COVID-19 Cases: Contained in America, Surging in Europe

It continues to look as if new cases may have peaked almost to the day that the Donald finally told Americans to wear a mask.

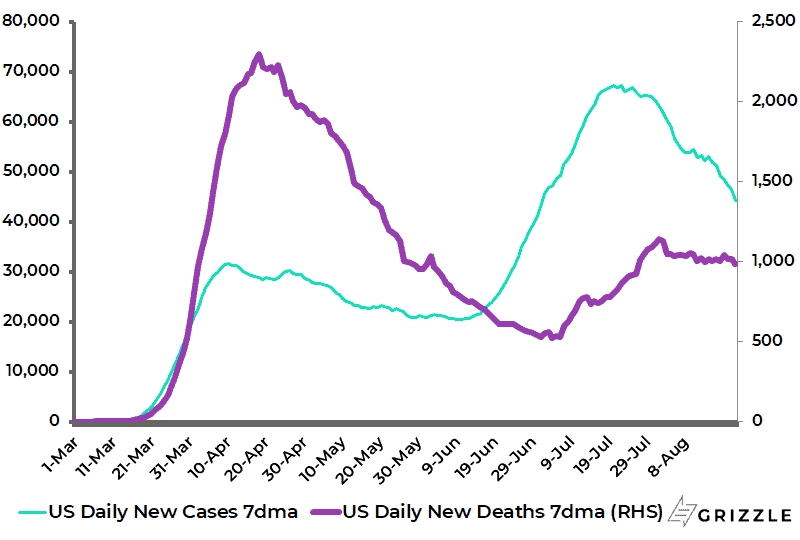

The 7-day average number of daily new cases in America has declined by 37.6% since peaking on 22 July, while the 7-day average number of daily deaths is down 19.7% from the recent high reached on 1 August.

US Covid-19 7-day Average Daily New Cases and Deaths

As for Europe, cases have surged with the opening of borders and the summer holiday season.

But the encouraging point is how little deaths have risen.

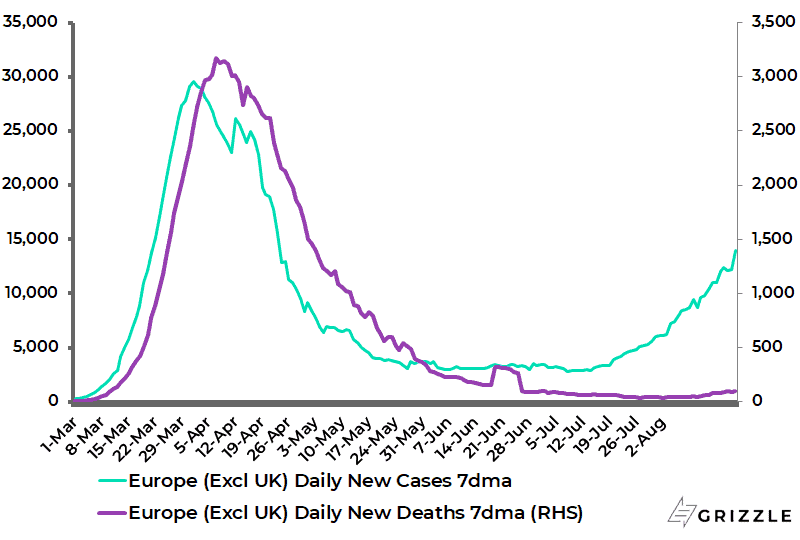

The 7-day average number of daily new cases in Europe, excluding the UK, has risen by 522% since 8 July.

While the 7-day average number of daily deaths rose from 34 on 2 August to 101 on 21 August but has since declined to 45, and it remains 99% below the April peak.

