Netflix, a provider of streaming video content (NASDAQ:NFLX) reported results that dissapointed analysts and investors.

The stock is down about 12% in after-hours trading as investors were dissapointed with subscriber additions that were less than expected and guidance for next quarter that was also weak.

The company added 10 million new subscribers in the quarter, 33% above their own guidance of 7.5 million additions but 16% below consensus of 12 million additions.

EPS of $1.59/sh missed consensus of $1.83/sh by 13%.

Revenue of $6.15 billion beat estimates by only 1%

3Q 2020 revenue guidance came in 1% lower than what the market was expecting, showing the positive impact from the Coronavirus is waning faster than investors expected.

Netflix expects to add only 2.5 million subscribers next quarter which is a very weak number when consumers are still banned from most entertainment options besides TV.

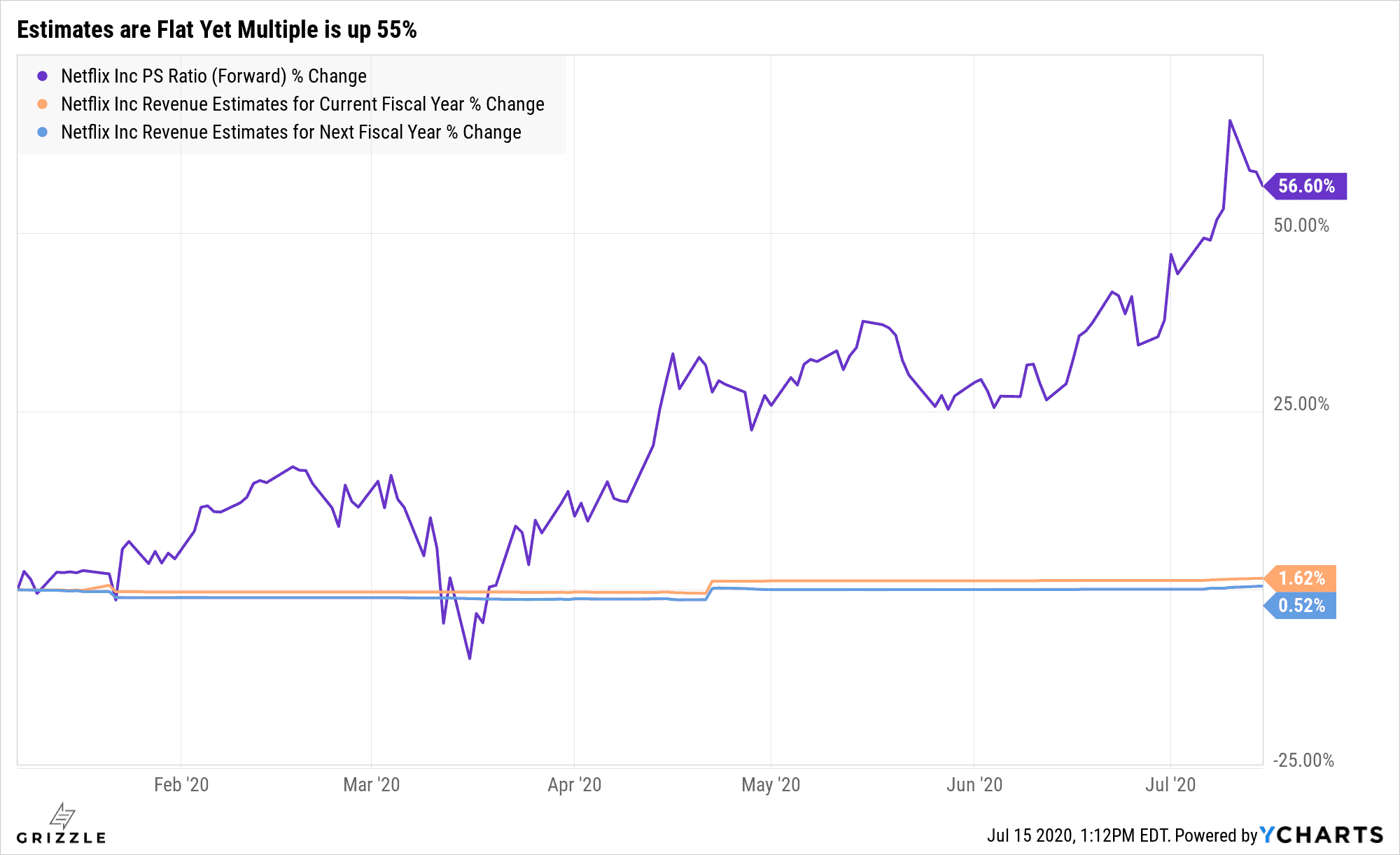

Revenues Estimates Flat but Revenue Multiple up 55% YTD

2020 Stock Price Driven by the Multiple not Underlying Results

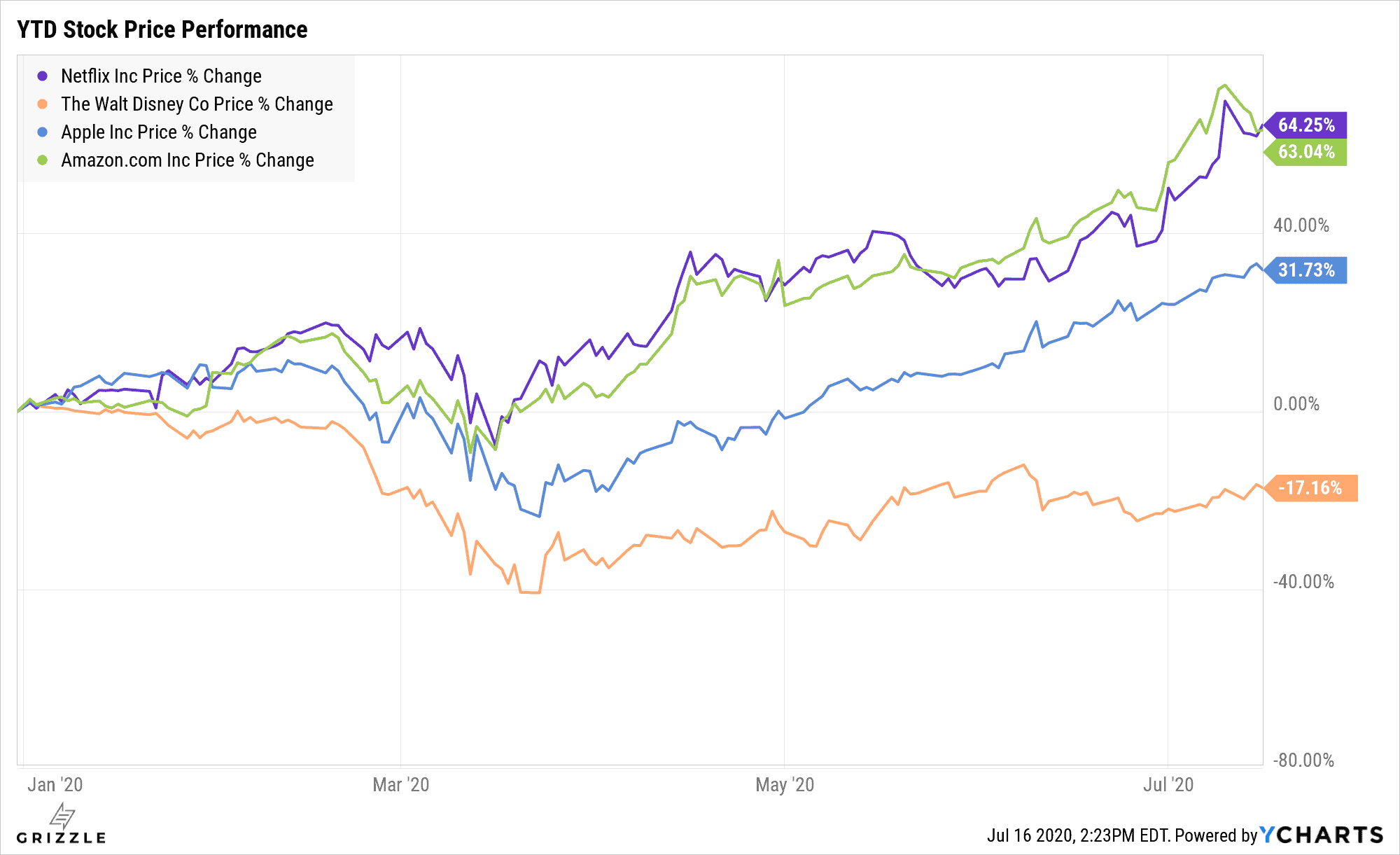

Netflix has handily outperformed two out of three diversified streaming peers so far this year.

