The Walt Disney Company (NYSE:DIS) reported its fiscal Q1 2020 earnings today.

Revenue came in at $20.86B which was in line with analysts’ targets of $20.83B (+0.1% vs estimates)

EPS was $1.53 which beat analysts’ targets of $1.46 (+4.79% vs estimates)

Overall, Disney has performed well throughout the past year, with the stock price increasing around 27% since the same time last year. Most of this terrific performance is due to the excitement around Disney’s video streaming service, Disney+, which is meant to compete with Netflix who is currently widely accepted as the king of video streaming at least for the time being.

All Eyes Are On Stats For Disney+

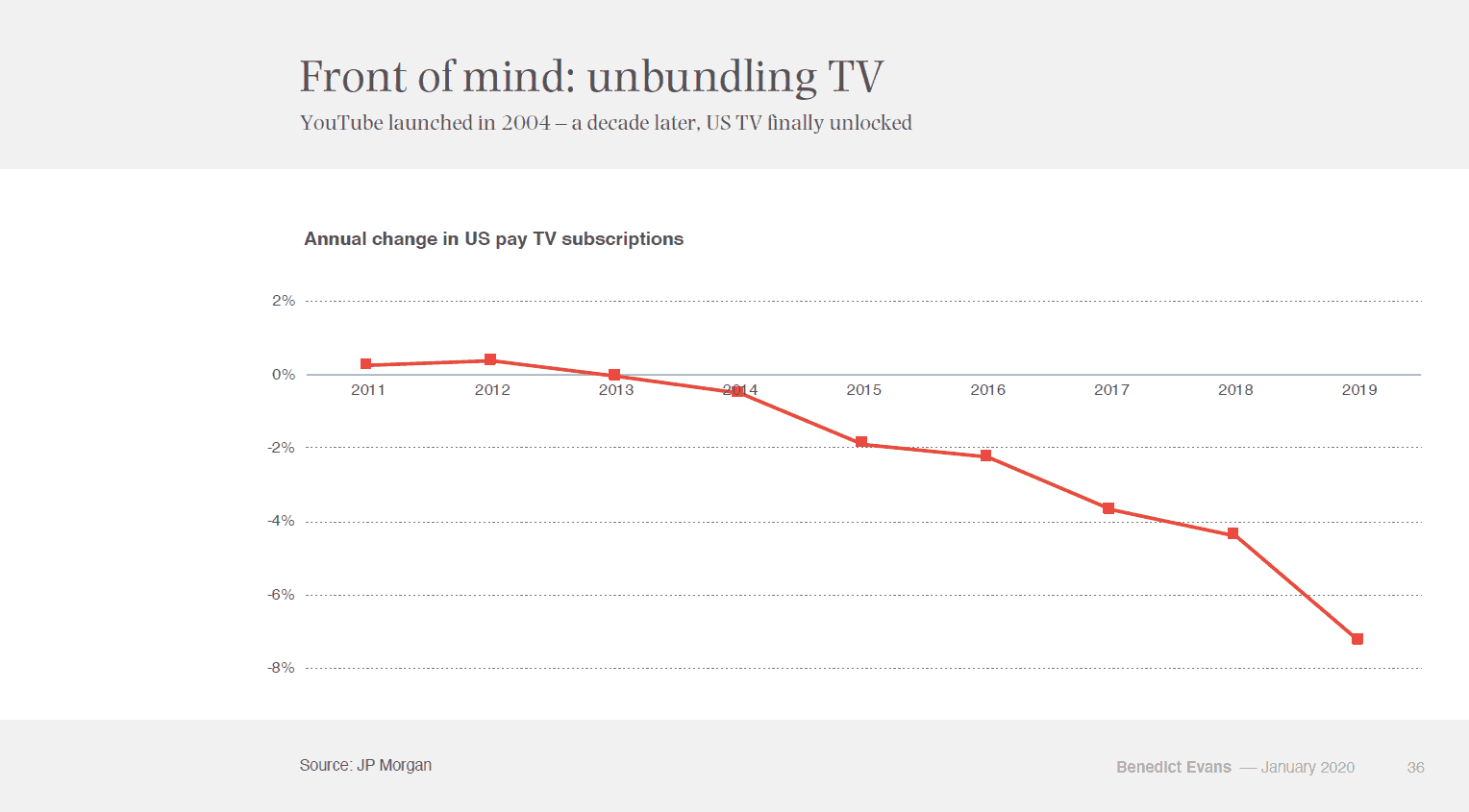

It’s no secret that consumers, especially the younger generation, are transiting away from pay cable TV in an ever-accelerating rate. In the US in 2019, pay TV subscriptions fell by more than 7%.