Europe ex-UK Covid-19 7-day Average Daily New cases and Deaths

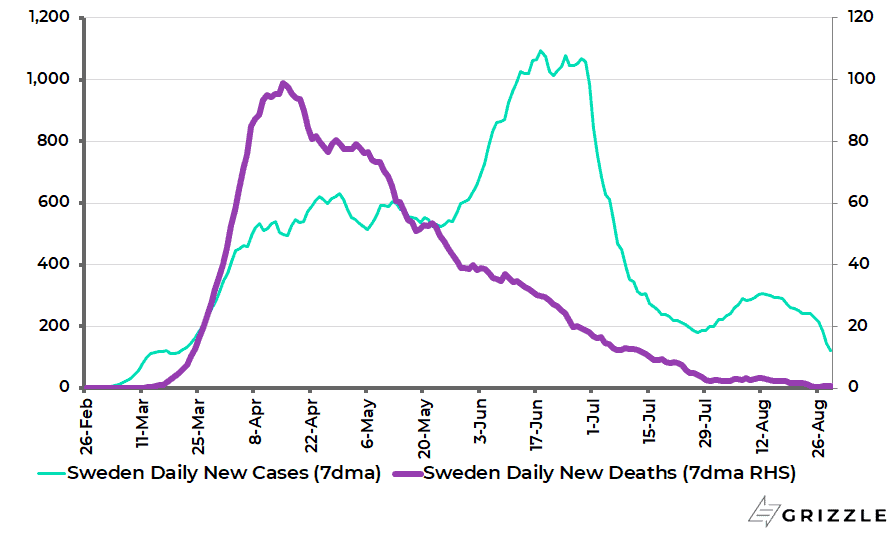

It is also worth highlighting that deaths have all but collapsed in herd-immunity Sweden.

The 7-day average number of daily new cases in Sweden has declined by 89% since peaking in mid-June, while the 7-day average number of daily deaths is down 99% from the peak reached in mid-April.

Sweden Covid-19 7-day Average Daily New Cases and Deaths

US Economic Data Remains Resilient, Especially the Housing Market

Meanwhile, in America, the latest economic data remains remarkably resilient given the failure of Congress to agree a new fiscal package before going into recess on 13 August.

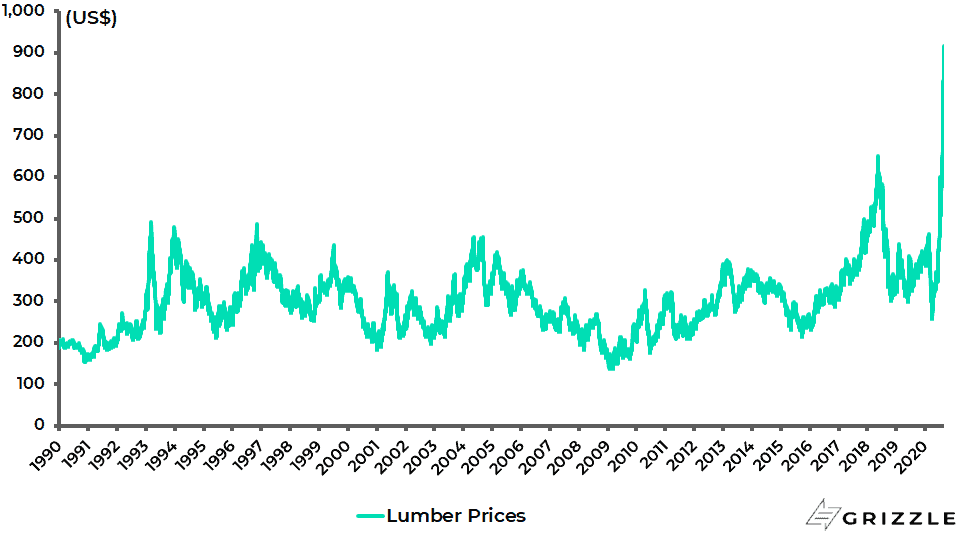

Perhaps the best example of resilience is the strength of the US housing market as reflected in the surge in lumber prices.

Lumber prices have risen by 264% from a low of US$251.5 in early April to a record closing high of US$915.5 on 28 August.