Amazon and Apple are the two competitors whose stock prices have also benefitted from an expansion in the multiple more than an increase in revenue or profits.

YTD Stock Price Performance

If we look at how the multiple investors are willing to pay has changed vs expectations for revenue this year, Netflix is much more expensive than where it started 2020.

Even though revenue estimates are basically flat, Netflix’s multiple of sales is up 55%!

A higher multiple means there are heightened expectations built into the stock.

When expectations are high, even small operational misses can hit the stock price hard.

Netflix Stock Price Driven by the Multiple, Not Underlying Sales

Investors are paying a lot more for the privilege of owning Netflix.

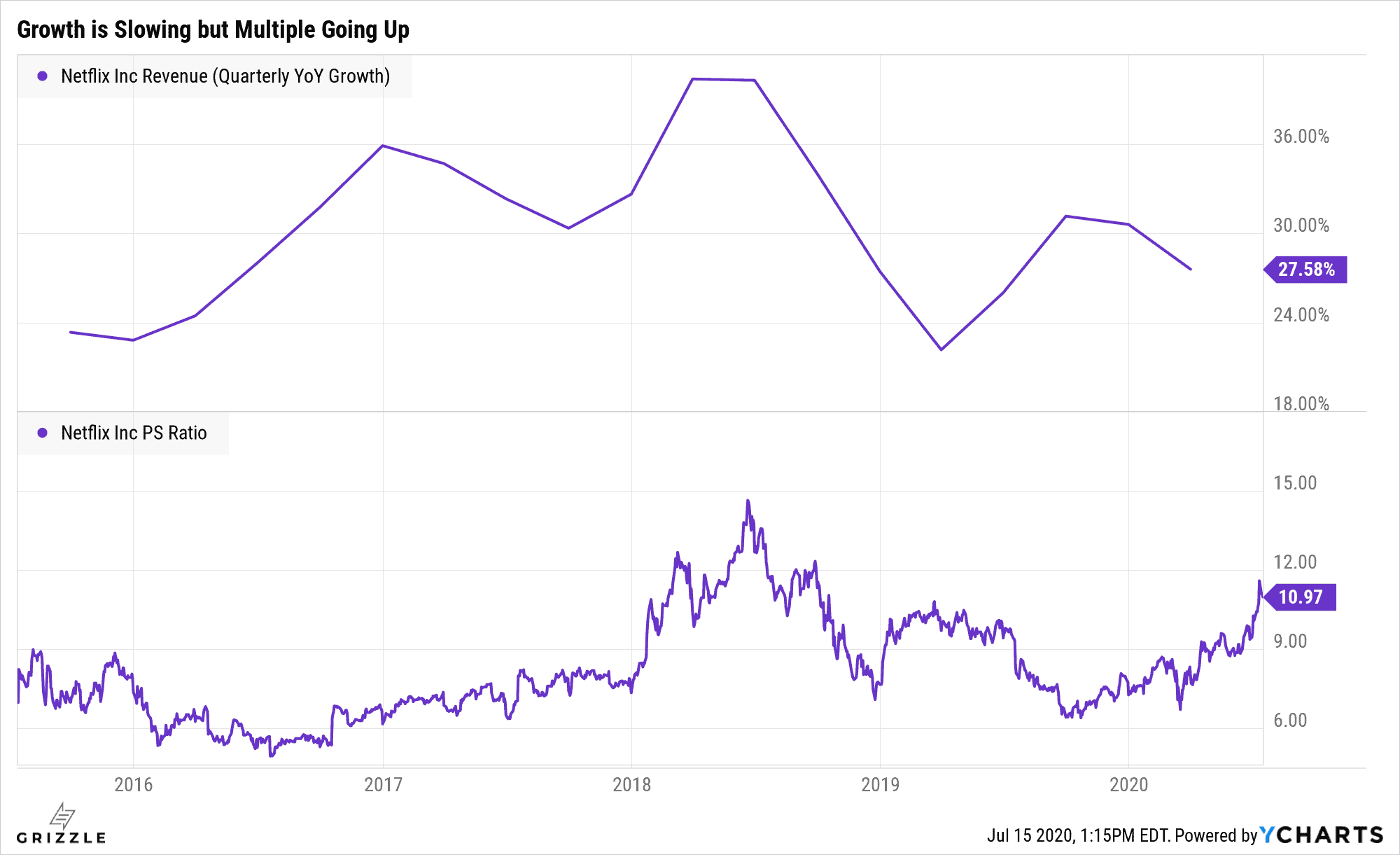

Netflix is seeing slowing growth, but the multiple is back to the days when the company was growing revenue over 30%, not 20%-25% like it’s expected to grow this year.

