Bottom Line:

This quarter, management went out of their way to explain all the ways Cronos (NASDAQ: CRON; TSX: CRON) is different.

While the rest of the industry focuses on low growing costs and ramping up supply, Cronos no longer cares about growing at all.

While everyone else is using raw cannabis flower as their raw ingredient, Cronos is researching an entirely new way to create cannabinoids.

These changes in strategy may make perfect sense over the long term, but in the here and now, Cronos is a cannabis grower stuck in a market with prices in freefall and volume growth disappointing expectations quarter after quarter.

Cronos investors need to understand they are now invested in a cannabis biotech play.

Get Ready for Lower Margins and a Higher Burn

Cronos’ bet on cannabis from yeast may well turn out to be a home-run.

But in the here and now, the decision to pivot away from in-house cannabis cultivation will have a big impact on financial results.

Cannabis in the wholesale market still trades at a 100% premium or more to the cost of growing your own.

What this means is Cronos is going to have higher costs and will generate lower margins on their sales compared to a low-cost grower like Aphria, Village Farms, or Zenabis.

Cronos is making a bet that eventually they can buy high-quality cannabis cheaper in the market than they could grow it for themselves.

We think this is a reasonable bet to make, but it will take time for prices to fall to that point and in between Cronos is going to feel the squeeze.

Investors now have lower margins and a higher burn rate to look forward to.

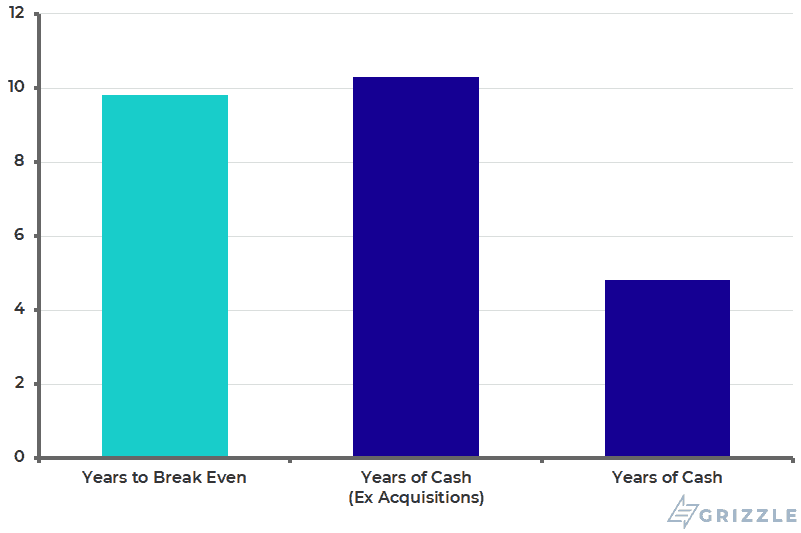

At Cronos’ current growth rate and gross margin, it is 10 years away from breaking even.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]At the current quarterly cash burn rate, Cronos’s war chest from Altria will last 5 more years including acquisitions or 10 years if they grow organically. [/su_panel]Years of Cash vs Years to Breakeven

Biotech research takes time, and in the interim Cronos investors are now looking at deeper cashflow losses and slower growth.

Investors better make sure they are on board because management is now playing the long game.

Earnings Review

A deluge of quarterly reports begins arriving for the North American cannabis industry today, with all eyes on loss numbers as stock prices continue to sag. Cronos Group Inc. (NASDAQ: CRON; TSX: CRON) reported surprisingly strong revenue for the quarter ending Sept. 30, 2019 given that overall shipments to the provinces were only up 6% through August.

This quarter was notable for the Cronos acquisition of Redwood Holding Group, which marks the company’s expansion into U.S. CBD sales with the Lord Jones brand.

Cronos’ revenue of $12.7 million in the quarter was up 24% over last quarter driven by revenue from Redwood. If Redwood is stripped out, revenue was up only 17%. Around 9% of that revenue came from Canadian extract sales, with a total 3,142 kilograms of product sold during the three-month period.

Most importantly the selling price of cannabis in the quarter fell 42% to $3.75/gram from $6.50/gram demonstrating that price compression is already here.

Cronos management said they’re meeting their supply commitments with even more wholesale flower instead of flower grown in their own greenhouses which increased costs in the quarter.

This decision explains why the gross margin fell 50% this quarter to $1.71/gram, an industry low.

Cronos reported positive net income in the quarter, but results were totally attributable to accounting shenanigans related to stock options.

When we ignore the gain on derivatives Cronos is still deep in the red.

On the positive side, Cronos still has a war chest with C$2 billion in cash and cash equivalents as of Sept. 30.

Gearing up for the investor conference call to discuss those numbers, Chief Executive Officer Mike Gorenstein commented:

The company also announced the launch of the PEACE+ brand today, with new hemp-based CBD tinctures in that line due to hit 1,000 convenience stores through the Altria Group distribution network.

Additional international expansion is still underway, as the Cronos site in Israel has finished construction and is now undergoing Good Manufacturing Processes certification and expected to begin producing products in 2020.

Cronos stock saw a slight uptick this morning to $8.47 a share, but has given up all of those gains and is down 2% in afternoon trading.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.