Economies and Tourism are on the Mend

Until Thursday’s sell off, the continuing positive tone to stock markets has been primarily driven by the re-opening narrative. True, there have also been the usual supportive comments from Federal Reserve Chairman Jerome Powell and renewed speculation about a cure all COVID-19 vaccine.

Still the key point is that economies are gradually reopening and, so far, there has not been a subsequent material pick up in infections, though the data continues to look much more encouraging in Europe than America.

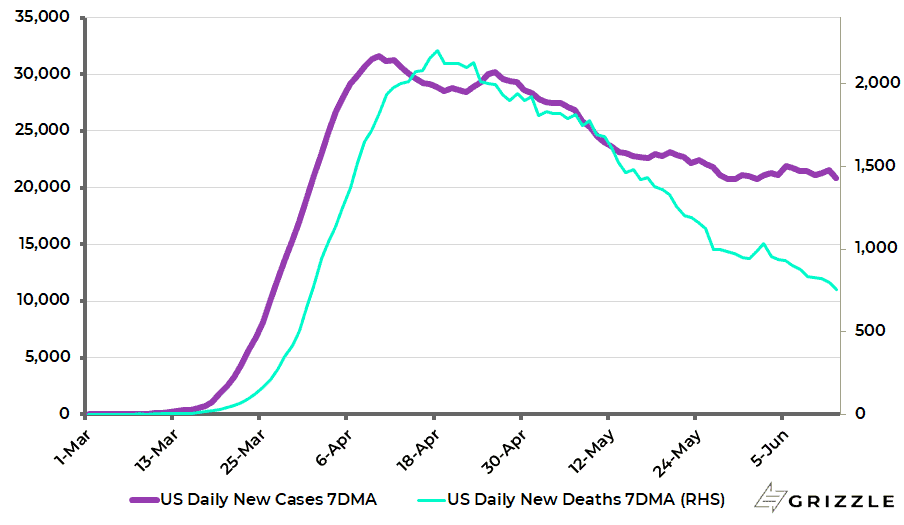

The number of new deaths continues to decline in America though the number of daily new cases has flattened of late. The number of daily new deaths, on a 7-day rolling average basis, has declined to 754 over the past week, down 66% from the peak in April.

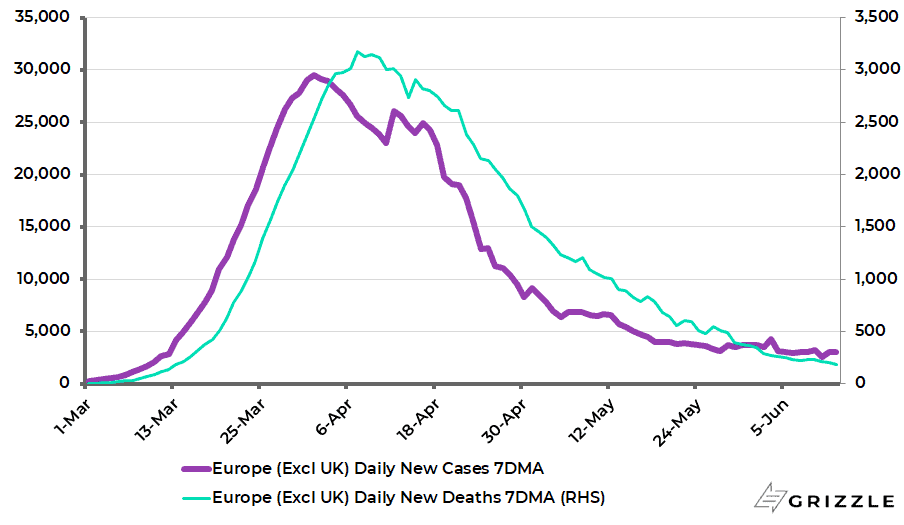

While the average number of daily new cases is down by 34% from the peak in April but has remained broadly flat at around 21,000 cases since late May (see following chart). By contrast the number of daily new cases and deaths in Europe excluding UK, on a 7-day rolling average basis, has declined by 90% and 94% respectively from the April peak.

