Is this really the top for Big Tech’s leadership of the US stock market, and the related unprecedented relative outperformance of growth over value?

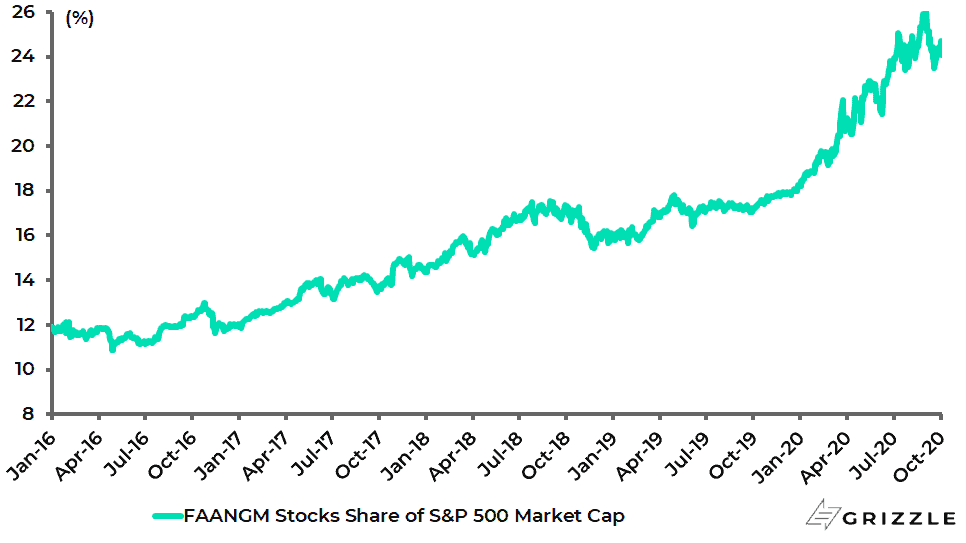

US Big Tech Stocks as % of S&P500 Market Capitalisation

This writer has to admit that if a narrative had to be written of what a peak would look like, recent events certainly fit the bill, be it stock splits by widely followed companies triggering euphoric retail-driven rallies (in this case Apple and Tesla) or the sudden exposure last month of a so-called “Nasdaq whale” (see Financial Times article: “SoftBank unmasked as ‘Nasdaq whale’ that stoked huge tech rally”, 5 September 2020).

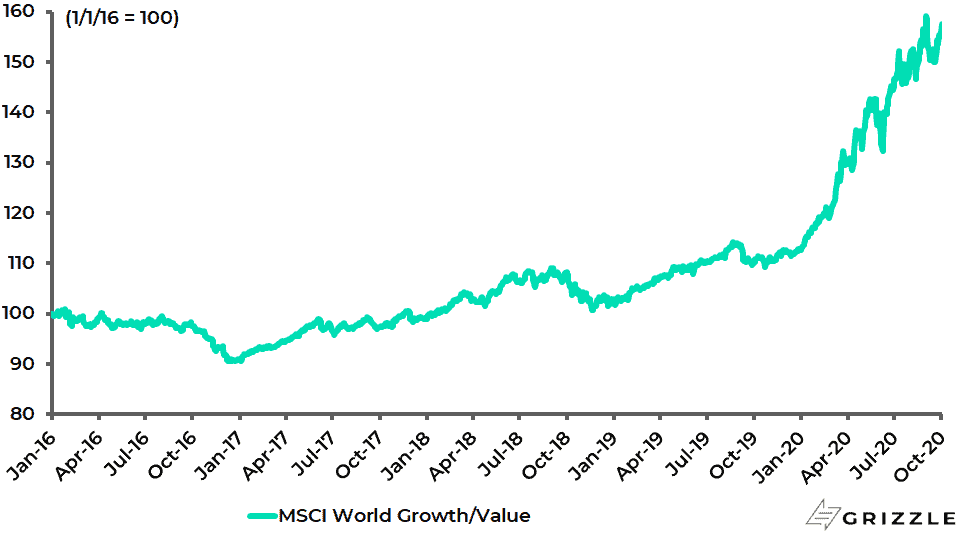

MSCI World Growth Index Relative to Value Index

Still, there is a more mundane explanation for why value could now be expected to enjoy at least an extended period of relative outperformance.

