With all this talk of an upcoming recession, we thought it’d be interesting to take a look at two stocks that people have been saying are ‘recession-proof’.

Namely, the stocks are: Costco and Amazon.

They both have very good business models that tend to work well regardless of prevailing market conditions.

These two companies provide products and services that are so important, or such an integral part of all of our daily lives, such that we would spend our money on them even if our pay gets cut.

If we were to enter into a long term recession, perhaps it would be a good idea to potentially load up on some shares in either these companies, at the same time as we buy their products.

Comparing How Amazon and Costco Fared During the Great Recession (2008-09) VS. Past 1 year

Although the conditions surrounding the economy now is very different to the economy preceding 2008-09, we can at least get a sense of how consumers and investors alike will react if a recession comes.

We’ll be comparing various metrics over the past one year to the same metrics throughout the peak of the Great Recession which occurred between Dec 2007 and June 2009.

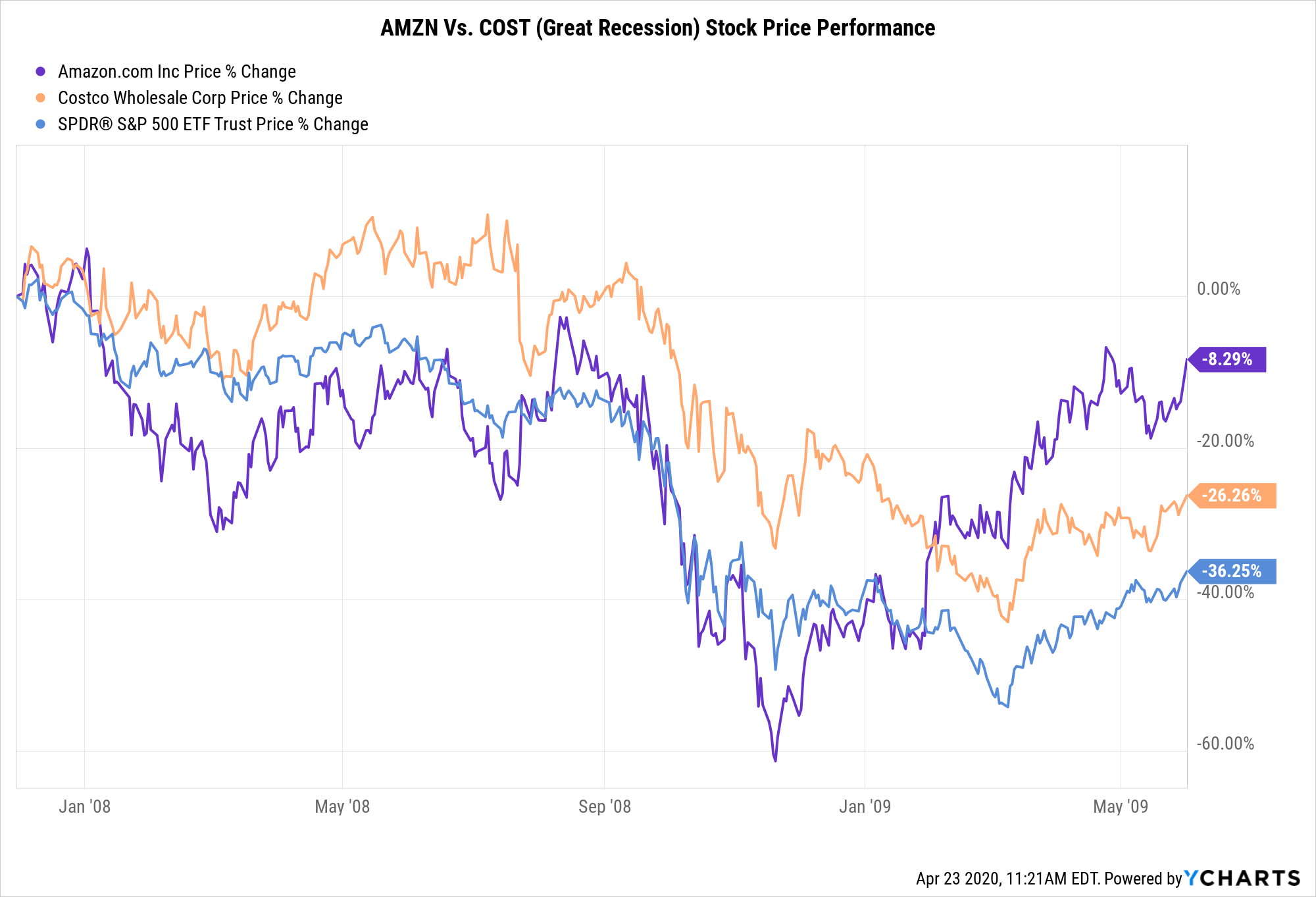

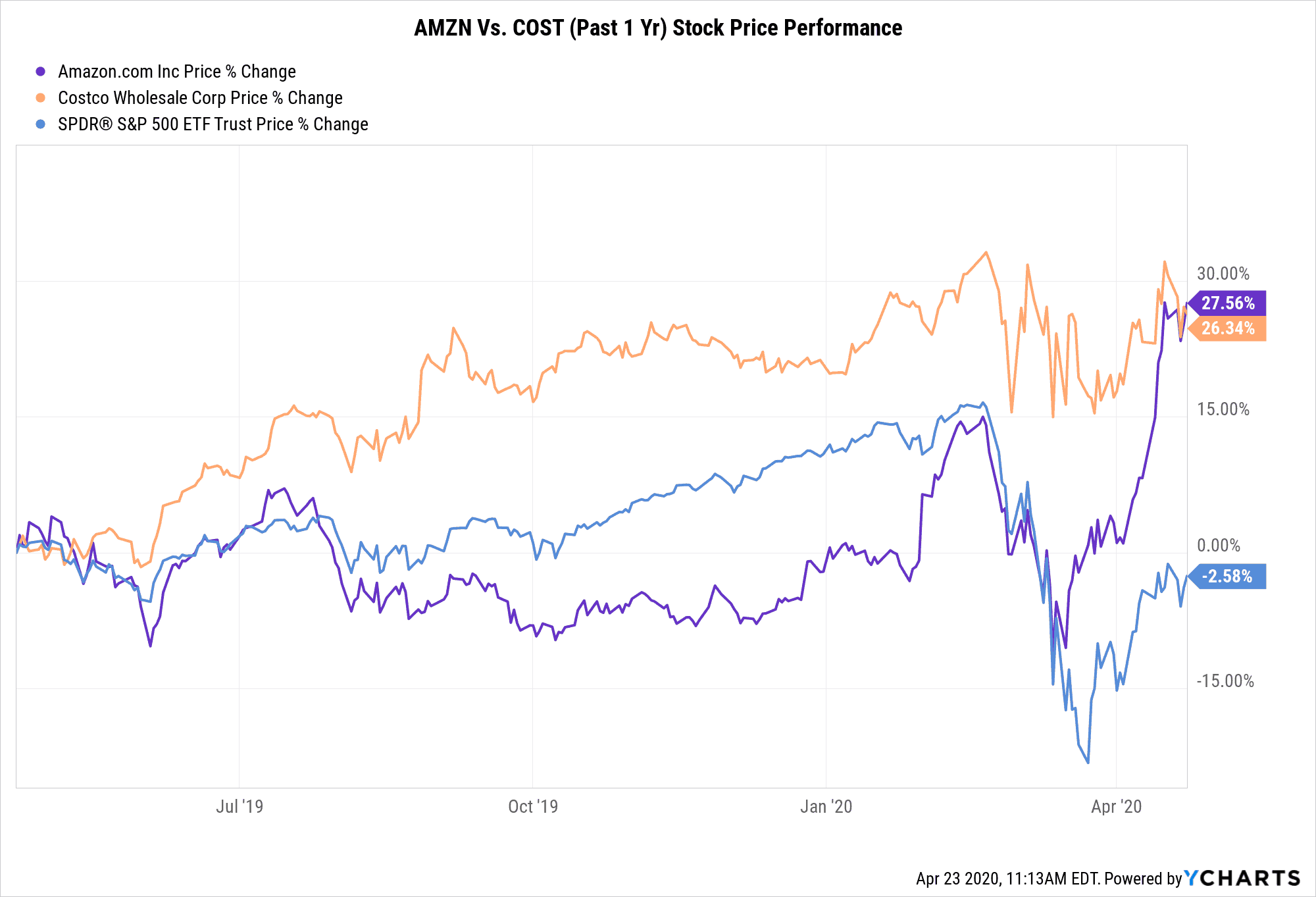

Stock Price Performance

We see that Amazon stock held up better than Costco from Dec 2007 to June 2009 during the height of the Great Recession. However, Costco had been leading Amazon for the better part of the entire recession bear market until the very end.

