Canadian Pacific Railway (TSE:CP; NYSE:CP) announced results that beat expectations.

Revenue came in at C$2.07 billion, a slight beat to consensus of $2.02 billion while earnings per share of C$4.82 beat the consensus estimate of C$4.67 by 3% and increased 6% from the same quarter in 2018.

Revenue ton miles, an indicator for the level of fleet activity declined again this quarter, down 3% over last year after declining 1% last quarter as well.

The operating ratio, a measure of efficiency disappointed, increasing to 57% from 56.1% last quarter and 56.5% in Q4 of 2018.

A lower operating ratio means lower costs.

The company released 2020 guidance that effectively met expectations on EPS and revenue.

Management is looking for a return to RTM growth in 2020 after a weak 2019.

The company also announced a 7% increase to the dividend and a buyback of 2% of shares in 2020.

An earnings beat was commendable with such a big increase in costs in the quarter but it doesn’t change the medium-term headwinds facing the entire railroad industry.

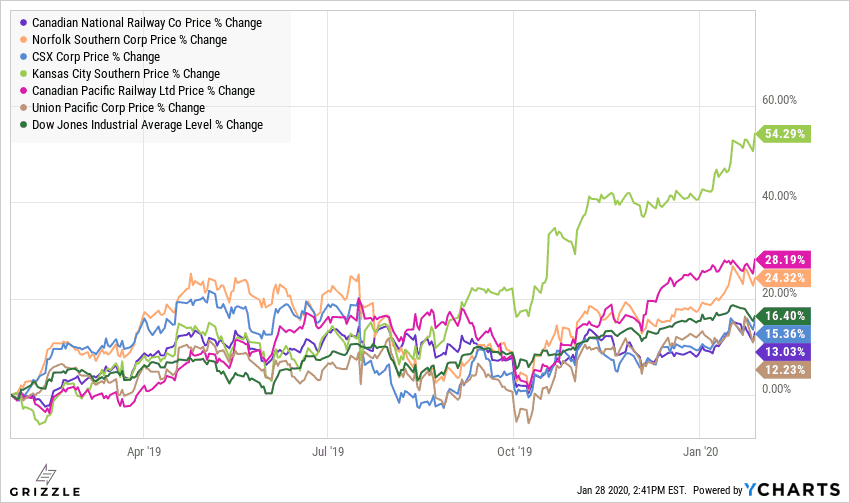

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Even though CP is doing a good job cutting costs and increasing efficiency to offset weaker revenue growth, railroad stocks are not what you want to own near the tail end of a decade long economic boom. These are stocks that perform best when purchased at the tail end of recession and sold a year or two later. [/su_panel]CP Outperforming Most Peers and the Index

CP is leading the pack when it comes to revenue growth.

The legacy of railroad superstar Hunter Harrison is likely still intact at the railroad to the benefit of investors.

Hunter built CP into the most efficient railroad in North America and the company is still benefitting from the organizational processes he put in place.

Revenue Growth is Best in Class

CP continues to have the highest margins due to a lean and mean operational network.

CP margins are still best in class and the new management team is doing a great job keeping costs down as shipping activity slows across North America.

CP Margins are Also Leading the Group

CP did historically have above average debt levels, but since Hunter Harrison resigned from the railroad management has done an excellent job deleveraging.

When an economic contraction eventually comes, and it will, CP will have no trouble dealing with a period of negative cashflow as it has significant wiggle room to borrow debt as a cashflow bridge.

Debt to Cashflow Lowest in the Group

Lastly looking at valuations, CP is still priced rich vs peers and has a weak expected EPS growth rate in 2020.

The market expects -2% earnings growth from CP in 2020 compared to 2%-10% for the other railroads.

So even though the stock has been outperforming, the valuation makes it clear the stock is no bargain.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]If you have to own a railroad stock we would recommend you make it CP. The company’s best in class profitability and growth make it the bellwether of the railroad space in this cycle.[/su_panel]CP Trades at a Premium Multiple of Earnings

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.