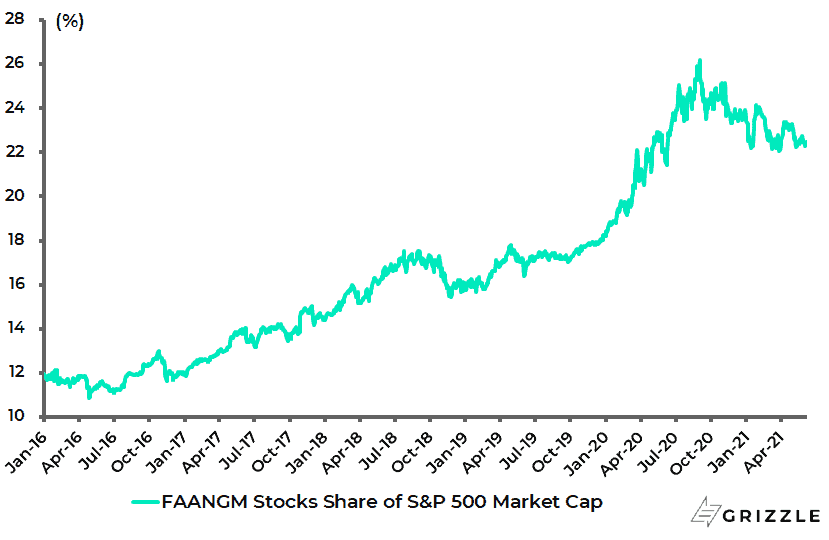

It is interesting that FAANG stocks still look like they have peaked out against the S&P500 despite the fantastic earnings reported by these companies last quarter, geared as they have been to the world of virtual working.

In a funny kind of way, the better the numbers these companies report the more it is a sign of their control of the marketplace from an anti-trust and other regulatory standpoints.

Action on the anti-trust front is surely coming sooner or later, just as it has already arrived in China.

US Big Tech’s share of S&P500 market cap

On top of this, there is the obvious risk of the law of large numbers as regards maintaining such growth rates.

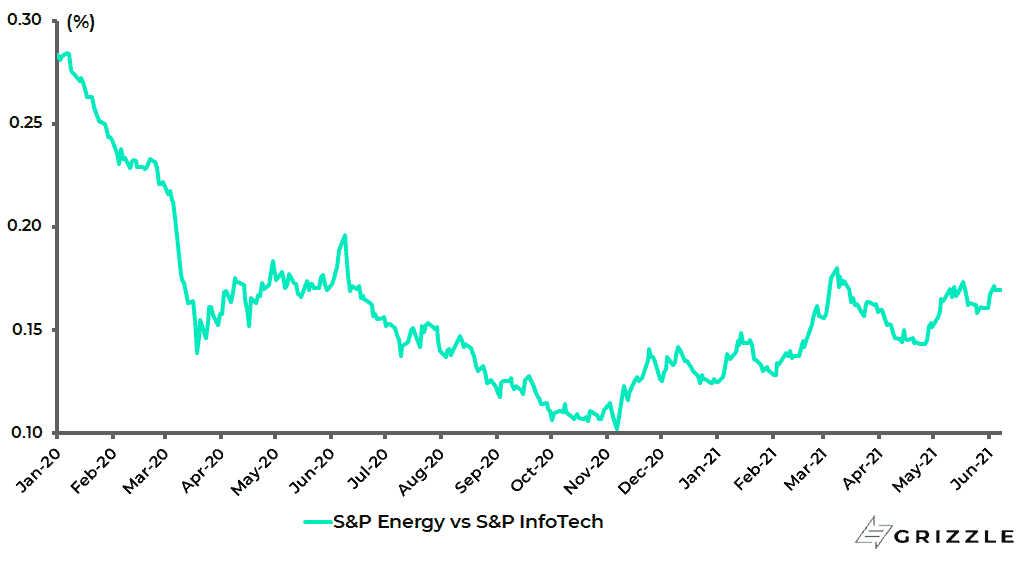

Meanwhile, this writer continues to prefer cyclical stocks with the obvious pair trade, in the context of the now commenced inflation scare, that of being long energy and short tech.