For that is what should happen if cyclical momentum continues to build as the virus continues to prove less virulent than previously feared.

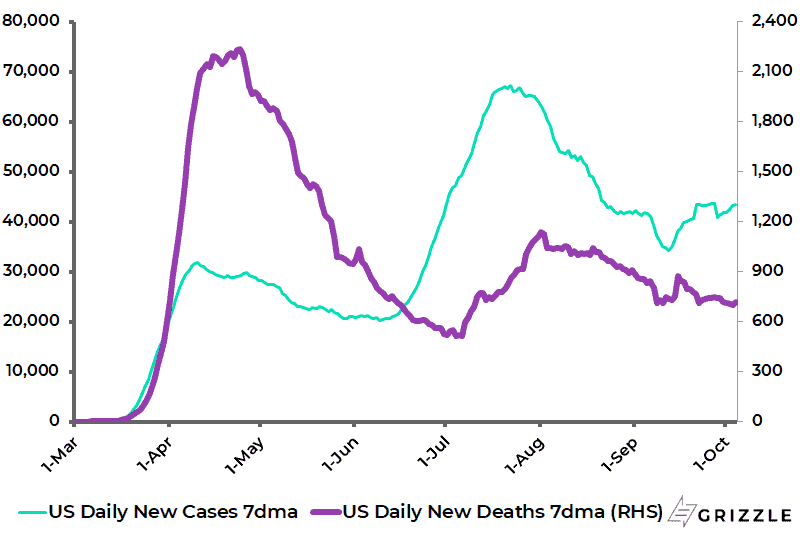

On this point, both daily cases and deaths in America have broadly continued to decline over the past week and are now 35% and 68% below their respective peaks in July and April.

US Covid-19 7-day Average Daily New Cases and Deaths

For if Big Tech’s business models have been massive beneficiaries of the economic lockdowns, as has clearly been the case this year as demonstrated by these companies’ earnings reports as well as their surging share prices, it follows that the same companies will be relative losers if the world goes back to normal sooner rather than later, which is what is still expected to happen here despite renewed second wave fears.

From a longer-term perspective, if it is indeed the case, as also has been argued here, that the policy response to Covid-19 marks the beginning of the end of the deflationary era, that should also benefit value (commodities) over growth.

Still, in the short term, the Federal Reserve’s precipitous return to the zero bound has provided further multiple expansion for Big Tech and related growth companies, while the Fed’s commitment to softer inflation targets and talk of fixing longer-term bond yields, if necessary, has served to reassure investors that interest rates will be lower for longer.

This means that “value” still has the system against it. But at least there is now some light at the end of the tunnel.

A Cyclical Recovery Remains on Track

Meanwhile, it is just as well that Jerome Powell ditched the Phillips curve as a theory at the virtual Jackson Hole conference in late August because otherwise, the August employment data might have been strong enough to cause markets at least to question their extremely dovish expectations.

