https://www.youtube.com/watch?v=cfqDTFzCkJg

UPDATE: After the release of full quarterly financials, we are much more bullish on the company than we were in the above video.

Multi-State cannabis operator Curaleaf (CNSX: CURA) reported first-quarter 2020 results that disappointed the market.

Revenue of $96.4 million almost exactly met the consensus estimates, however EBITDA of only $9 million missed consensus by over 35%.

Consensus was looking for $14 million of EBITDA but Curaleaf had more than $11 million of one-time charges which meant their actual EBITDA was $9 million, not the “adjusted” $20 million management reported.

The stock has run hard since March, and it was inevitable it would give back some of those gains if results weren’t on the stronger side.

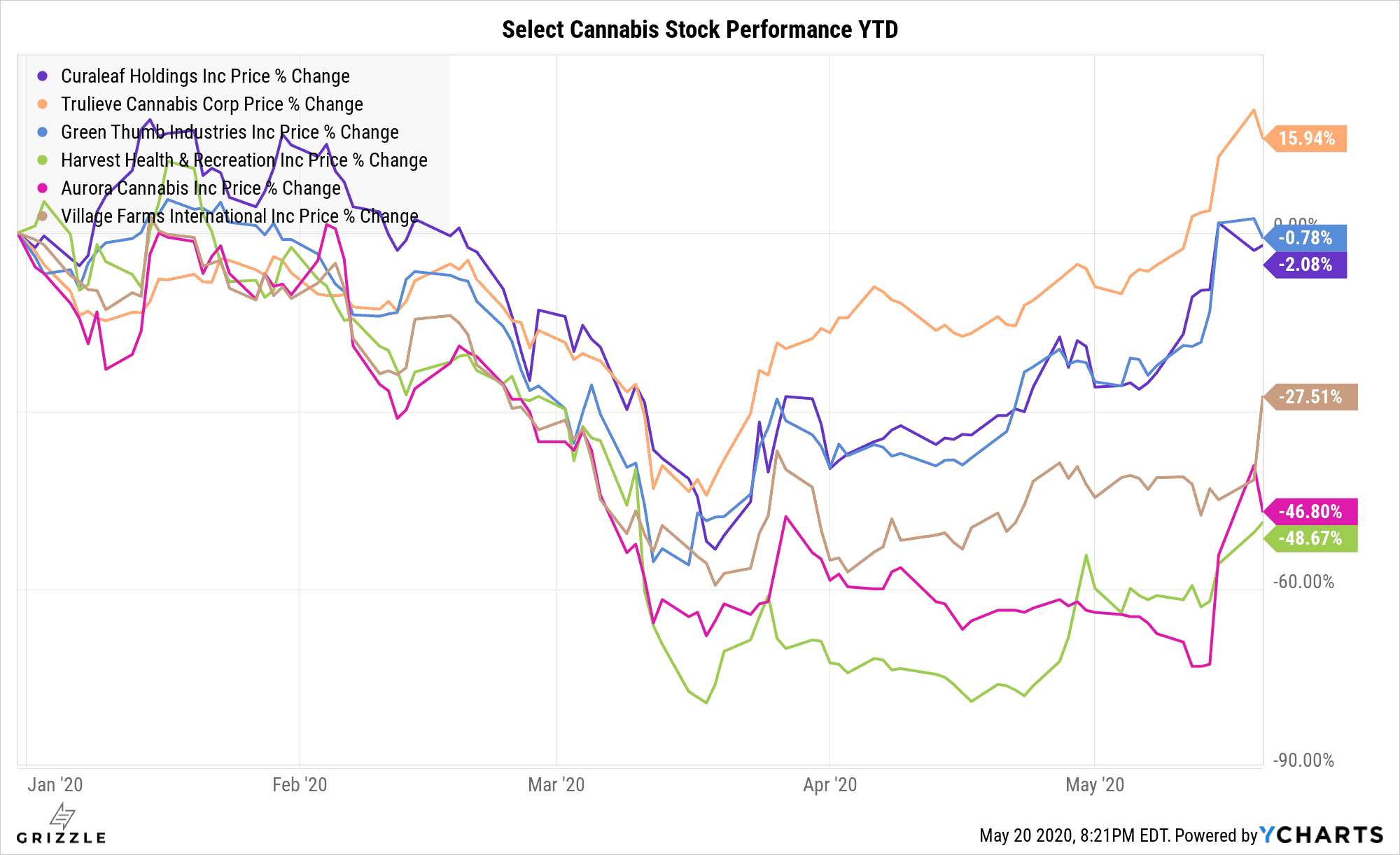

Cannabis Stocks on fire in May

Curaleaf is still taking a page out of the old cannabis playbook that said grow at all costs and figure out the profit later.