US COVID-19 Daily New Cases and Deaths (7-day moving average)

Europe (excl. UK) COVID-19 Daily New Cases and Deaths (7-day moving average)

In an interesting illustration of a development the consensus was not expecting, Italy said last month that it would open the country up to tourists from 3 June while Spain will open from the beginning of July.

This flies in the face of the previous talking head narrative that no one was going to take a summer holiday in Europe this year. In this writer’s view there will be massive pent up demand to take such holidays, particularly from younger people, providing travelers do not face quarantines whether on arrival or, upon their return home.

Trump isn’t Waiting for a Miracle Vaccine

What about the vaccine story? It would be wonderful if there is a vaccine and clearly there are massive financial incentives to come up with one. Still, given that there has been no vaccine created to address HIV or for that matter any coronavirus previously, conservative investors would be wise to assume the worst.

It is certainly crazy to say, as some more foolish politicians have pronounced, that economies should stay locked down until a vaccine is developed.

This is why Donald Trump has not based his whole reopening strategy on a vaccine being developed. To have a chance to be reelected in November, he needs the economy to be perceived to be back to normal by the third quarter.

Hydroxychloroquine Hysteria

Meanwhile it was amusing to see the Donald admit to a guffawing pack of hacks on last month that he had been taking the anti malaria drug hydroxychloroquine personally ever since a couple of people around him, including Vice President Mike Pence’s press secretary, had tested positive.

This is not the shock horror story it was reported to be by the media since this writer knows for a fact that the cocktail of hydroxychloroquine and azithromycin has been prescribed by doctors to deal with COVID-19 patients all over the world.

Yet, despite the reality of what doctors have been doing on the front line in terms of day-to-day treatment of Covid-19, the Food & Drug Administration (FDA) issued a safety announcement on 24 April against the use of hydroxychloroquine for COVID-19 outside hospital settings (see FDA Drug Safety Communication – FDA Cautions Against Use Outside of the Hospital Setting or a Clinical Trial Due to Risk of Heart Rhythm Problems, 24 April 2020).

Again the Washington Post in mid-May ran a negative story on hydroxychloroquine (see Washington Post article “The results are in. Trump’s miracle drug is useless”, 17 May 2020). The article noted that two large studies of hospitalised patients in New York City have found the drug was “essentially useless” against Covid-19. But the article was focusing on the results of two surveys of hospitalised Covid-19 patients.

The point about hydroxychloroquine and azithromycin, based on the feedback this writer has received from four doctors operating in four different countries, is that it is effective for most patients if administered when the symptoms first appear. By the time hospitalisation is required it may well be too late.

Lockdown Lunacy vs. COVID-19 Reality

This divergence with what doctors are doing in reality, and the spin in the media, is one of the biggest divergences between perception and reality this writer has ever encountered. Still the good news is that, if there is a cheap and readily available treatment that works for many (if certainly not all) people, it is one more reason why economies should be opened up immediately, thereby ending what continues to be viewed as lockdown lunacy.