Growth is Slowing but the Multiple is Going Up

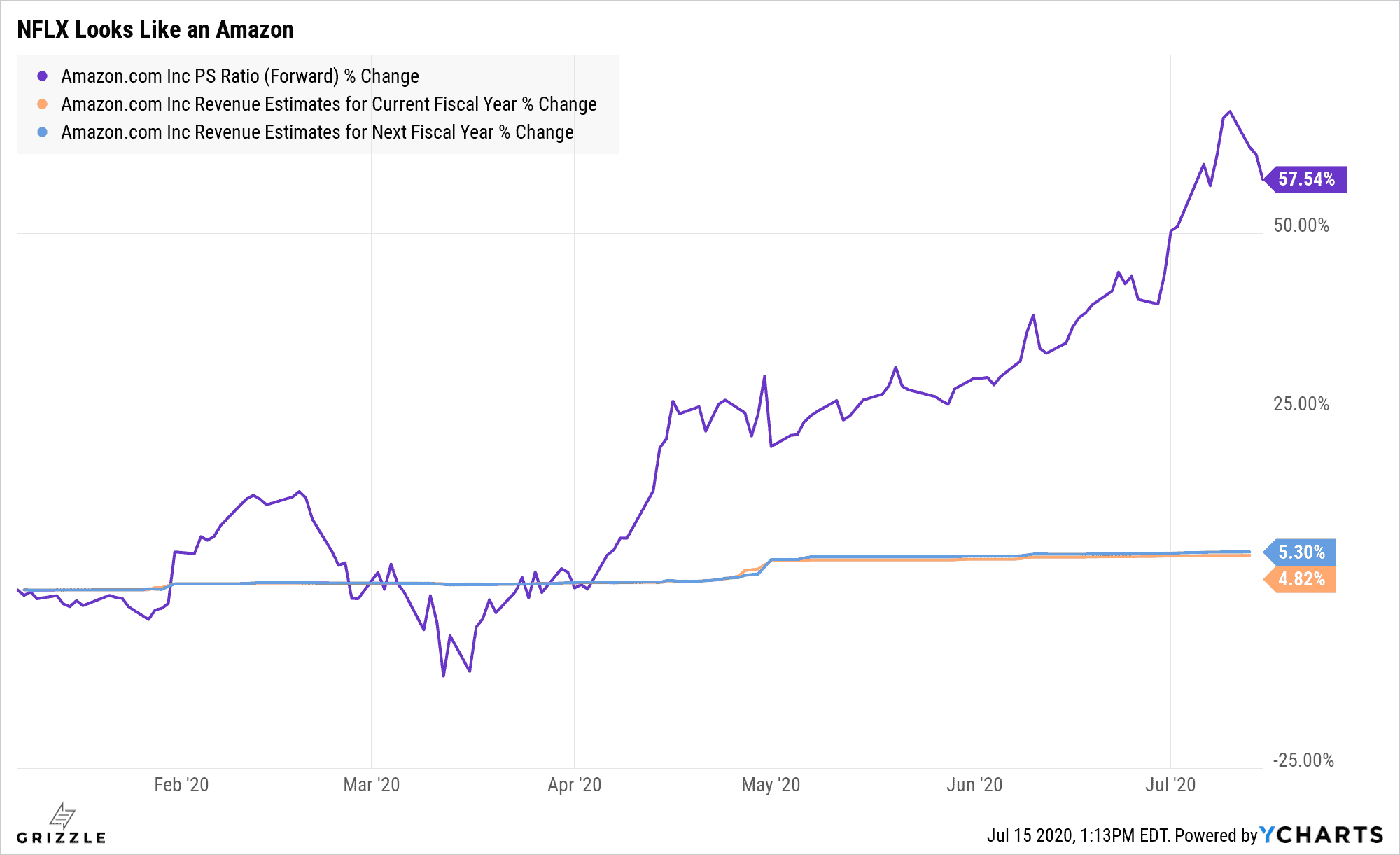

Though if we look at Amazon and Apple, their multiples are telling the same story.