Note that both stocks still outperformed the S&P500 during this time period.

Taking a look at the past one year from now, we see a similar story. Costco has the tendency to consistently beat the S&P500 while Amazon has the tendency to rally up really hard in short bursts.

Also note that ever since the COVID-19 crisis began back in around late February and into March 2020, both stocks have seen some healthy rallies while the S&P500 has declined notably, and still remains negative on a one year basis despite the recent rally.

Although Costco can be considered somewhat of an “outdoor” business (which is a business that requires its customers going outside to purchase its goods or services) which tend to get hit hard in a pandemic, Costco is somewhat exempt from this as they are an essential service and cannot be shutdown.

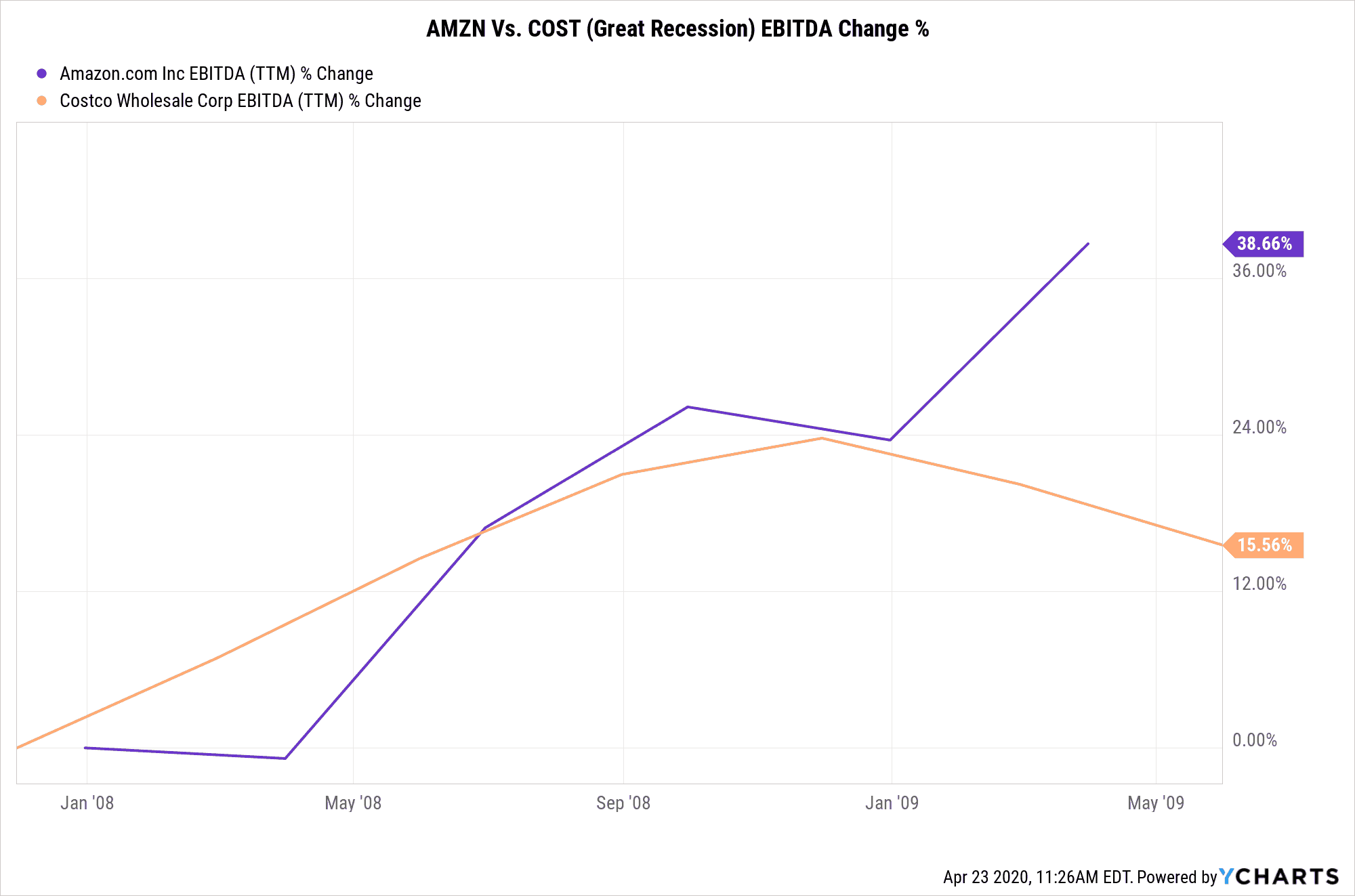

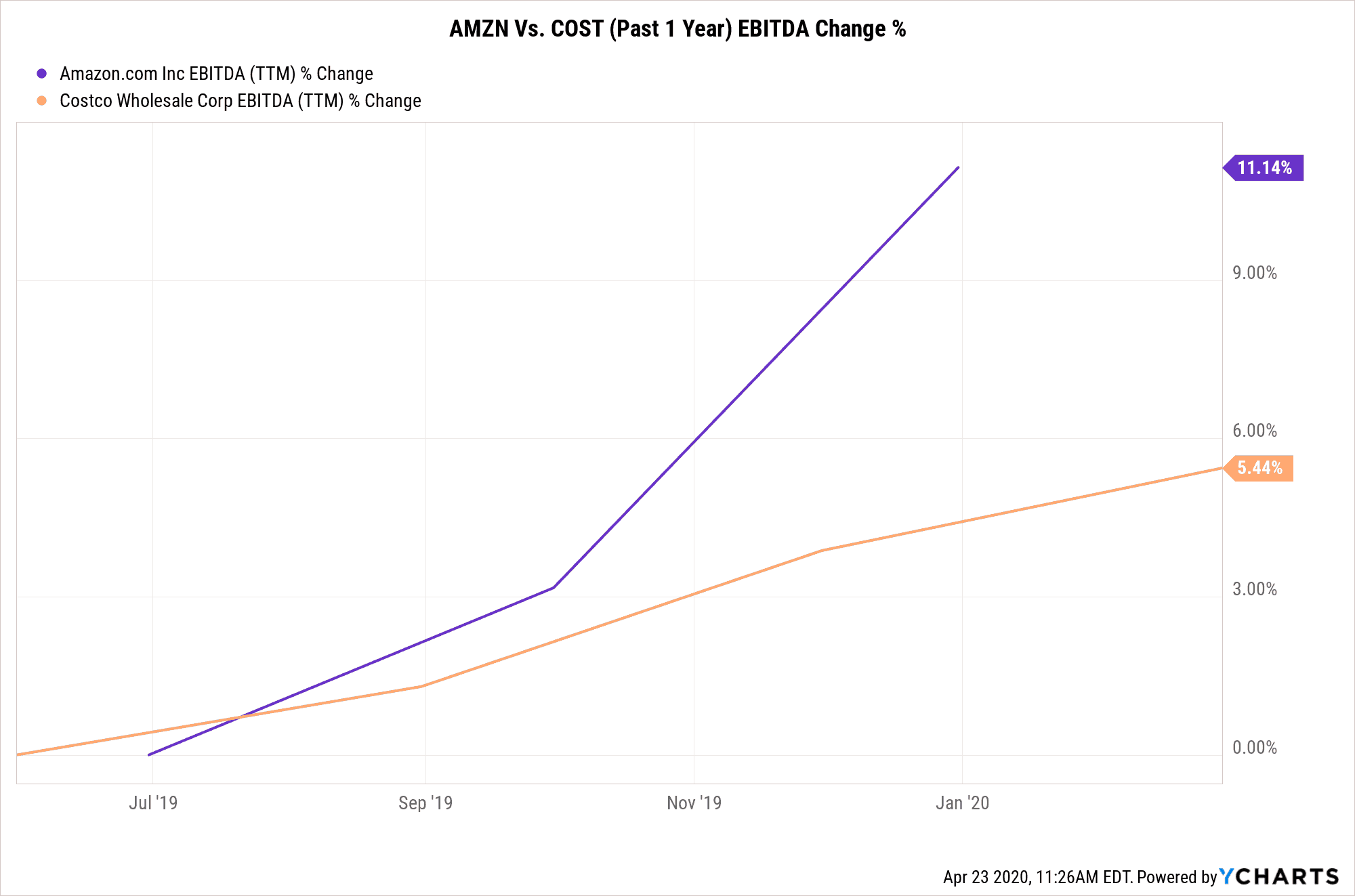

EBITDA Change

Diving in further, let’s look at EBITDA change of the companies during the Great Recession compared to now.

This is important because we want to see that the company’s profitability is not impacted too heavily if a recession were to occur.

We see that both companies increased their EBITDA significantly on a TTM basis during the Great Recession despite the overall bad market conditions, with Amazon up significantly more.

Although we won’t know how Amazon performed in their latest quarter until their results come out on Apr 30, analysts are expecting Amazon to post some very large sales increases, and it is likely that they will indeed deliver some amazing numbers given the reports coming in that Amazon has been going on a hiring spree to deal with increased volume for online shopping.

However, we must also keep in mind that we are only in the beginning stages of what might be a recession and the majority of the data we have now comes from pre-crisis times in 2019.

Another thing to note is that Amazon’s scale of business is dramatically larger than it was back in the Great Recession, so there is reason to believe that Amazon will fare much better if another global economic slowdown occurs.

