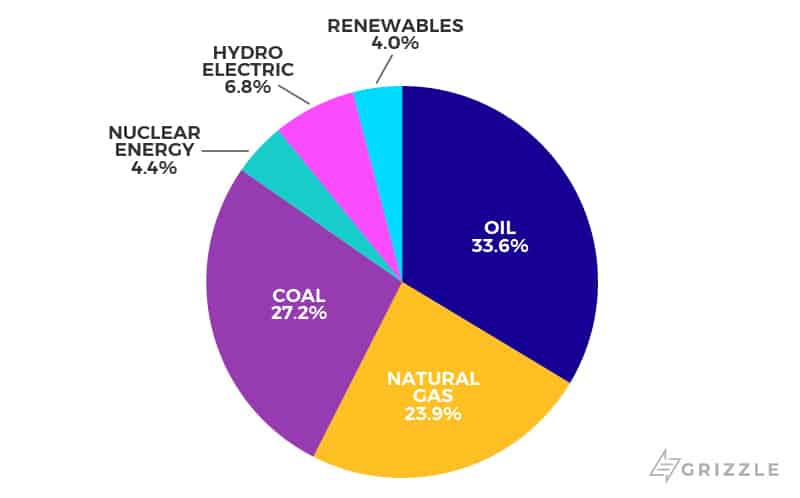

Based on the latest data, oil accounts for 34% of the world’s energy consumption, coal for 27% and natural gas for 24% – or a combined 85%.

While global oil demand reached a record 100m barrels/day last year, though the Coronavirus will likely cause a decline this year.

World Energy Consumption by Fuel Type

There also continues to be far more focus from both politicians and the growing number of ESG specialists on the “buy side” on curbing investment in fossil fuels rather than on curbing the demand for consuming them.

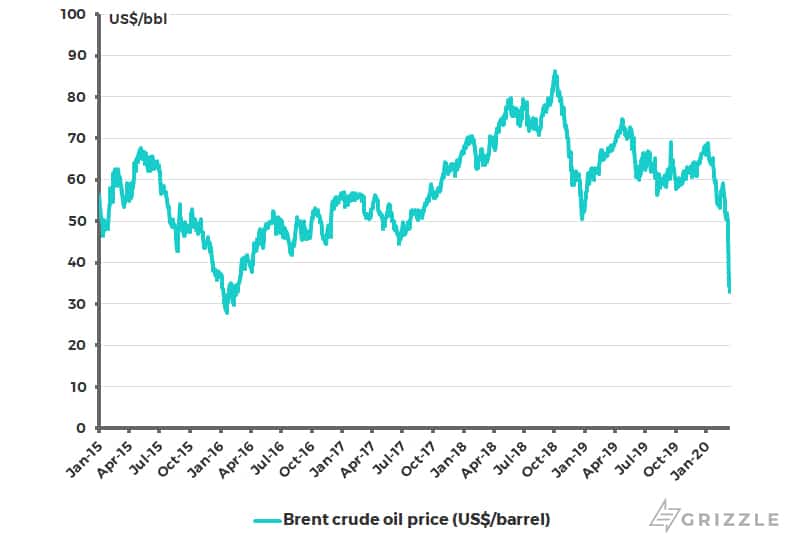

This is because the latter policies are likely in practice to prove politically unpopular with the ordinary voter, especially after the past week’s 32% collapse in the oil price caused by the failure of Russia to agree to production cuts with Saudi Arabia.

Indeed the collapse in the oil price is now a threat to the whole “sustainable energy” story unless governments are willing to tax consumers for consuming fossil fuels.

Brent Crude Oil Price

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.