The multiple is way up, but not revenue.

Amazon Stock Price Driven by the Multiple Not Underlying Sales

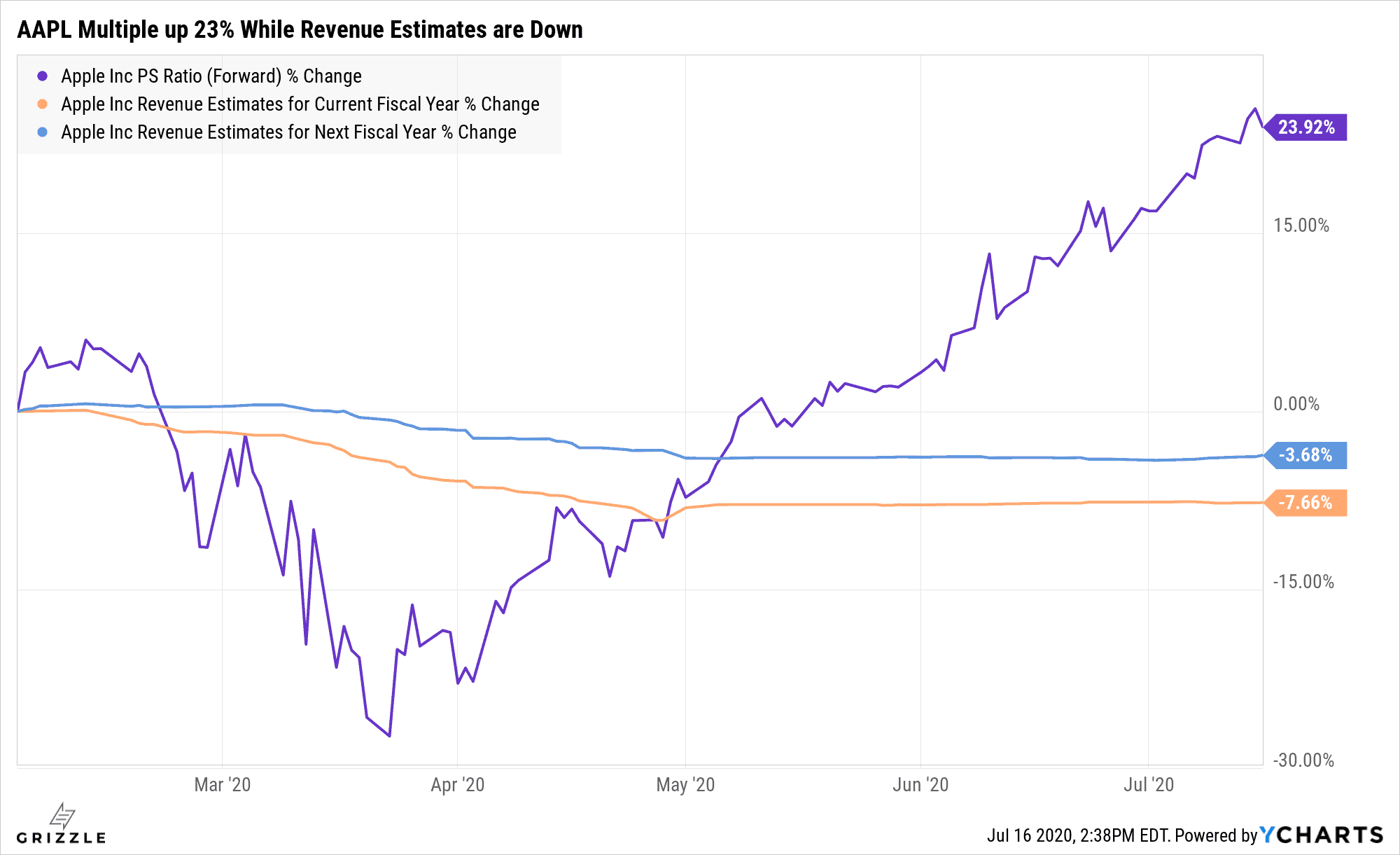

Apple’s multiple is not up as much as Netflix or Amazon, but the stock is still baking in lots of good news on growth and profits.

