Bottom Line

Curaleaf (CNSX: CURA) is set up to outperform in 2019.

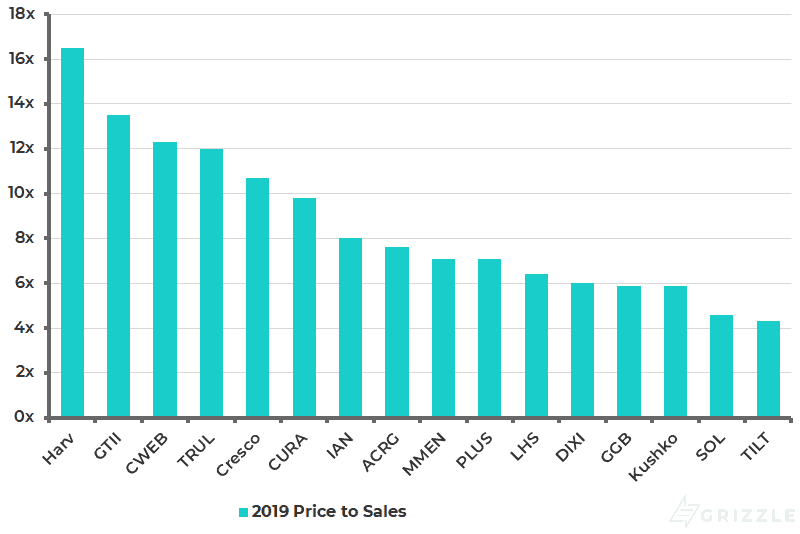

The company will have the second fastest revenue growth among U.S. peers, but only trades at a 15% premium to the group on price to sales.

Management seems confident they will be profitable this year, which will make Curaleaf only the second cannabis company in North America to turn a profit from growing and selling cannabis.

With quarterly revenues of $32 million and 2019 guidance that’s both positive and realistic, Curaleaf appears well positioned to grow its hold on the U.S. cannabis market.

The announced deal to supply 800 CVS stores with CBD, give Curaleaf a huge leg up over peers in regards to brand building and distribution of their products.

With that said, the stock is not cheap, but industry-leading revenue growth makes Curaleaf one of the most attractive U.S. stocks behind only iAnthus.

2019 is shaping up to be a good year for Curaleaf investors.

Cash and Operations Come at a Premium

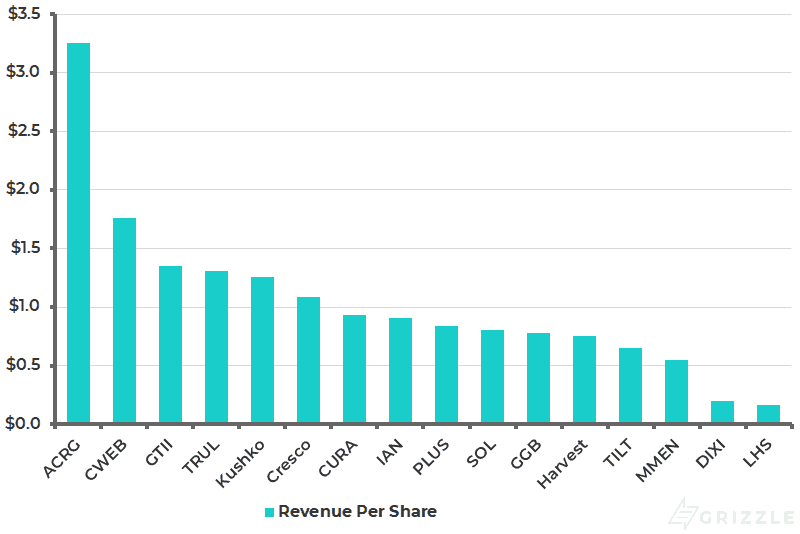

The company posted impressive year-over-year growth in revenues, gross profit and margins, specifically posting revenues per share of $0.19 for the year, a 215% increase from FY 2017. However, their adjusted EBITDA also grew, in the wrong direction, moving from a $1.2 million gain in Q4 2017 to a loss of -$6.2 million in Q4 2018.

While this may seem like a substantial drop in performance, management attributes it to their aggressive expansion strategy, and ultimately when you consider their impressive retail footprint and strong cash position, it’s hard not to feel it may be worth it.

