Within the Canadian technology landscape, Sylogist Ltd. (CVE: SYZ) is the closest you’re going to get to a “dividend aristocrat”. As of 2019, the company was the only TSX Venture-listed stock to have grown its dividend consistently for the past eight years. Its yield is also significantly higher than the average we typically see across both Canadian and U.S.-listed technology stocks. This makes SYZ a potentially profitable play for income investors.

Summary

- Symbol: SYZ

- Market Cap: $249.8 million

- Annual Revenue Growth: 15.2% (September 2018)

- Free Cash Flow: $11 million

Sylogist: The Business Case

Sylogist is a Calgary-based software company operating at the forefront of intellectual property – an evolving landscape undergoing constant innovation. Sylogist helps customers manage the entire intellectual property lifecycle through a suite of enterprise resource planning (ERP) solutions. This means it serves both public and private sectors.

The company has managed to onboard more than 1,000 customers worldwide, including local and national government departments. Its exposure to the public sector means it has a large addressable market inside government institutions with outdated legacy systems. Some of its most notable private sector clients include Lockheed Martin and Goodyear.

Over the past five years, Sylogist has managed to grow its annual revenue by nearly four times. Free cash flow has remained positive in each of the last ten years, giving investors more reason to be optimistic about future growth. Over the past five years, income has grown at a compound annual growth rate of more than 25%.

Dividend Star

An analysis of Sylogist wouldn’t be complete without documenting its impressive dividend yield. SYZ stock currently yields 3.11%, which is far and above the technology-sector average. The company has increased its payouts in each of the past eight years, an impressive feat given its micro-cap status. A strong buyback program combined with high free cash flow suggests dividends are likely to continue growing for quite some time.

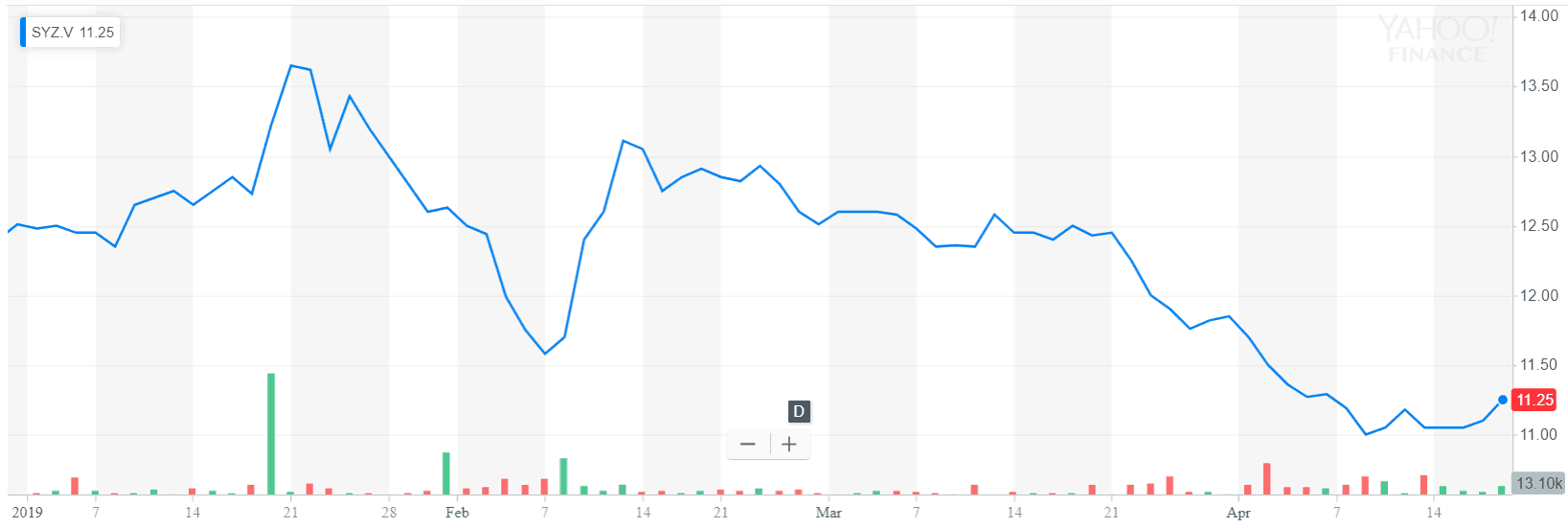

In terms of share price, SYZ has been mired in a year-long slump following the release of disappointing earnings. In its most recent quarter, Sylogist reported earnings and revenue that missed analysts’ expectations. However, that followed a massive uptrend in 2018 marked by impressive revenue and profitability, including an 84% gain in per-share earnings. When last year’s performance is taken into account, it’s easy to conclude that SYZ is probably oversold.

Since peaking in early November, SYZ is down 20%. Year-to-date, the stock is down just over 12%.

Conclusion

Income investors have plenty to be excited about when it comes to Sylogist. A large addressable market and strong value metrics suggest Sylogist will be a major dividend player for years to come. At roughly $11, SYZ stock is trading well below its peak.

Disclaimer: The author has no investment position in Sylogist Ltd. at the time of writing.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.