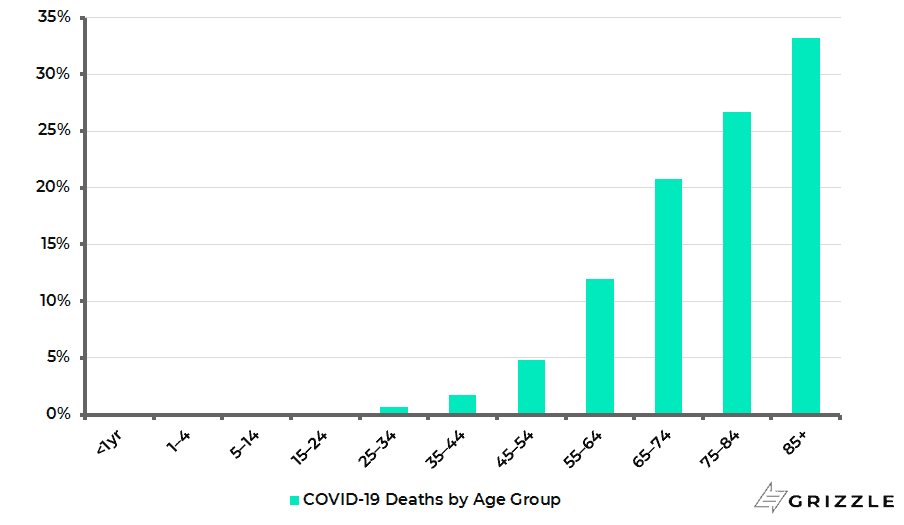

The other, of course, is that the average age of a Covid-19 mortality remains 76 in America, with 81% of the deaths aged 65 or above (see following chart).

US Covid-19 related deaths by age groups

Debt: Millennials Getting Shafted by Boomers… Again!

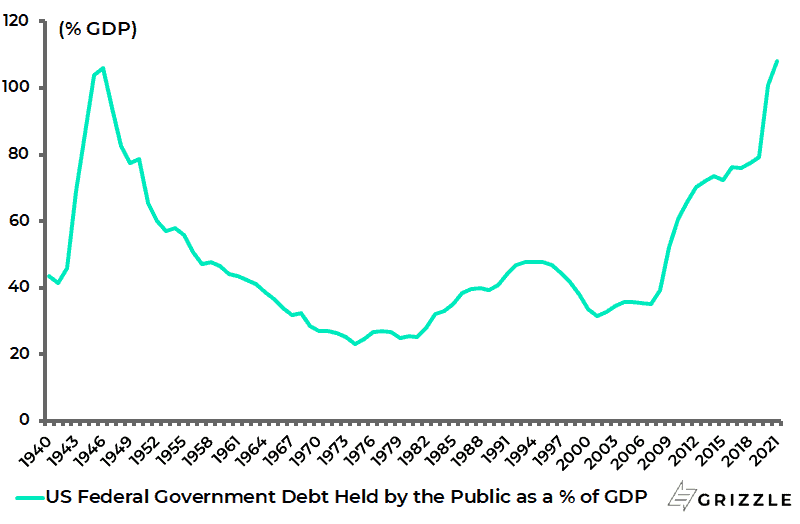

Indeed it is hard to understand why the younger generation were not already on the streets demanding an immediate opening, prior to the recent demonstration concerning racial injustice, given that the millennials are yet again being shafted by the boomers as government debt levels have been massively increased as a response to the crisis.

This is debt they will inherit. US federal government debt held by the public, for example, is now projected by the Congressional Budget Office to reach 101% of GDP by the end of FY20 ended 30 September and a record 108% by the end of FY21, up from 79% at the end of FY19 (see following chart).

US Federal Government Debt Held by the Public as % of GDP

In this respect, this writer continues to read that Covid-19 has caused a dramatic economic downturn. This is nonsense. The virus has not caused the downturn.

It is policymakers’ reaction to the health crisis, namely the decision to lockdown activity, that has caused the unprecedented downturn. The reason for that lockdown ended the moment it became clear that hospital systems were, contrary to earlier fears, not being overrun.

This is why, if there is a sudden realisation that continued lockdowns make no sense, there can be a much quicker return to normal than currently anticipated. At that point there will be much talk about V-shaped recoveries.

At the moment the consensus has moved from predicting a second Great Depression to a U-shaped recovery with much debate about the shape of the U. It is the potential for a V-shape recovery which explains why it has made sense to have exposure to cyclical stocks.

Still it is clear that the risk to this trade is a second surge in US Covid-19 cases where the re-opening had been conducted in a much more chaotic fashion than in Europe, let alone China. This reflects the extreme politicization of Covid 19 in the US.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.