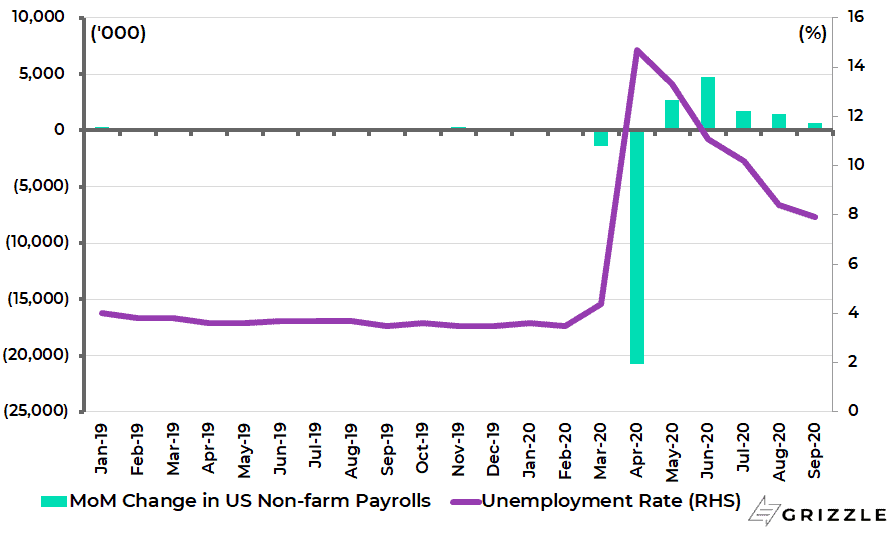

The decline in unemployment from the household survey was much bigger than expected while the headline payroll number was more or less in line.

Total unemployment and the unemployment rate declined by 2.79m and 1.8ppts from 16.34m and 10.2% in July to 13.55m and 8.4% in August, while US non-farm payrolls increased by 1.37m to 140.9m in August.

This compared with the then expected unemployment rate of 9.8% and the expected increase in nonfarm payrolls of 1.35m.

As for the just-released September employment data, the unemployment rate again declined more than expected, though the increase in non-farm payrolls fell short of market expectation.

The unemployment rate declined from 8.4% in August to 7.9% in September, compared with consensus forecast of 8.2%.

While nonfarm payrolls increased by 661,000 in September, compared with market expectations of 859,000. Still, the August figure was revised up to 1.49m.

US Change in Nonfarm Payrolls and Unemployment Rate

The above data serve as a reminder that cyclical recovery remains on track in the US despite the continuing failure to agree on a new fiscal package in Washington.

On this point, the increased unemployment benefit cheques of US$300/week stemming from Donald Trump’s executive order, signed on 8 August, are now paying out with 43 states already distributing the money.

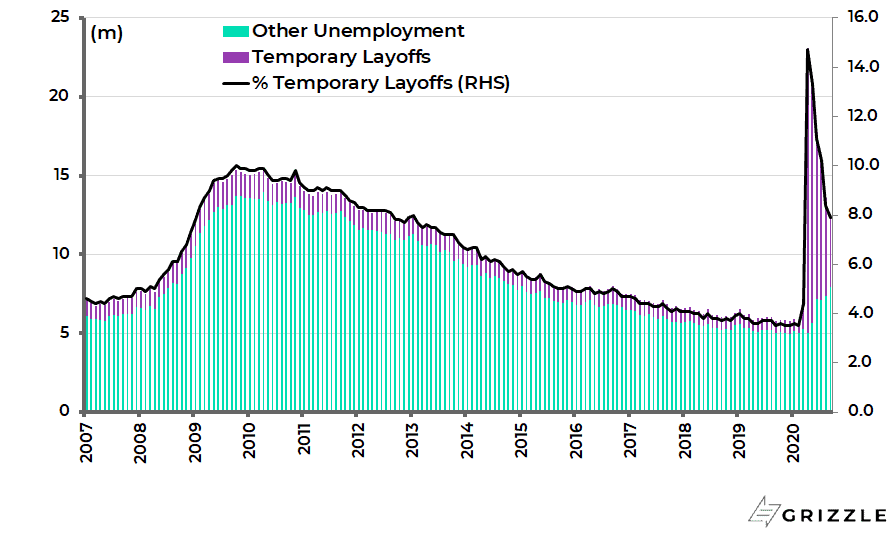

Most of the Temporarily Unemployed Can Still be Rehired

Meanwhile, if it is good news for markets that rising employment data no longer necessarily means a reduction in monetary easing expectations, it is also worth emphasising again that a lot of the temporarily unemployed in America can still be rehired.