Lumber Prices

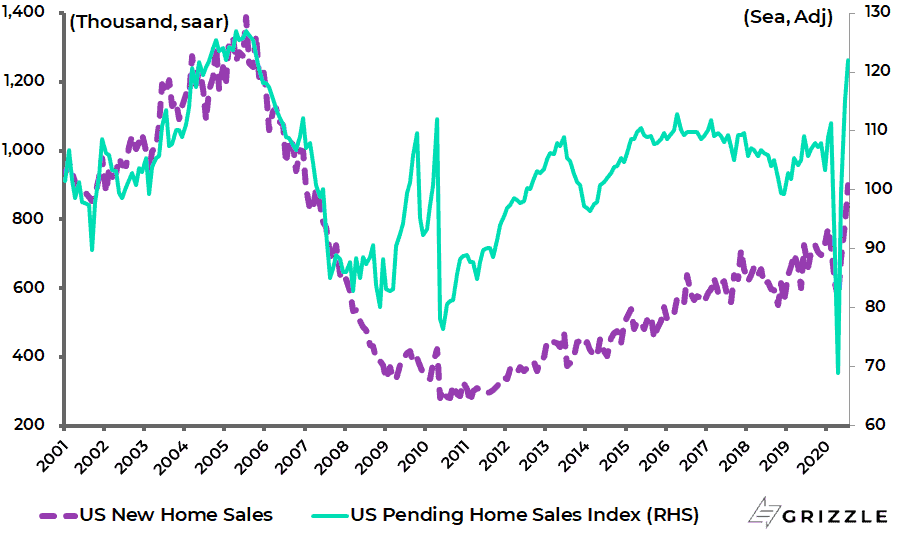

US new home sales and the pending home sales index of existing homes rose by 36.3% YoY and 15.5% YoY respectively in July, while the S&P CoreLogic Case-Shiller National Home Price Index is up 4.3% YoY in June.

US New Home Sales and Pending Home Sales Index of Existing Homes

Reduction in Emergency Unemployment Insurance will be offset by Stimulus Cheques in the Mail

As for the fiscal package, the failure to agree has meant that the extra US$600 per week emergency unemployment insurance expired on 31 July.

Republicans do not want to extend this in full because of the obvious disincentive caused by paying an unemployment benefit much higher than what many could hope to earn working.

The Congressional Budget Office (CBO) estimated in June that, if the US$600/week additional benefit is extended by six months to 31 January 2021, five out of every six recipients of such benefits would receive more in benefits than they would in wages, and employment later this year would probably be lower (see CBO report: “Economic Effects of Additional Unemployment Benefits of $600 per Week”, 4 June 2020).

Still, the executive order signed by Donald Trump on 8 August means that an extra unemployment benefit of at least US$300/week will continue to be paid, albeit with a lag.

Most of the unemployed are now only getting US$333 a week and will probably have to wait another two to three weeks before receiving the increased benefit.

This will lead to a total weekly payment of US$633, down from US$933 before the end of July but still well above the pre-Covid level of US$385. So far, only six states have started paying out the money.

Still, the cut in the emergency unemployment benefit means an immediate hit to household income.

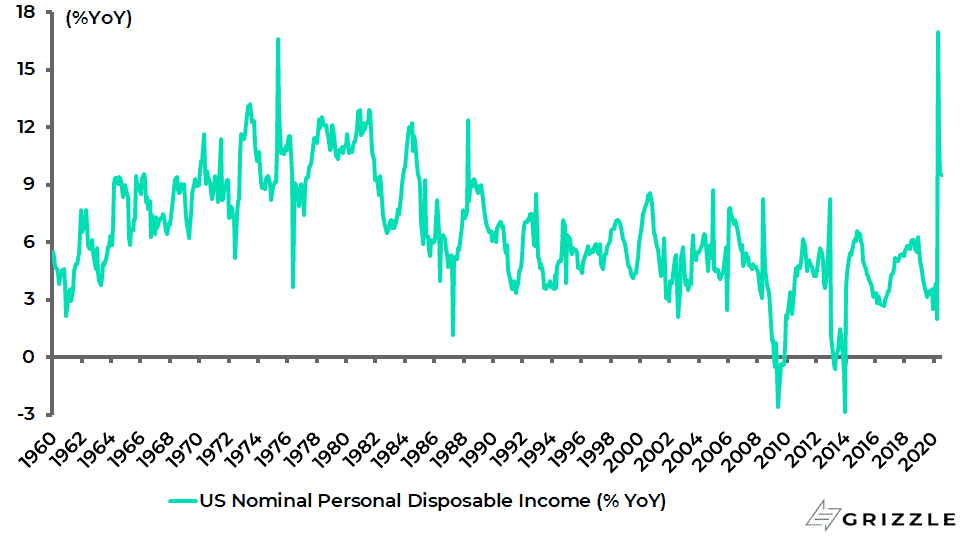

In this context, US nominal disposable income rose by 17% YoY in April and 9.5% YoY in July, compared with 2% YoY in March.

US Nominal Disposable Income Growth

Meanwhile, if a new fiscal package is eventually agreed, as should still be the case, it will also likely include another so-called stimulus cheque since both Republicans and Democrats agree on this point.

Previously under the Cares Act passed in late March, each household got US$1,200 per adult and US$500 per child under 17, with the cut-off for full payment being households earning US$75,000 a year or US$150,000 if married.

Under the Republicans’ proposal, the second round of stimulus cheques will have the same amount and phase-out limits.