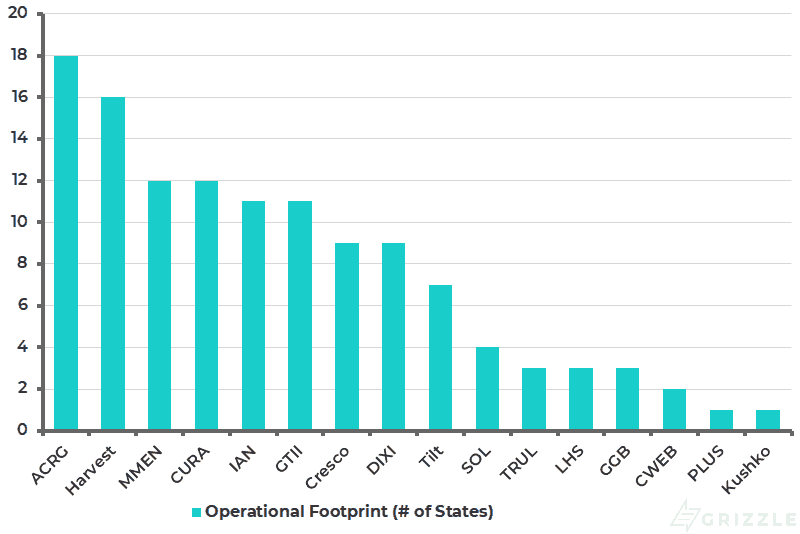

Curaleaf boasts one of the largest operations among U.S. cannabis companies, with an operating presence in 12 states, tied for third with MedMen and only behind Acreage (18) and Harvest (15). As mentioned before, with digital advertising restricted, brand recognition will be built through retail locations. This clearly puts Curaleaf in a strong position.

With a raise completed in Q4 2018, the company is currently sitting on ~$270 million of cash as of December 31st, 2018. While they have recently announced the acquisition of Acres Cannabis for $25 million cash (plus $45 million in Curaleaf shares), they still have enough cash to fund 18 months of operations based on the cash burn rate in 2018. With the company guiding to profitability in 2019, further capital raises seem unlikely.

Additionally, management has agreed on an extension to their voluntary lock-up that will take them until October 2019. This means there shouldn’t be any pressure on the stock price from insider selling.

With all this said, Curaleaf is no bargain and trades on the more expensive side among U.S. cannabis companies on a forward price to sales basis. They clock in at 10x estimated 2019 sales, a 15% premium to the industry average, and good for 6th most expensive among peers.

The Outlook – Curaleaf Set for Aggressive Expansion

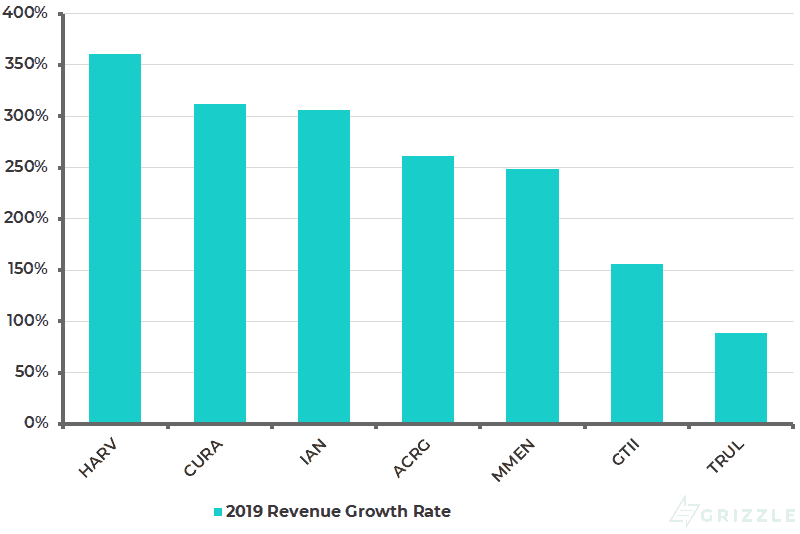

Looking forward, the company’s estimates remain unchanged with 2019 full year managed revenues of $400 million. This would represent an annual increase of over 400% and an increase of over 175% on a run rate revenue basis, no easy feat to achieve. These numbers would make them the highest revenue generator of all U.S. MSO’s with the second highest growth rate (2019 revenue growth over 3rd quarter annualized), according to current estimates. As well, with free cash flow guided to $100 million, it appears as though they might be only the second North American cannabis company to generate positive cash flow.

Overall, the yearly revenue per share would be $0.93, putting them in the middle of the pack as current estimates stand for U.S. cannabis companies. However, investors should understand this is still no small feat, even for cannabis. This is still a developing market with its continued growth hinging on legalization progress and a strong economy, both are factors far outside a company’s control

Aggressive Expansion is the Name of the Game

Throughout Q4 they opened 7 new dispensaries in Florida and Arizona, demonstrating their aggressive approach and suggesting they are interested in capitalizing on the ageing populations in Florida that are expected to create a large demand for medical marijuana.

Furthermore, as recently as March 18th, they acquired Acres Cannabis. While this comes with significant cultivation capacity, it also brings with it one of the most unique dispensaries in the U.S., located in Las Vegas, Nevada. This dispensary is all about the cannabis experience, which is ultimately the direction we see the cannabis retail market heading. This is clearly a smart play from a well-positioned company.

Overall, management has made it clear they plan to continue expanding their footprint in both overall reach and size. While they will face lots of competition, they are proving they what it takes to make the necessary moves.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.