Indeed, companies are incentivized to re-hire under the Paycheck Protection Programme (PPP).

On this point, the number of temporary laid-off workers in America declined to 4.64m in September, accounting for 37% of the total unemployed of 12.58m and 2.9% of the labour force, down from a peak of 18.06m in April.

US Unemployment Breakdown

As temporary layoffs decline to the pre-Covid level of 801,000, the unemployment rate will fall to 5.5%.

In this respect, furloughed employees are treated as “unemployed” in America, whereas that is not the case in, for example, Britain.

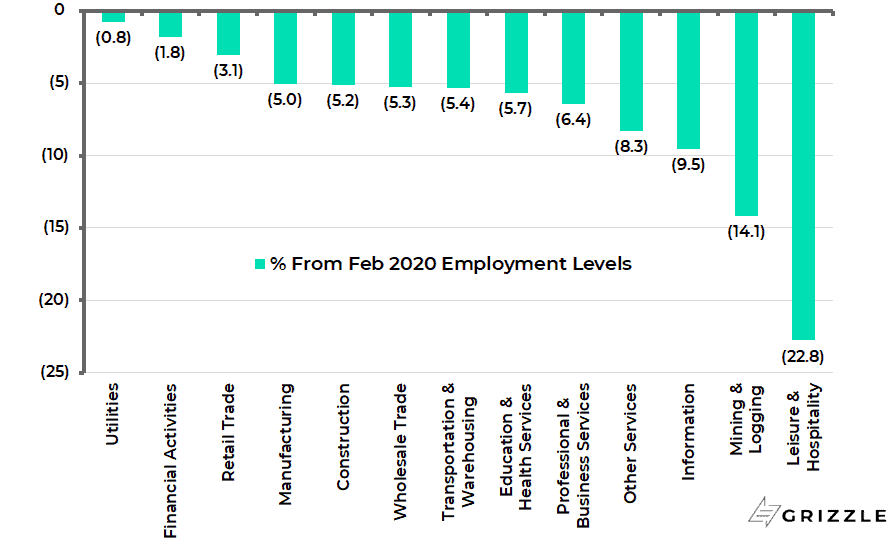

The latest American employment data also highlights the very different experiences workers are having depending on where they are positioned in the economy.

Employment in the construction sector is almost back to pre-Covid levels. But it is a very different story in the hospitality sector.

Thus, employment in the construction sector declined from 7.64m in February to 6.56m in April and has since risen to 7.25m in September or 5.2% below the February level.

By contrast, employment in the leisure and hospitality sector fell from 16.87m in February to 8.55m in April and has since risen to 13.03m in September, or still 22.8% below the February peak.

US Nonfarm Payrolls: % from February 2020 levels

Developed Market Bonds Looking Like Dead Money

Meanwhile, the recent stock market wobbles in the US stock market have not resulted in a bond market rally, which is somewhat surprising.

Still, if yield curve control is coming sooner or later in America and the rest of the G7 world, which this writer still believes to be the case, there is really no point owning G7 government bonds any more save for those players who are forced to for regulatory reasons.

In this respect, a growing number of people are arguing that the traditional 60/40 balanced portfolio between equities and bonds no longer makes sense.

This writer agrees with that point of view in the G7 world, just as the risk-parity approach also no longer makes sense if price controls are coming since Treasury bonds will cease to be a hedge in a falling stock market. Unless, of course, Powell pivots again into negative rates.