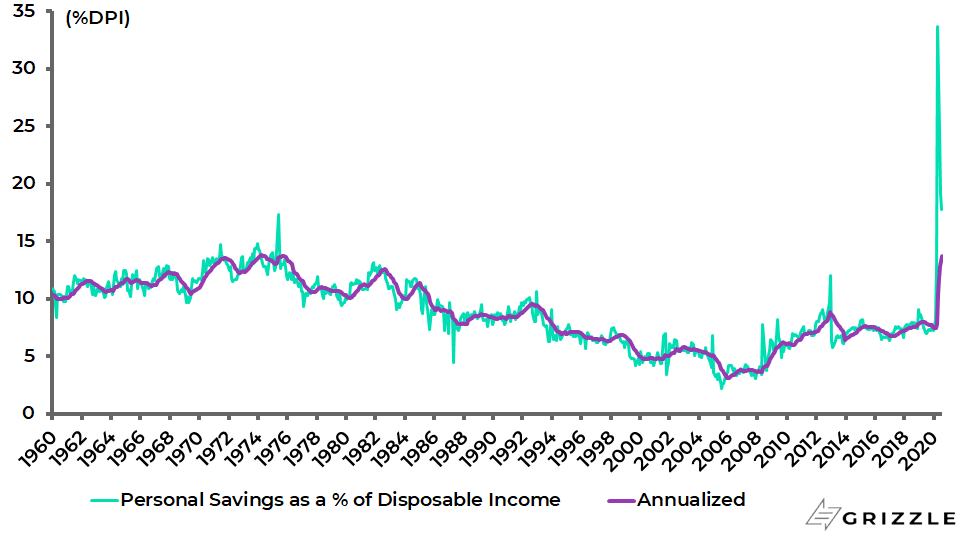

The other explanation for the relative resilience of the American economy is the increase in the personal savings rate as a result of lockdowns and the increased benefits.

The US personal savings rate rose from 7.6% of disposable income in January to 33.7% in April and was 17.8% in July.

US Personal Savings as % of Disposable Income

Meanwhile, the Paycheck Protection Program (PPP) is likely to be given more funding in the anticipated fiscal package.

The Republican proposal is for another US$190bn to go to the programme.

Under the bill, small businesses can apply for a second PPP loan if they meet the Small Business Administration (SBA) revenue size standard, have no more than 300 employees and can show at least a 50% reduction in gross revenues.

The total size of the current PPP scheme is US$659bn.

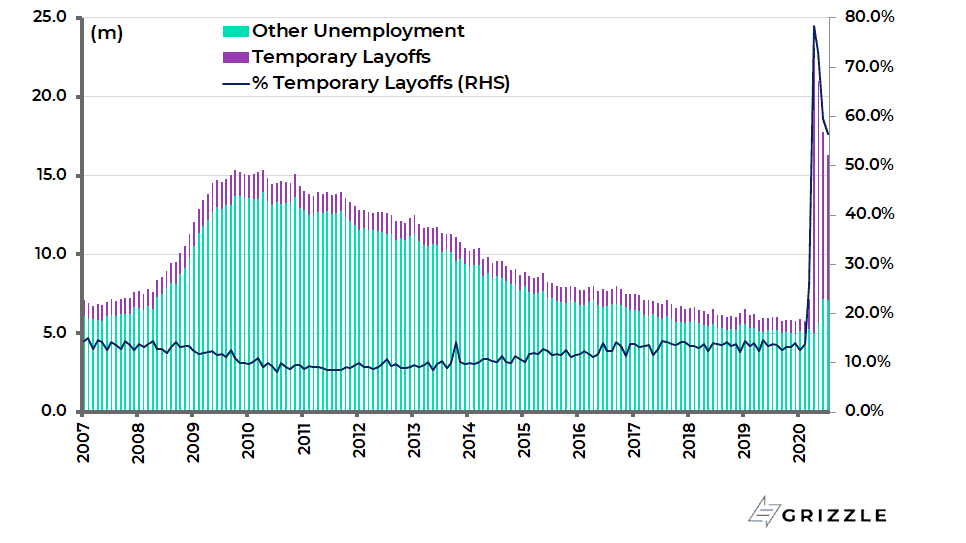

This program is significant because it creates an incentive for companies to rehire temporarily laid off labour.

Unemployed persons on temporary layoffs, measured as those who have been offered to return to work or are expected to be recalled to their job within six months, surged from 801,000 in February to 18.1m in April.

That number has since declined to 9.2m in July and now accounts for 56% of the total 16.3m who are unemployed, though down from 78% of the 23.1m unemployed in April.

