Bottom Line

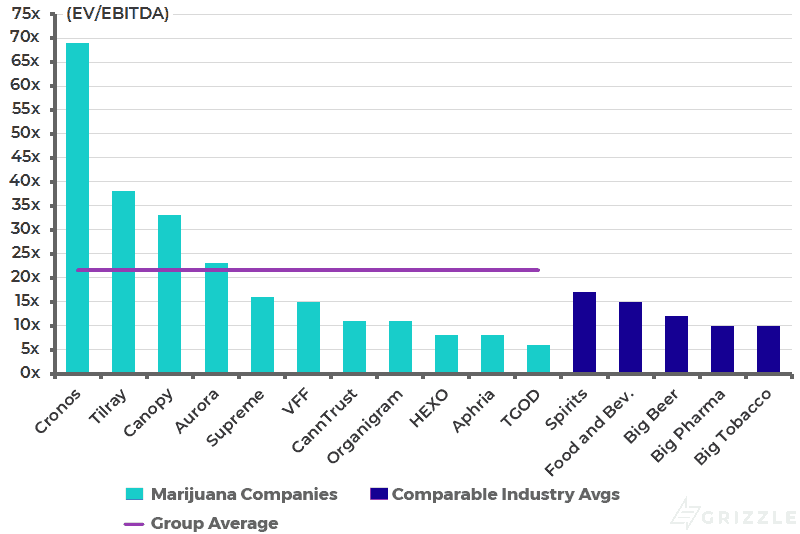

In a surprising twist, Cronos has snatched the crown for most expensive global cannabis company from perennial leader Tilray.

With a flood of new shares issued to Altria for a $2.4 billion investment, Cronos now trades at 70x EBITDA in 2020. This is 80% higher than Tilray, which is already overvalued and triple the Canadian average.

Estimated Enterprise Value to 2020 EBITDA

Overall what the earnings release makes clear is Cronos will need to do a big transformative deal with their pile of cash to support the current stock price.

Investors have a choice of buying stocks in Canada, a legal market that has stopped growing, for 30x sales or they can buy U.S. multi-state operators growing at 200-300% a year for only 9x sales.

U.S. stocks provide far more growth for a cheaper price and provide a measure of downside support should investors get skittish or global stock markets fall.

We think Cronos is a “show me” story for the rest of 2019.

Operational Review – Per Gram Costs Disappoint

While Cronos’ quarter over quarter cannabis sales doubled from 514 kg to 1040 kg, this is nowhere near the 1,600 kg breakeven mark we projected.

More concerning, however, is the fact that their revenue only increased by 50% to $5.6 million from $3.8 million in Q3 2018. This makes their revenue per gram $5.60, second lowest behind only Hexo.

Revenue Per Gram over the Last Six Months

These poor production numbers led to a drop in EBITDA from -$3.3 million to -$7.9 million. While this would be a red flag in any other industry, for Canadian cannabis producers Cronos’ 140% decrease leaves them in the middle of the pack.

Below you can see they record the fourth largest loss per gram among Canadian peers (5th best!). Organigram is the only cannabis grower in North America generating positive EBITDA.

So far it looks like economies of scale have not yet kicked in for many growers.

EBITDA per Gram over the Last Six Months

Looking deeper, the significant drop in EBITDA can be attributed to an ~80% increase in operating expenses quarter over quarter. Specifically, the big factors compared to Q3 2018 were sales and marketing, which increased ~330% to $2.6 million, and first-time R&D expenses of $2.4 million.

Surprisingly, their production costs saw a ~10% decrease from $3.3 per gram to $3 per gram, making them the third most efficient producer among Canadian peers.

This is perhaps the only positive from their operations, but take it with a grain of salt. Cronos sold recreational cannabis for only $3.50 per gram after taxes which is not enough margin to generate a profit when your costs are only $0.50 lower.

Until they can increase production while keeping a lid on operating costs, it won’t make a difference how cheap their product is, they won’t be profitable.

Production Costs Per Gram Over the Last Six Months

These production costs gave Cronos a gross profit per gram of $2.4, third lowest among Canadian peers.

Gross Profit Per Gram Over Last Six Months

The Outlook – Cash Rich but Priced for Perfection

While their per gram numbers would normally be concerning, with the recent injection of cash from Altria, Cronos will have time and capital to make improvements.

Their current cash position of $2.44 billion paired with a cash burn rate of $50 million per quarter leaves them with over 12 years of cash remaining. While they have significant plans to improve operations through their Cronos GrowCo JV and Latam buildout along others, investors should also expect R&D and M&A activities to receive a boost if they have any desire to keep up with peers.

The one true positive of Cronos is that investors will not have to worry about further dilution (beyond the massive Altria deal) as they are now the second most cash-rich cannabis company behind only Canopy.

However, from a valuation perspective, Cronos will basically have to do a transformative deal to move the stock any higher from the nosebleed levels it currently enjoys.

If Cronos is to fundamentally trade at a 15x EV/EBITDA multiple, in line with food and beverage peers the company will have to sell every gram of its planned 83,000 kg capacity for $43.

The company currently makes $5.40 per gram.

There is a very high probability Cronos disappoints the market in the coming 12 months unless management adds another 500,000 kg of capacity or starts selling drinks, edibles, and medicine for much higher per gram prices.

We recommend investors take a hard look at their holdings and consider rotating from Canadian cannabis names into U.S. multi-state operators until the legal market in Canada shows some signs of life.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.