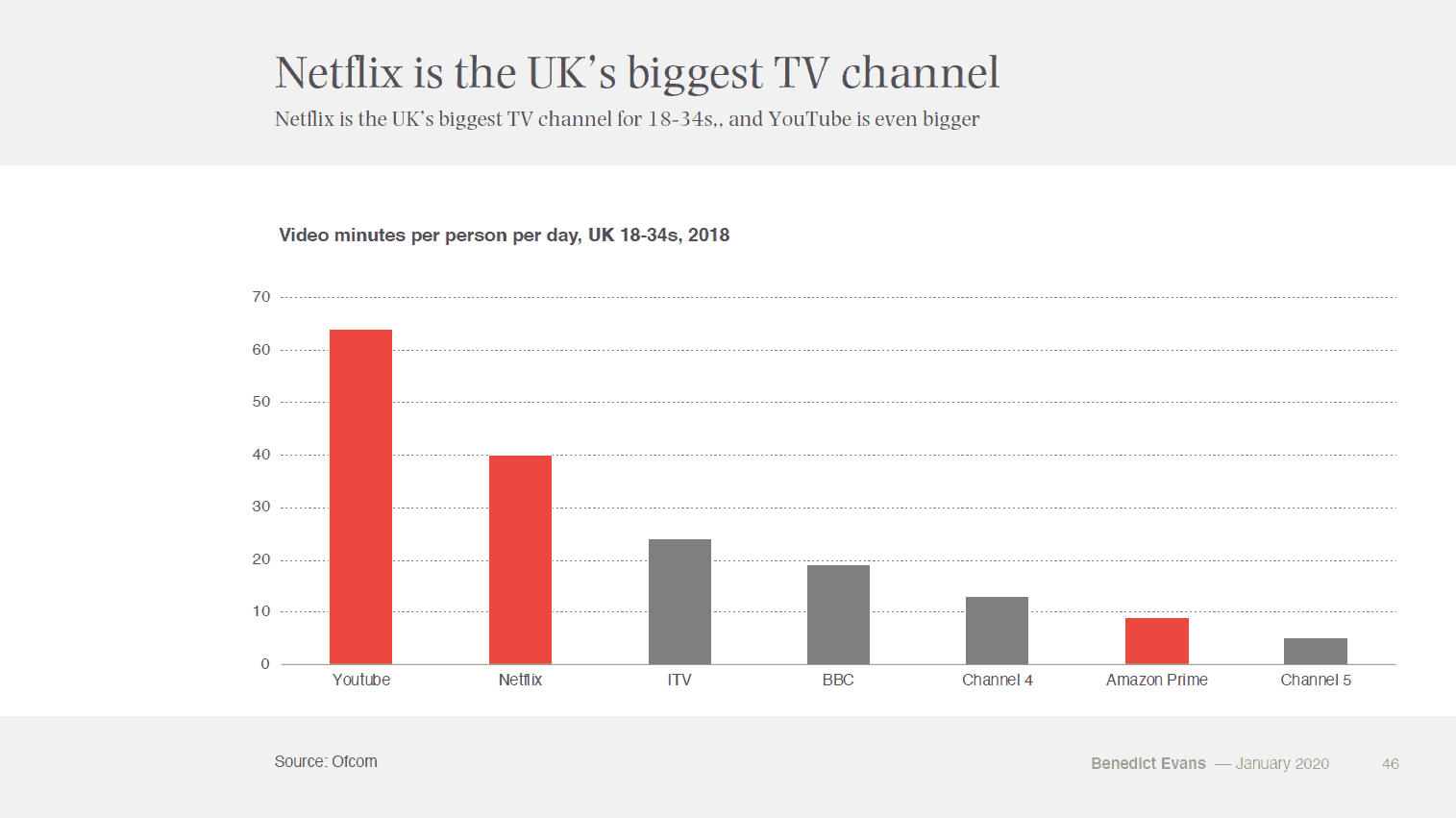

The story is similar overseas. In the UK in 2018, Netfllix beat out all other TV Channels in viewership hours and only lost out to YouTube which typically have much more casual and easier to consume short-form content compared to Netflix.

It is natural then, that Disney wanted a piece of the pie from Netflix. When Disney first announced their Disney+ service, they surprised everyone by pricing the service very aggressively and coming in at $6.99 USD per month, which is $2 a month cheaper than Netflix’s basic plan which only allows the user to stream on one device at a time. Disney+’s $6.99 price point allows for 4 users at once and is the most comparable to Netflix’s premium plan which costs $12.99 per month.

Within one week of its launch, Disney+ acquired over 10 million subscribers. However, this still pales in comparison to Netflix which boasts over 158 million subscribers worldwide. The CEO of Disney, Bob Iger, said right before the launch of Disney+ that the service would be “the most important product that the company has ever launched”.

With this new report for Q1 2020, the company posted an impressive 26.5 million subscribers to Disney+ worldwide. This beat out analysts’ estimates of around 20 million subscribes by a very large margin. This is great news for Disney going forward.

Original Shows Are the Name of The Game

Netflix launched its new original series, The Witcher, back in December 2019 to much fanfare. The show was very well received by the public, and got 76 million views in total within the first week of its launch. Disney+ introduced fans of the Star Wars series to The Mandalorian, a TV show set in the Star Wars universe that quickly became the most popular show in the US after its launch in November 2019, surpassing Netflix’s Stranger Things in view count.

In a dance that’s all too reminiscent of the rivalry between Netflix and Disney, the two companies have continuously tried to one-up each other by spending a massive amount of money producing original shows. The winner may just be the company that can burn enough cash for long enough to sustain making all these originals.

Headwinds From Chinese Coronavirus

Investors in Disney should expect headwinds from the 2019 Novel Coronavirus to continue for Disney as the company has already temporarily shut down its Shanghai Disneyland theme park due to concerns regarding the virus. The closing of Shanghai Disneyland comes at an especially bad time for Disney as it was right around Chinese New Year, which would have otherwise been one of the busiest times for the park.

The virus is also expected to negatively impact theater attendance for the foreseeable future as more people stay home instead of going to the movies. This is horrible news for Disney’s new live action “Mulan” movie which was expected to be very popular in China due to its cultural and historical ties to Chinese legends. Disney also owns 4 cruise ships which are also expected to be hit hard by the news of the coronavirus outbreak. The coronavirus will also have negative impacts for Disney outside of China as more people opt to stay home just out of precaution.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.