Bottom Line:

Diversified U.S. cannabis operator Curaleaf Holdings (CNSX: CURA; OTCMKTS: CURLF) today announced the issuance of a new $275 million senior secured term loan facility.

This debt deal should cure any concerns investors have about the company’s cash position.

We estimate management now has about two years of cash runway to either turn a profit or wait for regulations to move in favour of cannabis opening up new pools of capital to the company.

The fact alone that Curaleaf was able to complete such a large deal at better than average terms tells us the market views them as one of the best U.S. cannabis operators.

Curaleaf is now tied with Trulieve as the U.S. multi-state operator with the best chance of becoming a leader in the North American cannabis market.

Owning Trulieve gives you exposure to a solidly profitable company — in four states it generated $282 million of annualized revenue.

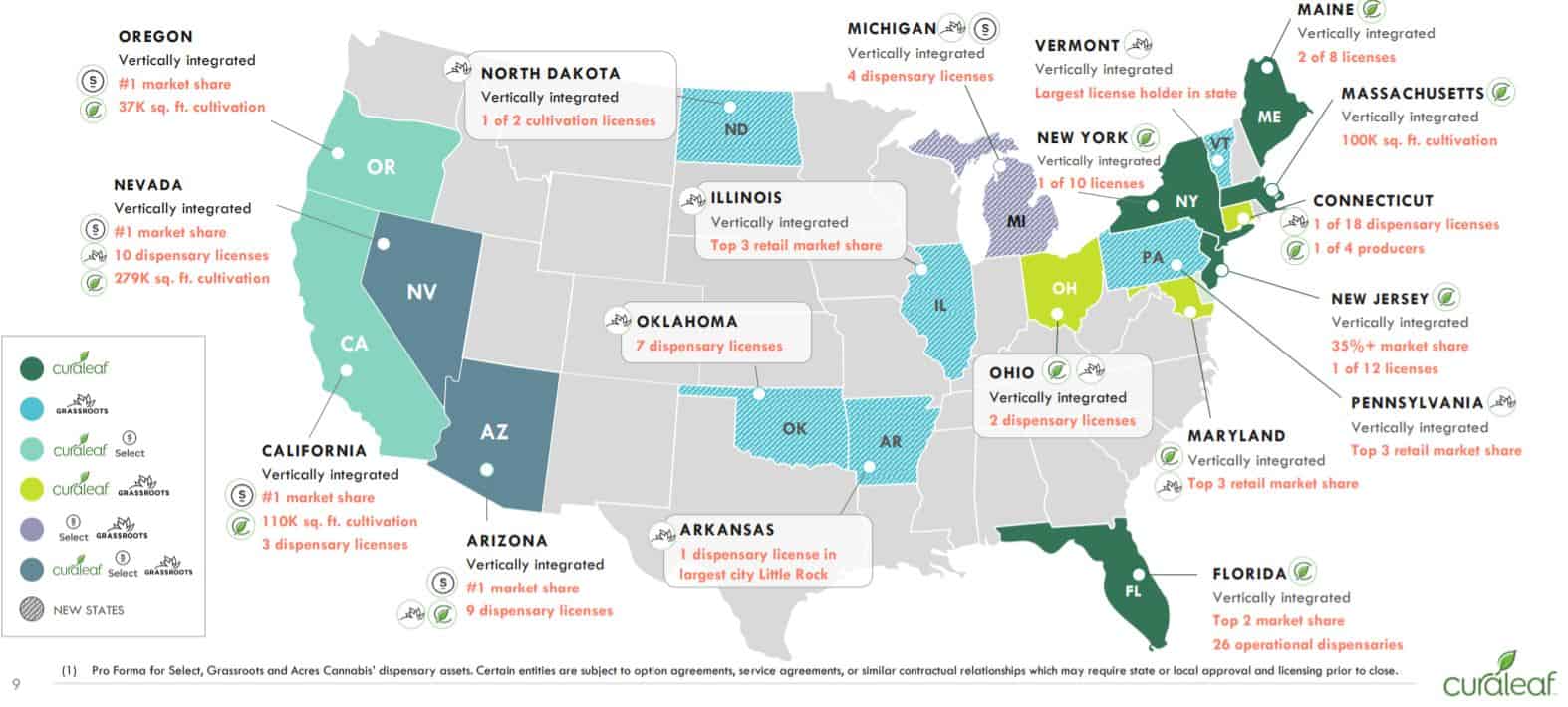

Owning Curaleaf gives you exposure to a company still burning cash, but with a massive footprint in 19 states and annual revenue of $516 million including recently announced acquisitions.

Curaleaf State Footprint is Massive

Both Curaleaf and Trulieve will still thrive while cannabis remains illegal at the federal level.

There is lots of sales growth to go even in medical-only states.

Once the political winds start shifting, as soon as early 2021 in our opinion, U.S. investors will begin to pile into U.S. cannabis plays and these two stocks will capture a solid share of those dollars.

More Details of the $275 Million Debt Deal

The company has lined up a group of sophisticated lenders who have committed to a 4-year bond that pays interest quarterly at 13% annual rate. The loan syndicate includes both existing debt holders and new institutional investors.

Curaleaf plans to use the proceeds to refinance some of its existing debt and to fund its strategic growth projects.

It will also be used to pay transaction fees and expenses related to its recently announced acquisitions.

Regulatory approval for the closing of its two-dispensary buyout of Nevada-based Acres Cannabis was granted yesterday and is scheduled to close Jan. 1.

Deal Terms Better Than Most Cannabis Debt Offerings

The Curaleaf loan offering stands out from recent cannabis debt financing deals due to its more attractive terms.

For one, there is an absence of options or warrants as part of the deal, a common feature in recent debt raises from other multi-state operators.

Not having an equity component built into the offering makes for a lower cost of capital for the company and means it is not giving away additional equity ownership that would have diluted current shareholders.

It also shows that the investors did not need the pot (no pun intended) sweetened with equity incentives and were comfortable with Curaleaf’s financials.

Secondly, while a 13% rate of interest has become standard in the industry, the four-year maturity is very appealing.

The lengthy, broad-based institutional deal shows that the investors are in it for the long haul, believe in the growth prospects of the cannabis industry, and have confidence in Curaleaf’s business model and management team.

Curaleaf Poised to Capitalize on U.S Growth Opportunities

As a vertically integrated multi-state operator (MSO), Curaleaf is well-positioned to become a leader in the emerging U.S. cannabis industry.

Its high-growth facilities are in some of the most populous regions and represent a solid base from which to expand. It presently operates 51 dispensaries, 14 cannabis cultivation sites, and 13 processing sites spread across 12 U.S. states and has licenses or license applications in process to operate in 19 states total.

A strong presence in the medical and adult-use markets should also bode well for the company’s future growth.

Yesterday the company announced that it received regulatory approval to open Cape Cod’s first adult-use retail dispensary which is scheduled to open in the beginning of next year.

Cape Cod is a big summer tourist destination on the East Coast and should put up big sales numbers for the company.

Expanded Balance Sheet Supports Growth Initiatives

Curaleaf has the scale and healthy free cash flow that should enable it to build off its success.

The latest influx of capital affords the company additional liquidity and puts it in an even stronger position to grow.

This should particularly benefit the pending takeovers of Select and Grassroots who will now be supported by a bigger balance sheet.

Shares of Curaleaf are trading 4% higher in late afternoon trading. The deal is subject to the usual closing conditions and is slated for completion on or about Jan. 10.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.