Apple Stock Price Driven by the Multiple Not Underlying Sales, but Less So

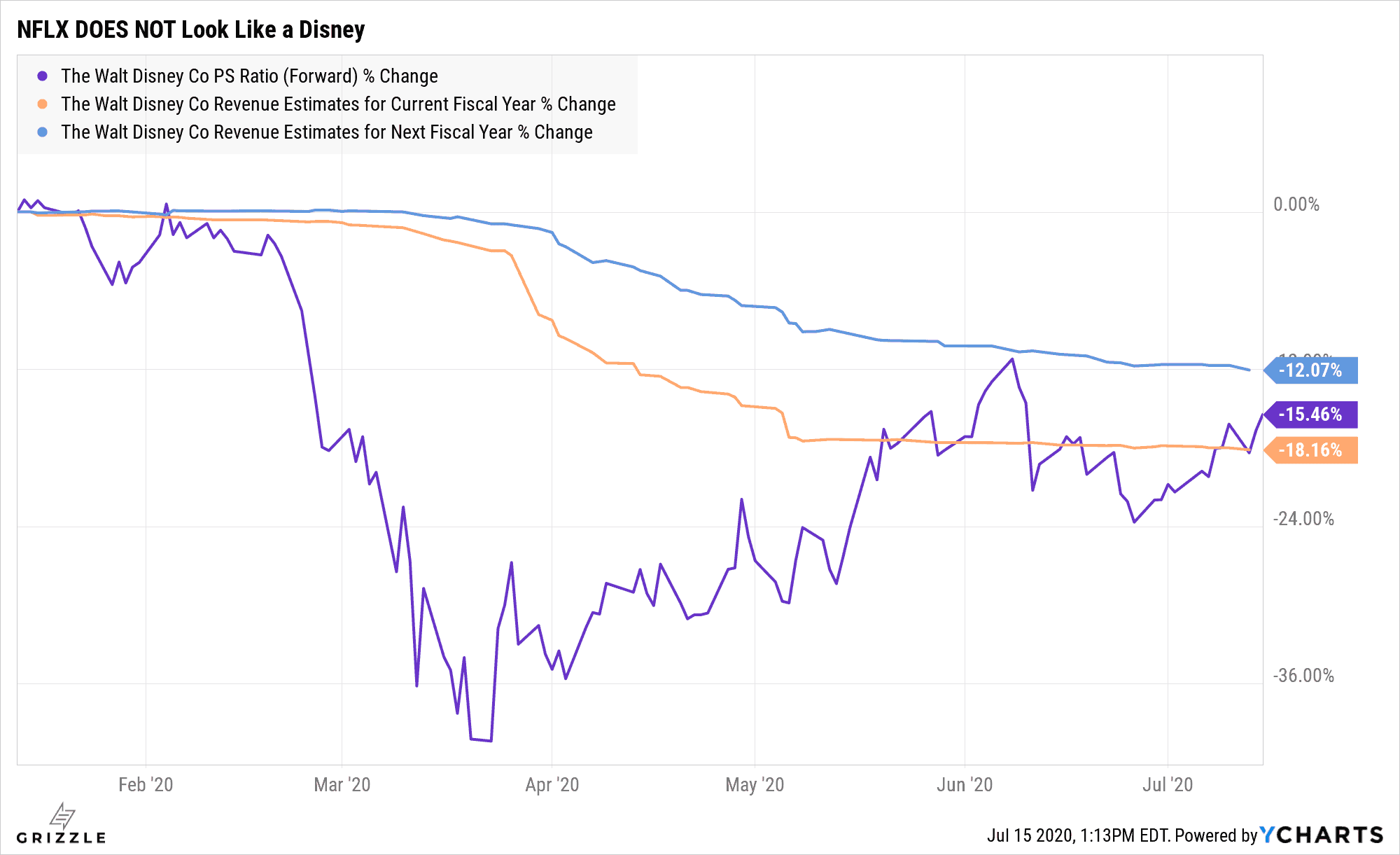

Disney is What we Want to See, Revenue Down, Multiple Down

Netflix remains a long term winner in the trend towards streaming over paying for cable.