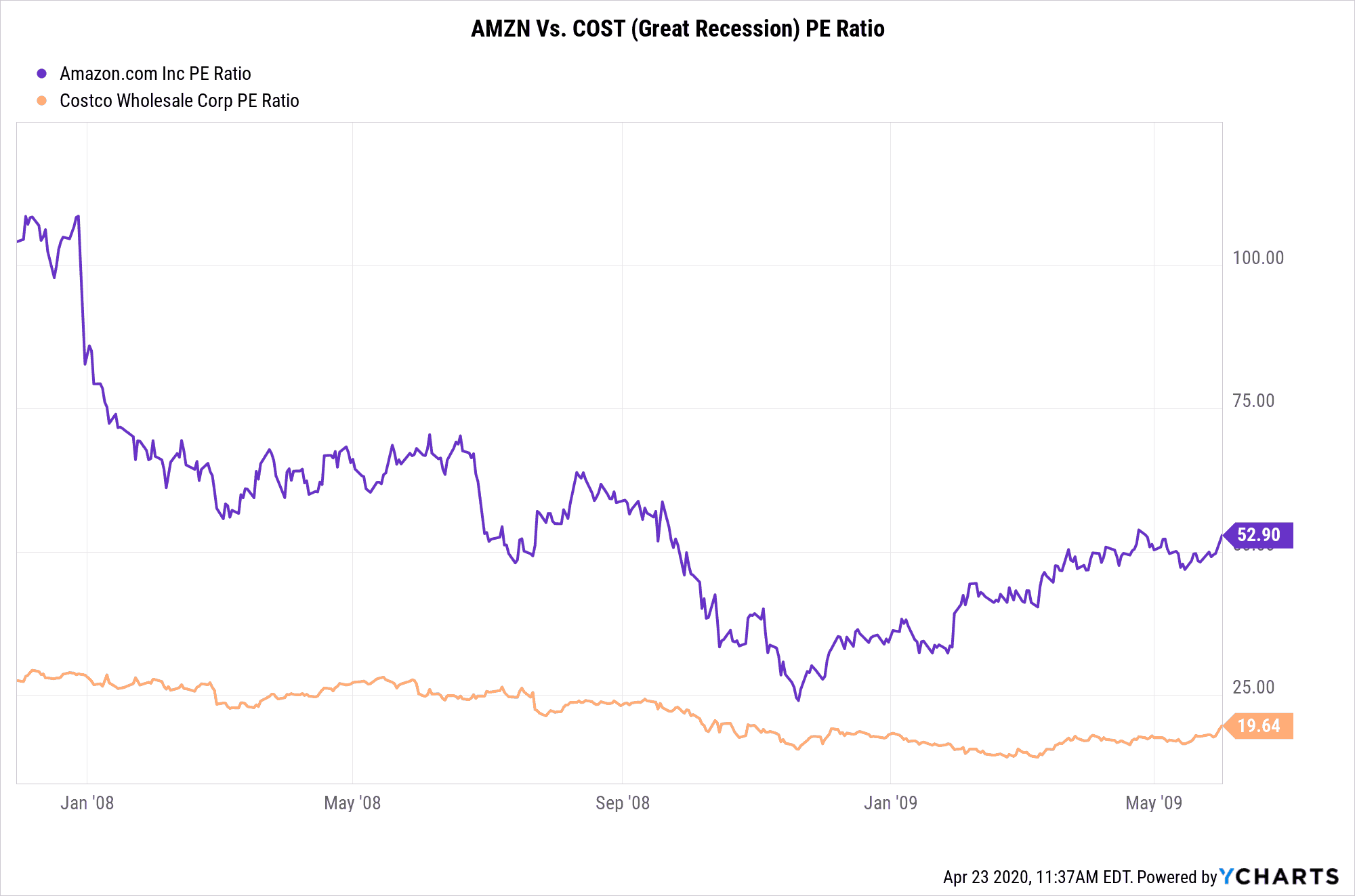

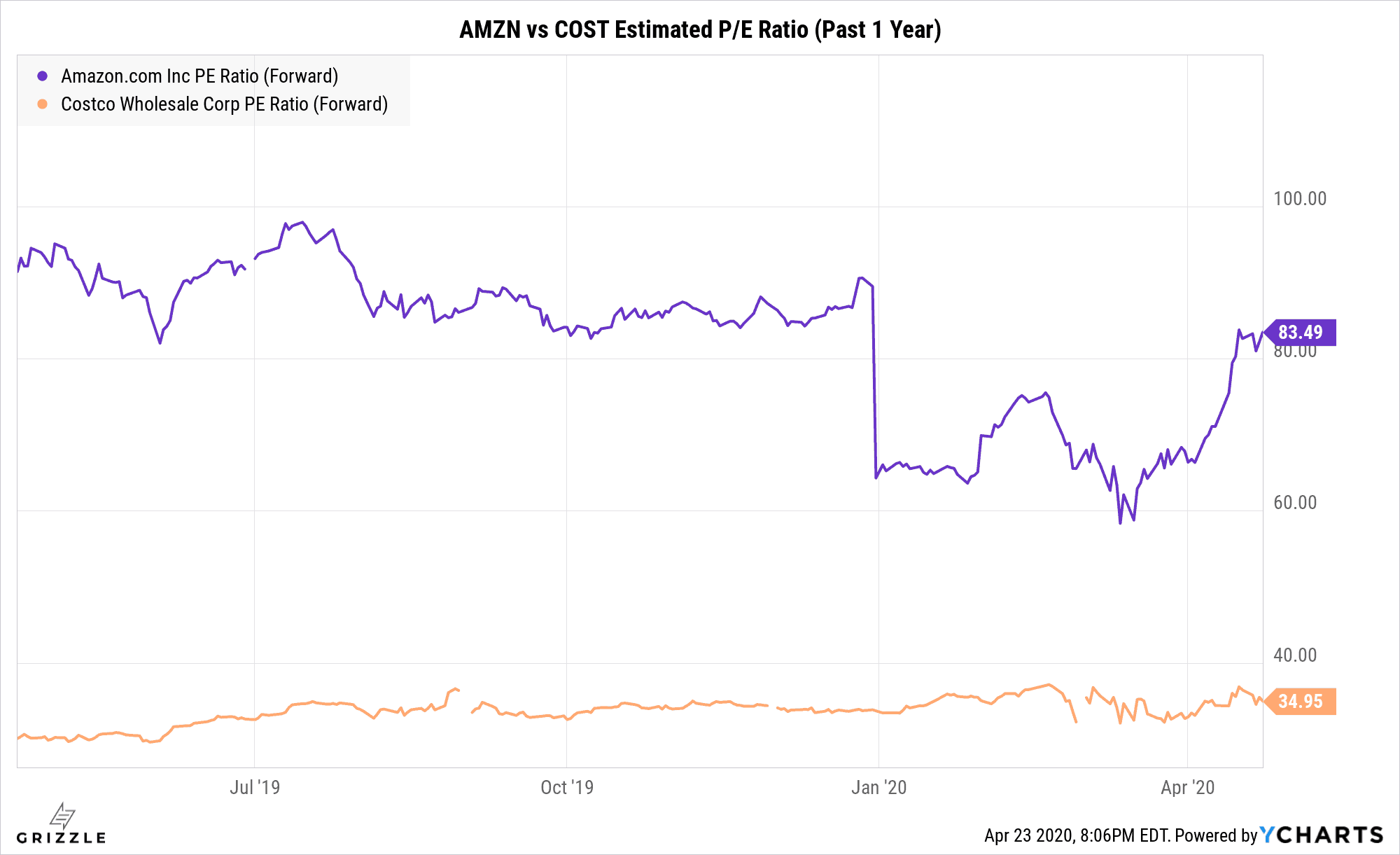

Price to Earnings Ratio

Now let’s look at the valuations of Amazon and Costco.

Amazon has been a highly valued stock for a long time and this includes back during the Great Recession.

We see that even at Amazon’s lowest valuation in the Great Recession which saw the company trade at a PE of around 25, it was still higher than Costco’s PE.

Amazon’s P/E premium has only gone higher, especially with the recent sales surge.

The PE for Amazon sits around 84x, well above Costco.

Bottom Line

It’s hard to go wrong with Amazon stock seeing that it consistently outperforms its peers and the S&P500 regardless of whether or not there is a recession.