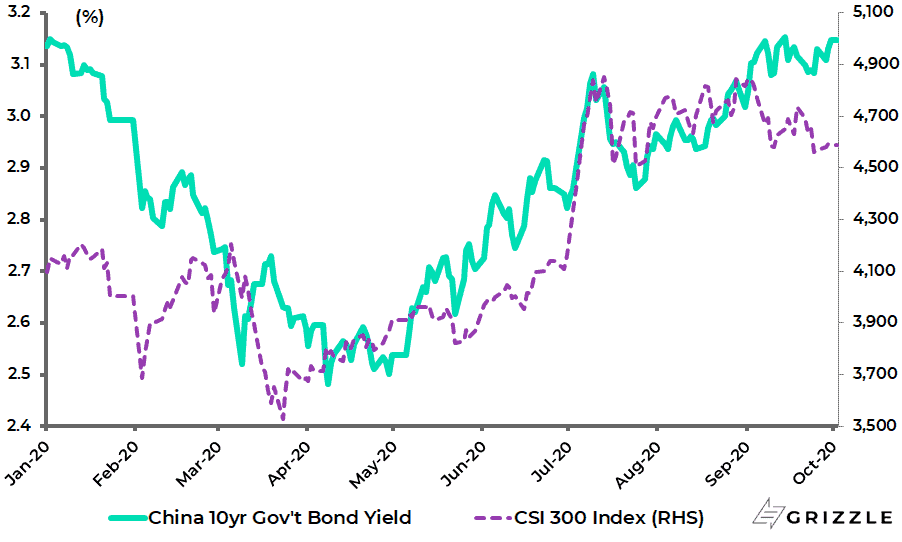

By contrast, China’s capital market provides a much more suitable context for maintaining both the traditional balanced portfolio approach and indeed for running a risk-parity strategy.

For with the ten-year China government bond yielding 3.15%, there is a lot of room to hedge a stock market decline.

China 10-year Government Bond Yield and CSI 300 Index

Or for investors willing to go a little up the risk curve, the ten-year paper of the three China state-owned policy banks currently yield between 3.72-3.86%.

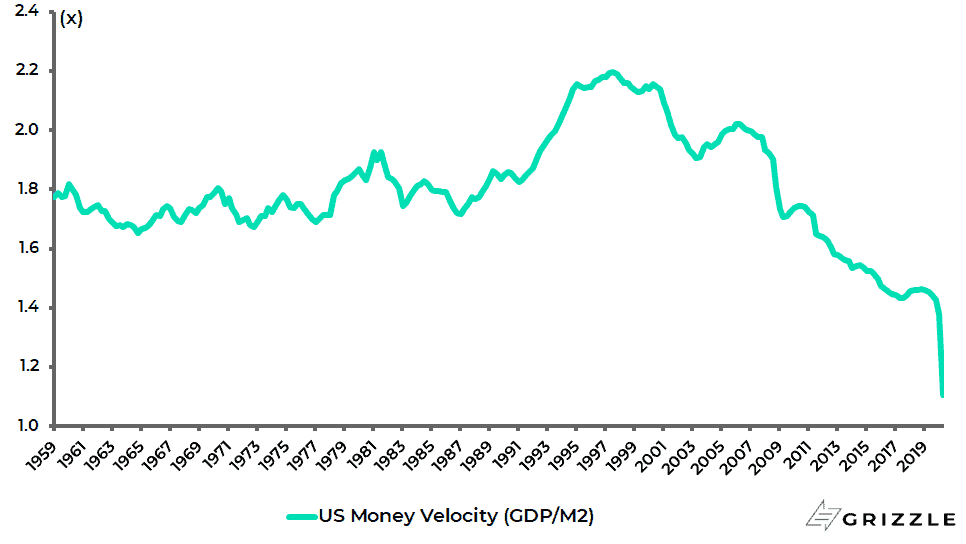

The Deflationary Era is Over

Meanwhile, returning to America and the rest of the G7 world, the “big picture” base case remains that the policy response to the pandemic has set in motion forces that mark the beginning of the end of the deflationary era in place since the early 1980s.

This is despite the further deflationary collapse in velocity that has occurred in 2020 as a consequence of the lockdowns triggered by governments’ responses to the pandemic.