We think the stock price will continue to work through 2020 while Coronavirus cases spike then ebb, but we think its likely demand was pulled forward due to recent quarantines.

Growth and rising competition will again cause investor’s concern in late 2020 or early 2021.

Keep playing while the music is on, but we would be cautious buying Netflix stock anytime after the fall.

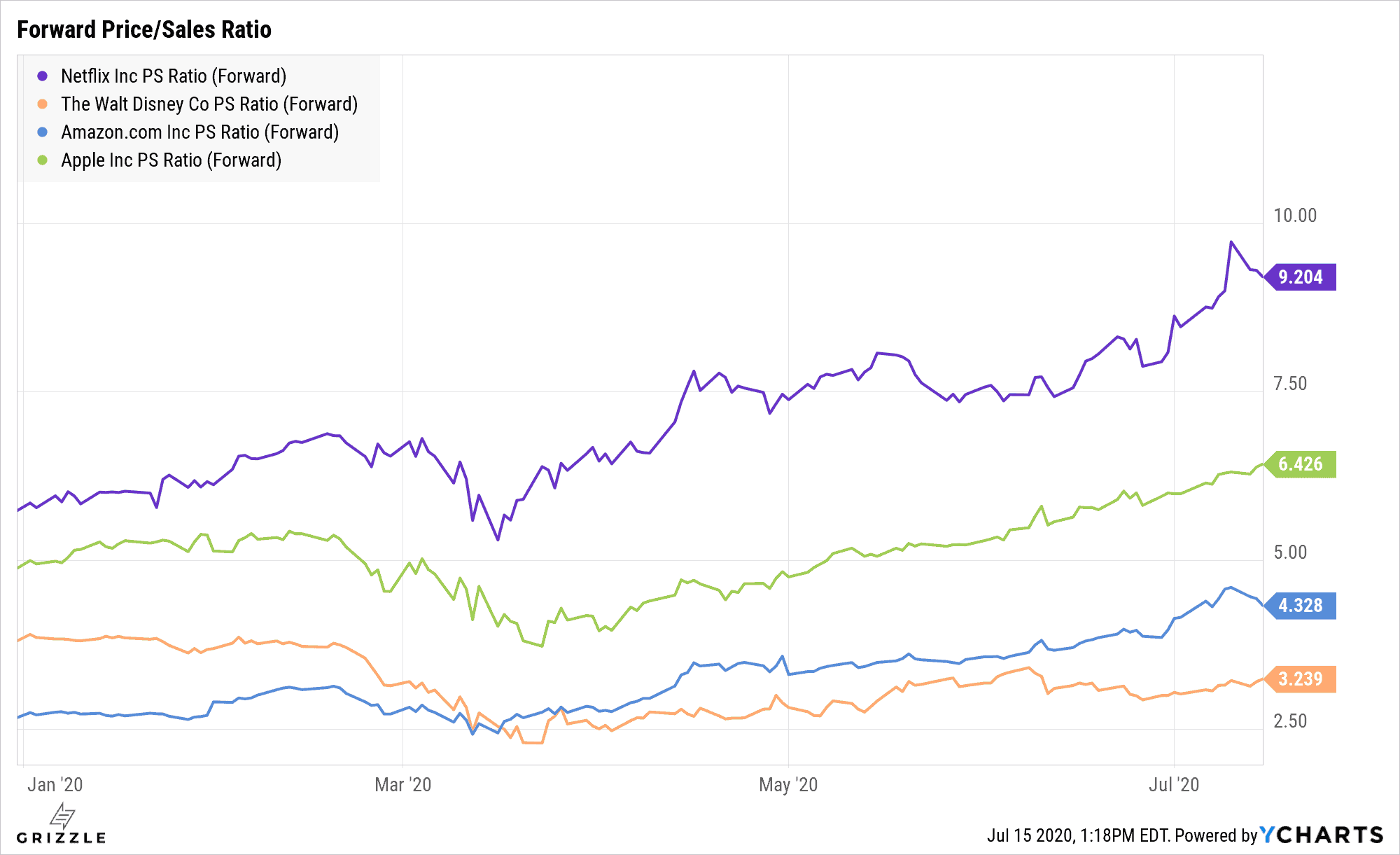

Price/Sales Multiple of Netflix and Peers

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.