If the number of such temporary laid-off workers declines further to the pre-Covid level of 801,000, the unemployment rate would fall to only 5%, compared with the reported 10.2% in July and a peak of 14.7% in April.

US unemployment Breakdown

All of the above highlights both the importance of the bridge financing provided to cushion the impact of the lockdowns and the difficulties of weaning economies off such support.

This point applies not only to America but all other economies which implemented generalized lockdowns.

Big Tech Winning During Lockdown, Regulation Remains the Medium-Term Risk

Meanwhile, one reason there has not been that great a pressure on the politicians to agree a new fiscal package has been because the American stock market has kept rallying, driven primarily by the Big Tech companies whose business models have benefitted from the lockdowns.

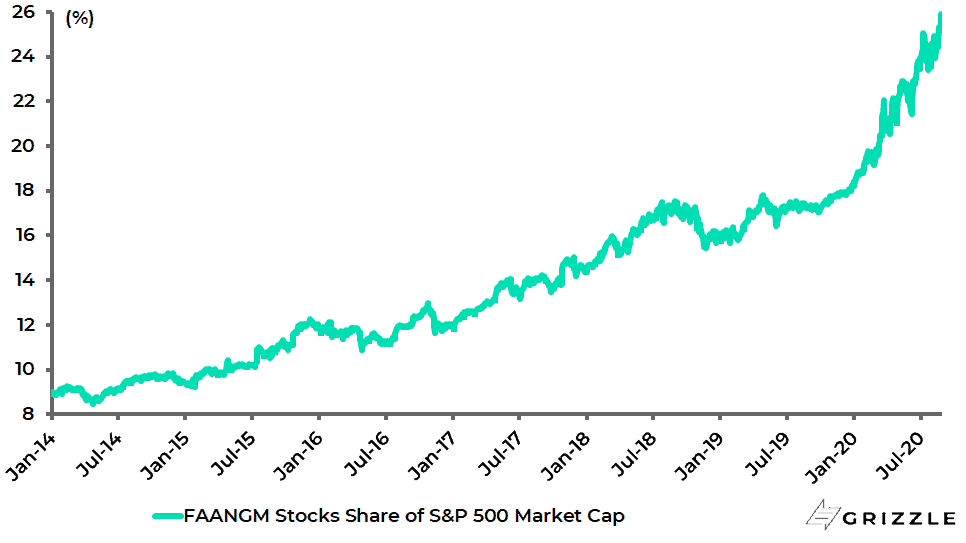

There is no doubting the narrow nature of the Wall Street rally.

But this may not be as extreme as it looks when a premium is put on the quality of the tech giants’ earnings. On this point, Facebook, Apple, Amazon, Alphabet (Google), Netflix and Microsoft account for a combined 25.6% of S&P500 total market cap and 17% of S&P500 2020 consensus forecast earnings.

Big Tech Stocks’ Share of S&P500 Market Cap

Perhaps the biggest medium-term risk for investors in these companies is if there is targeted taxation and regulation of Big Tech.

Targeted regulation and taxation of Big Tech is one of those issues on which the socialist left and the free-market right agree in the same way that both wanted to nationalise the bailed out banks in 2008.

This means that such policies can potentially be implemented whoever wins in November.

What could the policies look like? On the taxation front, it could be as simple as a windfall profit tax.

On this point, Amazon paid US$162m in federal income tax last year while Walmart, its largest competitor, paid US$2.76bn.

On the regulatory front, a long-overdue reform is to make social media platforms responsible for their content in the same way as media companies have always been responsible for content.

Another long-overdue reform is anti-trust action by, for example, forcing divestment of WhatsApp and Instagram in the case of Facebook or YouTube in the case of Google.

Students of American history will know that there is a long and proud history of anti-trust activism.

This has been suppressed in recent decades on the view that nothing matters so long as the end-consumer is getting a cheaper deal.

Such a view no longer makes sense under the lucrative model of surveillance capitalism where users are not paid for their data.

In a world where Facebook and Google have an estimated 61% share of digital ad spending in America, and Google has a 71% share of search advertising, action is again long overdue, though the lobbying power of these companies is formidable.

The virtual appearance in late July of the heads of Apple, Amazon, Facebook and Google in front of the antitrust subcommittee of the House of Representatives committee on the Judiciary may be a prelude to what is coming.

Still on this particular occasion, the questioning by Congressmen was not as narrowly focused on the anti-trust issue as it could have been. This, and the proximity of the presidential election, is why nothing is going to happen in the short term.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.