Bottom Line

The leak of acquisition talks between Cronos and Altria is a classic tactic used by companies to support their share prices prior to raising money.

Cronos was likely hoping the news would bring enough positive sentiment into the share price to support a much-needed capital raise.

As soon as a company goes public with acquisition talks, the deal is effectively dead.

Cronos is a company that as of Sept. 30 had $41.5 million of cash against a cash burn rate of $47 million a quarter.

Given that last quarter’s EBITDA was negative we think this is a company that may be facing a true liquidity crisis.

Why Would Altria Pick Cronos?

Cronos is not the only company Altria is evaluating for a potential investment.

Both Aphria and Tilray have also held talks with Altria about a possible investment, according to the Financial Times.

Cronos likely asked for a meeting, promising a new revolution in cannabis science and then used the meeting as collateral for a future leak.

On a fundamental basis, if we compare the attractiveness of all three producers, Cronos looks to come in a distant third place.

Capacity

First, Cronos is the smallest of the three targets, with current capacity of 7,500 kg and planned capacity of ~75,000 kg by the end of 2019.

This compares to Aphria with 35,000 kg of capacity now and 255,000 by April 2018 and Tilray with 20,000 kg of current capacity and 140,000 kg planned for 2019-2020.

If Altria wants access to raw cannabis material at scale, Cronos is the weakest option of the three.

Product Portfolio and Clinical Research

If Altria is looking for a deep portfolio of cannabis consumer products, there are much better targets than Cronos.

CannTrust has been the leader in building a deep bench of consumer products and developing novel delivery methods such as its nano-encapsulation technology.

Cronos just recently released branding for many of its dried flower products and has not publicly given any indication that it has infused cannabis products ready to go.

Moving to medical research leadership, Cronos is behind peers, including Tilray and Aphria.

Cronos has no R&D expense on its income statement while peers are spending 3%-10% of sales on R&D each quarter.

Even their R&D partnership with Ginkgo Bioworks, which looked exciting on the surface, is targeted at bringing down production costs, not inventing new patient therapies for cannabis.

According to the fine print, Ginkgo isn’t even working with cannabinoids currently and needs numerous licenses before it can start using the cannabis plant in its research.

Bottom line, a medical research leader Cronos is not.

Stock Price

If Altria is looking to get any value out of a cannabis deal, Cronos is one of the worst places to start.

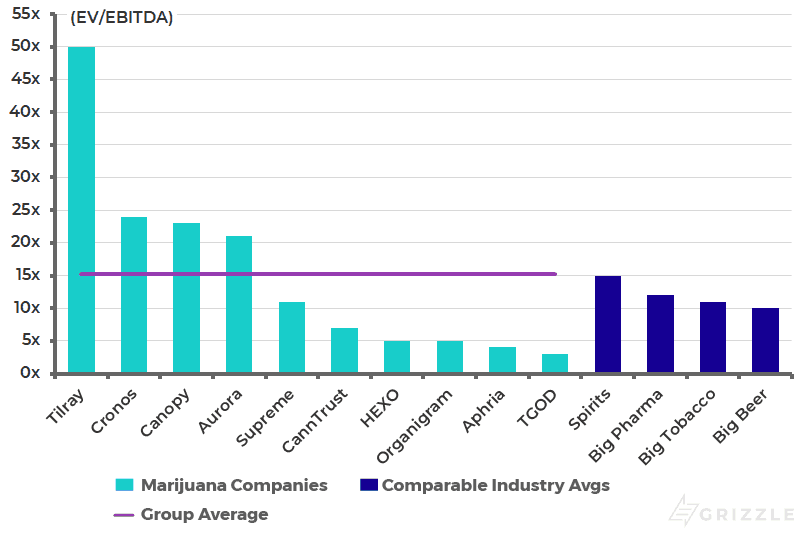

Based on Grizzle’s estimates Cronos is trading for 24x 2020 EBITDA, a measure of cashflow.

This is the second highest multiple in cannabis after Tilray, another nose-bleedingly expensive name.

A sophisticated corporate development team knows that if you are buying a company priced for perfection it is exceedingly hard to make a decent return on your investment.

Cronos is both smaller than peers and more expensive and Altria knows it.

2020 EV/EBITDA Multiples

Cronos Running Low on Cash

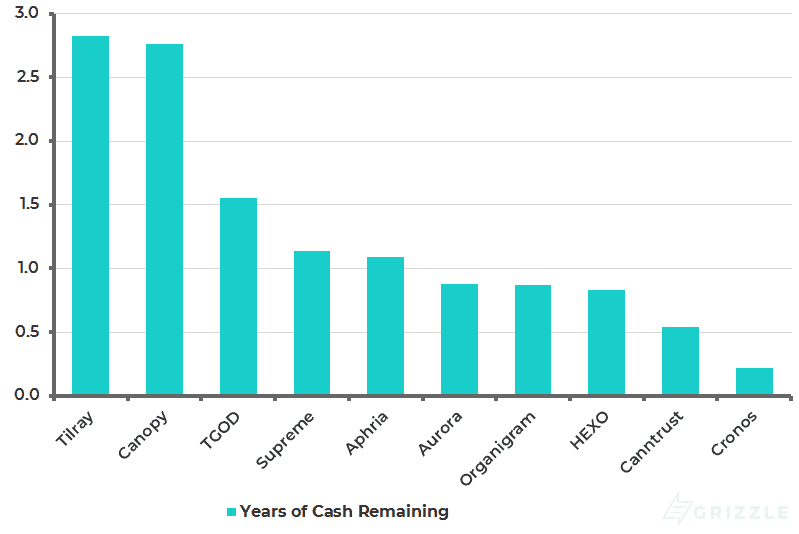

In November Grizzle published its Cannabis Scorecard looking at which licensed producer was best positioned from a liquidity and cashflow breakeven standpoint.

Cronos scored last in the liquidity ranking with an estimated 2.5 months of cash remaining. This would carry the company into mid-December if the current spending rate on construction and operations continued.

Years of Cash Remaining at Current Burn Rate

Cronos still has to construct the 850,000 sq ft greenhouse it is building through the Cronos GrowCo JV which will likely cost at least $100 million, or at least $50 million net to Cronos based on the construction costs of other large greenhouses.

Other drains on cash will likely come from the buildout of the new LATAM venture and final construction on the Peace Naturals facility in Canada.

The company does have a potential lifeline with $28.6 million remaining on a construction loan agreement, however, if they draw this entire loan down, the interest expense alone will total $4.2 million a year, more than Cronos generated in revenue last quarter.

Add this $4.2 million into operating costs and you have a company that needs to sell 6,400 kg a year for $7.30 a gram just to break even and stay in business.

Cronos is at an annualized run rate of 2,000 kg currently so needs to triple sales by next quarter.

Cronos is up against the wall and needs either perfect execution or a new capital raise to avoid running out of money.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.