This column has not yet discussed the emerging world of cryptocurrencies. Still this area entered the formal financial service world in mid-December when the Cboe and the CME in Chicago started trading Bitcoin futures on December 10 and December 17, respectively.

Like seemingly everyone else, this writer is of the view that blockchain technology is potentially groundbreaking and is an area certainly worth investing some dollars in. But the risk is that the speculative fever that surrounded Bitcoin trading until recently, amid growing evidence of retail investor participation, causes a dramatic sell-off which, temporarily at least, blows up the whole blockchain ecosystem.

An Asset Class Waiting to be Smothered by Regulators

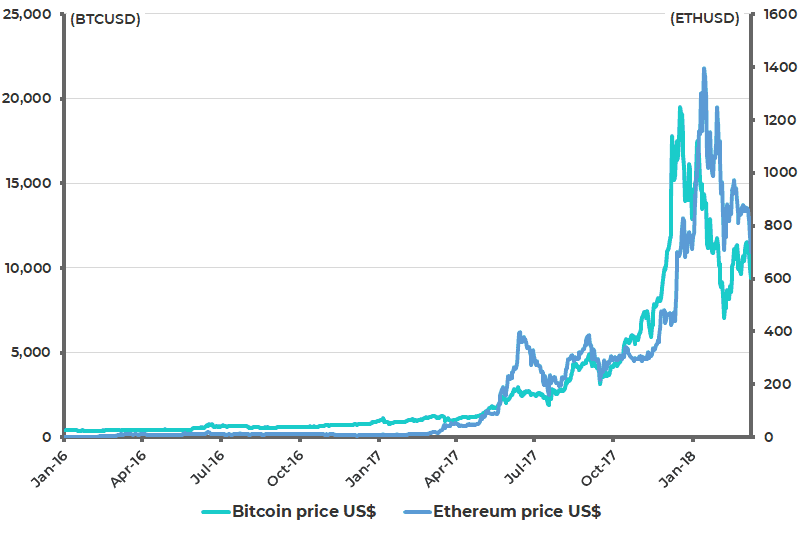

The obvious trigger for such a bust is regulatory intervention. Indeed that intervention has already begun and a sell-off is already under way. This is why Bitcoin price is now US$8,664, down from a peak of US$18,674 in mid-December and Ethereum is now US$663, down from a peak of US$1359 in mid-January (see following chart).

Bitcoin and Ethereum price in US$

Perhaps the most market moving regulatory announcement of late was an announcement by Korean regulators at the start of March threatening to shut down the cryptocurrency exchanges and ban crypto trading. The government has also seemingly banned its own officials from holding and trading cryptocurrencies. This caused a big decline in the price of initial coin offerings (ICOs).

The US Securities and Exchange Commission (SEC) also made an announcement recently. The SEC said in a statement on Wednesday that online platforms trading digital assets that are considered securities need to register with the agency as a national securities exchange. These regulatory moves followed an earlier crackdown in China in September, when the government banned both ICOs and cryptocurrency exchanges.

The other threat to the crypto phenomenon is the growing efforts by governments to tax capital gains made on owning cryptocurrencies. In the US for example, cryptocurrencies are treated by the Internal Revenue Service (IRS) as property for tax purposes rather than as currency. That means profits from cryptocurrency transactions are subject to both the short- and long-term capital gains tax.

Still, if the regulatory reaction has begun, commencement of Bitcoin futures trading also marked the cryptocurrency phenomenon entering the formal financial world. It means that bitcoin can be bought with leverage, which is both a positive and a negative since it means that any future collapse in prices could cause collateral damage in the financial system. It also means that bitcoin can be sold shorted and hedged. This is important since it will have encouraged financial intermediaries to trade bitcoin because they will now be able to hedge the risk.

Meanwhile, it is also important to keep an eye on the ‘big picture’ represented by blockchain technology. In this respect former Federal Reserve chairman Ben Bernanke in a speech at a conference in Toronto in October highlighted the obvious regulatory risk to the cryptocurrency phenomenon. That is that, while conceding that blockchain technology seemingly offers a way to remove the middleman from financial transactions, Bernanke opined that cryptocurrencies would never replace fiat currency because governments would “take whatever action necessary” to ensure that never happens.

Blockchain Will be Co-opted by Governments — Just Like the Internet

This is, unfortunately, a reasonable assumption, which is why the libertarian aspect of cryptocurrencies may be of limited practical import in the real world if only because of its alleged abuse by criminal elements, true or false, which then is used to justify government action.

Just as the internet in China has been co-opted by the mainland government, via the dominance of Alibaba and Tencent, to enable increased social control, the application of blockchain technology, by digitizing assets such as real estate, could accelerate the current attack on cash.

In this sense the early libertarian promoters of the internet proved to be naïve as their cherished invention has turned into an instrument enabling Big Brother while also insidiously undermining the economics of the ‘quality’ media.

Inherently Less Monopolistic Than the Internet

There is a critical difference between the internet and blockchain technology, which should not be ignored. Internet business models clearly encourage ‘winner take all’ business models, which is why Google and Facebook have, at least for now, such a massive share of digital advertising.

But blockchain by its nature, in terms of a distributed ledger, is a much better reflection of a Hayekian view of a free market economy where market outcomes are determined by millions of individuals making their own rational choices rather than dictated by economic planners, of which modern central bankers are one good example.

Nassim Nicholas Taleb referred to this phenomenon in a highly recommended article on Medium as the Hayekian notion of ‘distributed knowledge’. In this sense blockchain technology poses a potential disruptive threat to the monopolist ‘winner take all’ dynamic of modern internet business models which, as discussed last week, should already have triggered antitrust enforcement actions by governments.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.