S&P500 Energy relative to S&P500 InfoTech Index

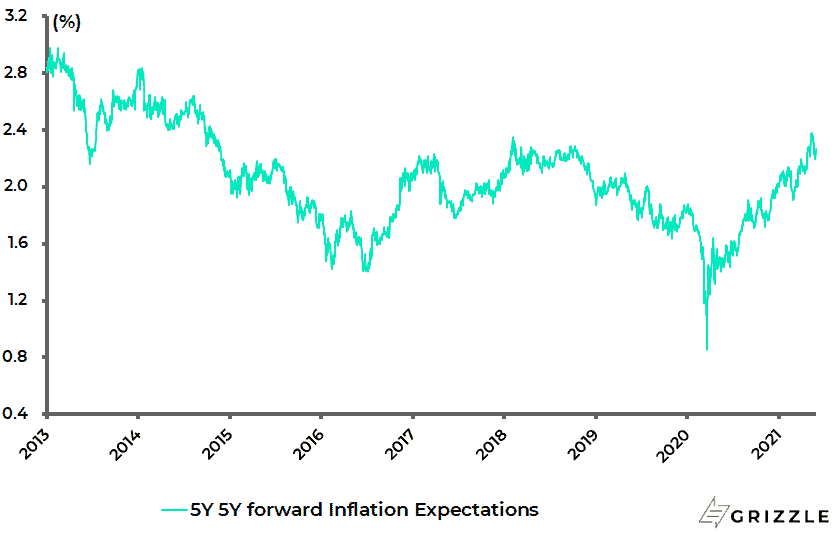

With a long-term deflationary view maintained for many years, this writer has been in a somewhat weird position during the past year and more of arguing that a change in investment regime, from a deflationary era to an inflationary one, could be forthcoming.

This remains the base case though, as also discussed here previously, the outcome will ultimately depend on how the Federal Reserve and other G7 central banks respond when it becomes clear they have underestimated the inflationary pressures coming out of the pandemic.

For such a surge in inflation expectations will be the trigger for the markets to stress test the Fed’s metal.

The US 5-year 5-year forward inflation expectation rate is now 2.26%.

US 5-year 5-year forward inflation expectation rate

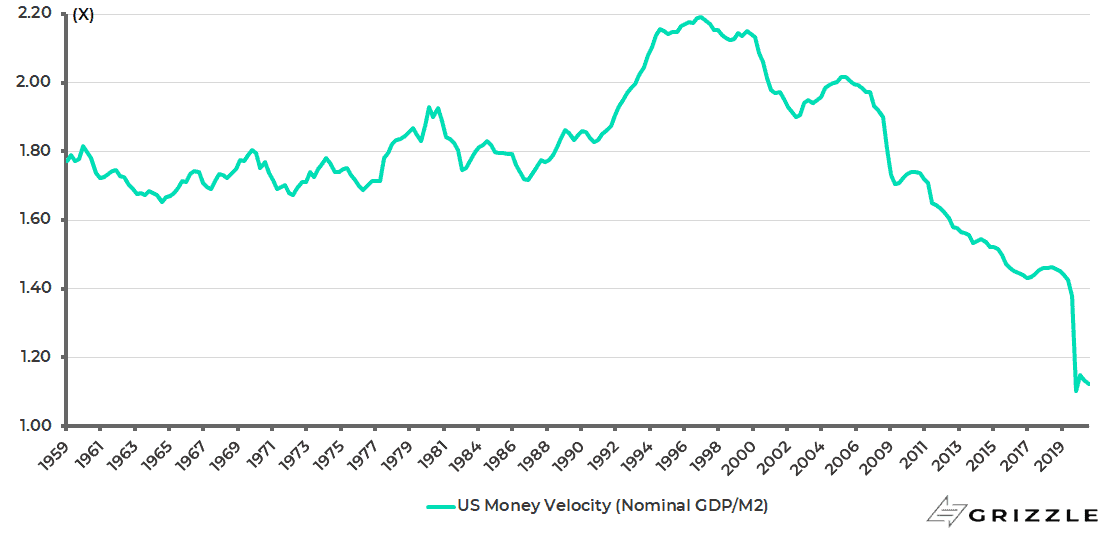

Still, having said all of the above, it is worth asking the rhetorical question of how this view could be wrong, and how the deflationary regime could be maintained despite the frenzy of monetary and fiscal stimulus witnessed in the G7 world over the past year and more.