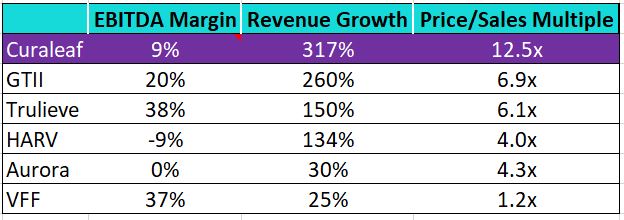

The market approves for now, with the stock trading at the highest multiple of revenue among all U.S. multi-state operators.

Curaleaf has 10-14 months of cash left which is a decent runway, but if they ramp up acquisitions, management will have to issue shares to keep the lights on sooner than later.

[su_panel]For now Curaleaf’s rapid growth and expansive footprint have it tied with Trulieve as our favorite ways to play national legalization of cannabis in the U.S. [/su_panel]CURA Stacks Up Well Against Other Cannabis Co’s

A Capital Raise is Assured: The Question Will be if its Debt or Stock?

Curaleaf was running low on cash in January when it announced a huge debt deal to extend the runway.

The $300 million the company borrowed should keep the cash hopper full through this year, but at the current pace of capital spending, the company will be back to the markets for more cash next year.

They are break-even on cashflow, but have some recent acquisitions to assimilate which will increase the cash burn.

[su_panel]The big question will be if they raise money through more debt or if it comes from new shares of stock. We think its very likely the capital raise is done with stock which will put pressure on the share price when it happens as another US$300 would increase the share count by 10% or so. [/su_panel]The reason we think the company has exhausted their debt capacity is due to the type of debt they’ve borrowed so far.

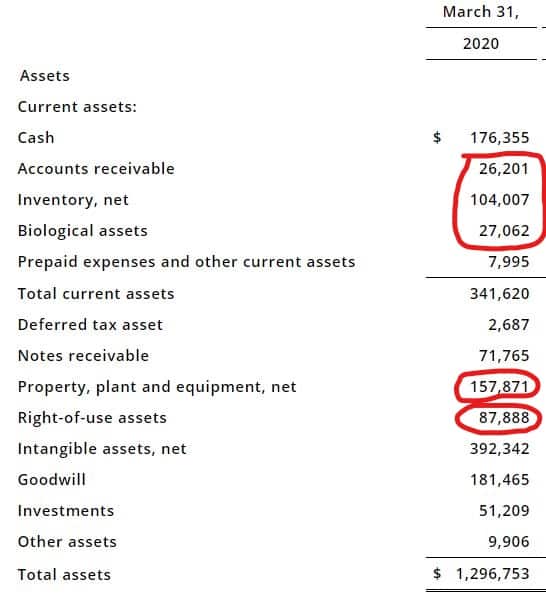

The $300 million of debt was secured, meaning lenders can take all their assets if the company defaults.

Secured lenders typically lend with a minimum of 150% coverage, meaning if hard assets like the buildings, equipment, inventory and receivables are worth $150 million, then Curaleaf could borrow $100 million of secured debt.

Given their hard assets are currently worth $315-$340 million and secured debt is $300 million we don’t think there is any more room to take on more secured debt.

Curaleaf March Balance Sheet

With non-secured “normal” debt out of reach for cannabis companies until federal legalization, share issuance is the only option left.

Curaleaf is in a relatively good position right now, but as we move through 2020, the threat of future stock issuance could cause the stock to underperform.

Curaleaf is already twice as expensive as similar companies, so either a capital raise or pulling back on growth to hit profit targets will negatively impact the multiple and the stock.

This is a company with tons of promise, but also with some important hurdles to navigate in the coming months.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.