US M2 Velocity

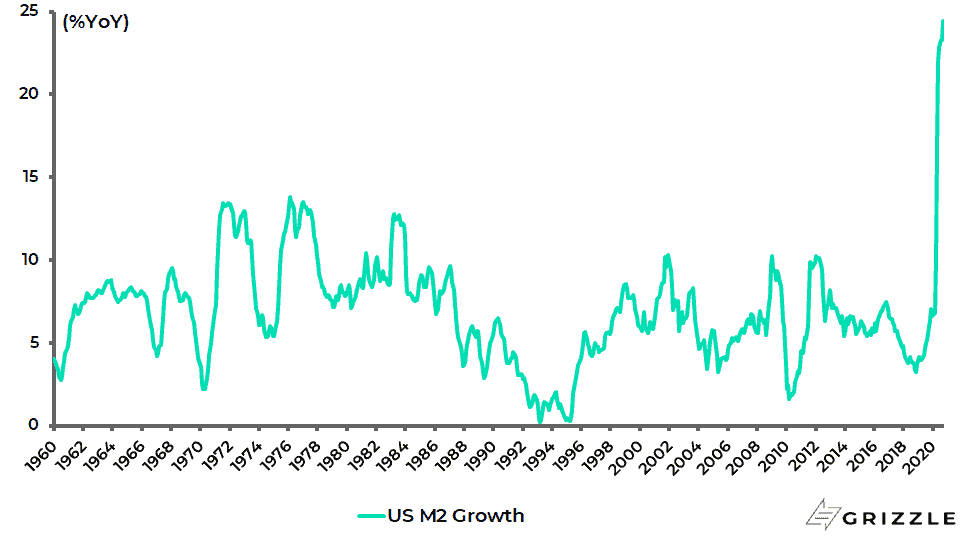

For example, US M2 growth rose to 24.7% YoY in mid-September, the fastest YoY growth rate since the data series began in 1959.

US M2 Growth

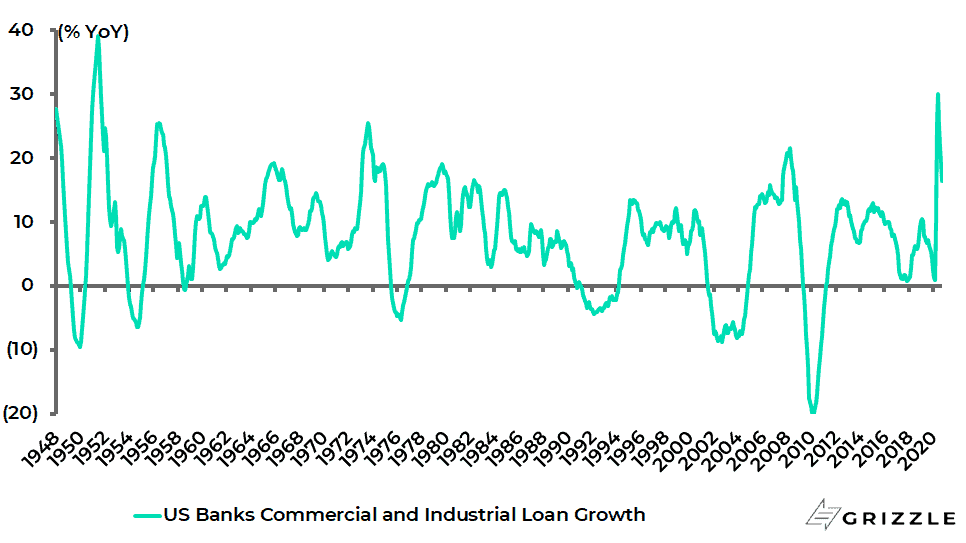

While US banks’ commercial and industrial loan growth surged to 31% YoY in early May, the highest YoY growth since 1951, and was still 16.4% YoY in late September.

US Banks’ Commercial and Industrial Loan Growth

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.