The obvious technical ‘big picture’ answer is if velocity keeps trending down despite the massive expansion in broad money supply seen over the past year.

US M2 velocity declined from 1.463 in 4Q18 to 1.103 in 2Q20.

It then rose to 1.148x in 3Q20 as the economy rebounded, though it has since fallen again to 1.122 in 1Q21.

US M2 velocity (Nominal GDP/M2)

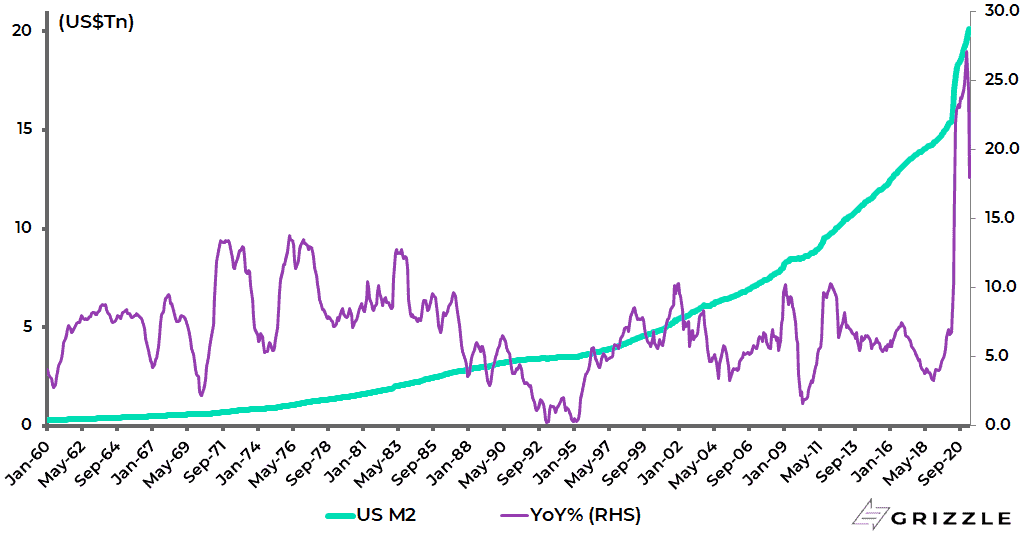

As for broad money supply, US M2 growth accelerated from 6.8% YoY in February 2020 to 27.1% YoY in February 2021, the fastest pace since the data series began in 1960, and was 18% YoY in April.

As a consequence, US M2 has risen by US$4.6tn or 30% from the pre-Covid level in February 2020 to US$20.1tn in April 2021.

US M2 Growth

This question is worth raising since the most recent set of US quarterly bank earnings results has provided a reminder of the longstanding deflationary backdrop.

This is because there is no sign as yet of a pickup in the credit multiplier in America.