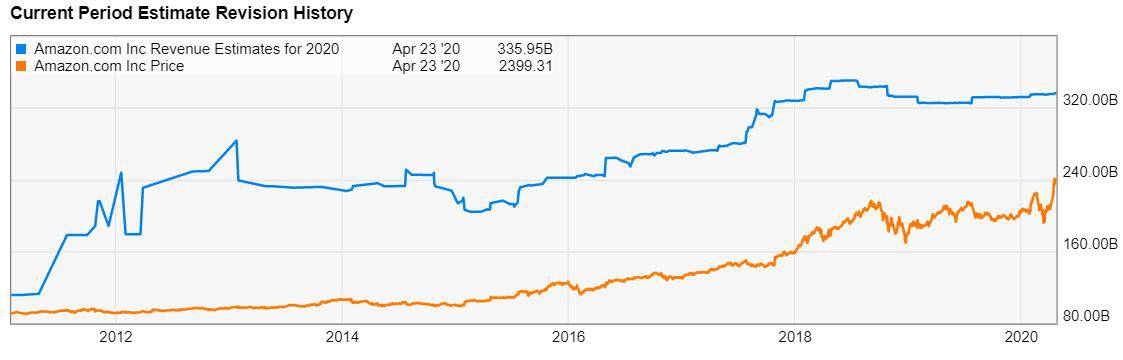

However, at its current PE of 84x, saying that the valuation is frothy is an understatement.

However, analysts revenue estimates really haven’t moved at all since COVID-19 spread across the globe and sales spiked.

When analysts get around to updating their revenue and earnings estimates the P/E will turn out to be lower than 84x most likely.

Revenue Estimates (Blue Line) Haven’t Moved Recently

It appears that Wall Street has already priced a future where Amazon continues to post huge numbers and amazing growth.

It is hard to imagine one losing money when they decide to invest in Amazon for the long term, but given its already high valuation, further upside might be somewhat limited.

Costco might be a better play out of the two seeing as it also tends to outperform the S&P500 during both good times and bad times and its valuation seems a lot more reasonable compared to Amazon.

Don’t forget that Costco also has a dividend, which granted, is very low-yielding coming in at only 0.90% currently, but has grown consistently throughout the past 15 years (so, throughout the Great Recession as well), and has a modest payout ratio of around 32%.

But overall, it seems like both these businesses are extremely well-positioned to handle a recession and ranks among some of the highest quality stocks available on the market right now.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.