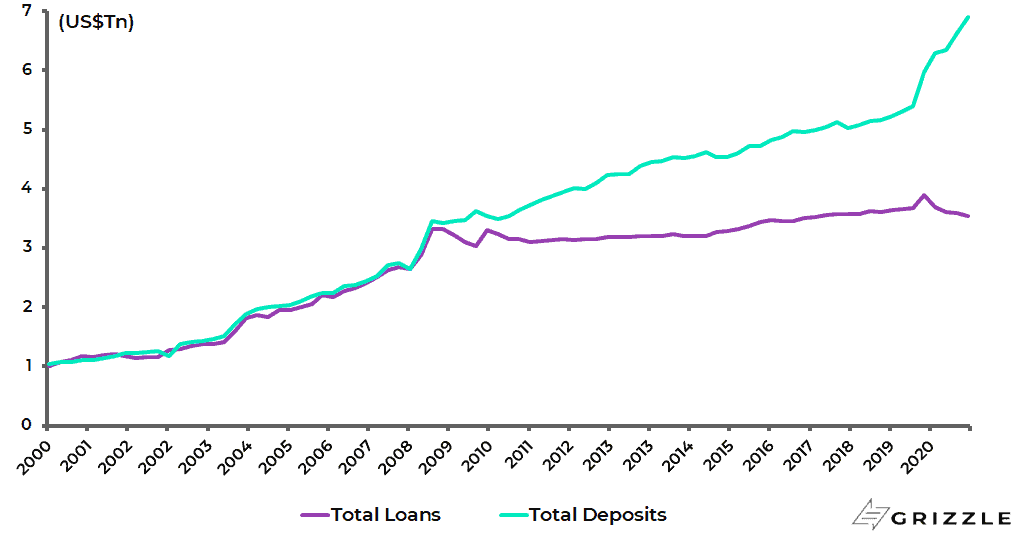

The four major US banks’ total loans declined by 9% YoY at the end of 1Q21 and are down 3.6% since the end of 2019; even though there was a 9.8% YoY increase in assets driven primarily by an increase in securities held by these four banks, namely JPMorgan, Bank of America, Citigroup and Wells Fargo.

Yet if loan growth has not picked up, bank deposits have continued to surge as a result, in large part, of the increase in transfer payments or handouts.

The four major banks’ total deposits rose by 15.4% YoY in 1Q21 and are up 28% since the end of 2019.

US Four Major Banks’ Total Loans and Deposits

The Fed’s flow of funds data shows that the increase in household deposits in 2020 accounted for 52% of the increase in total deposits.

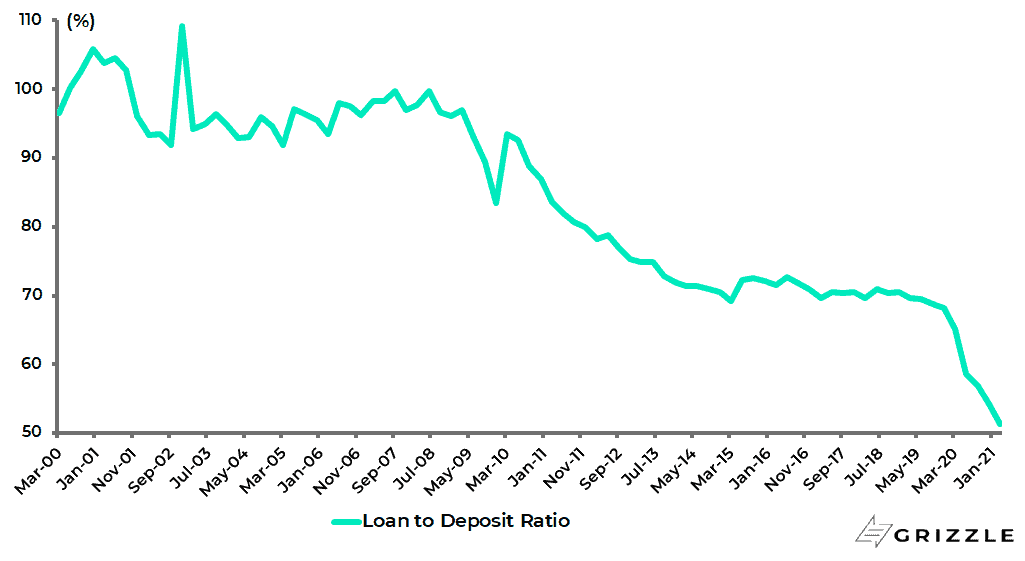

The result is that the loan-to-deposit ratio of the four major banks has fallen to 51% in 1Q21, down from 68% in 4Q19.

US Four Major Banks’ Loan-to-deposit Ratio

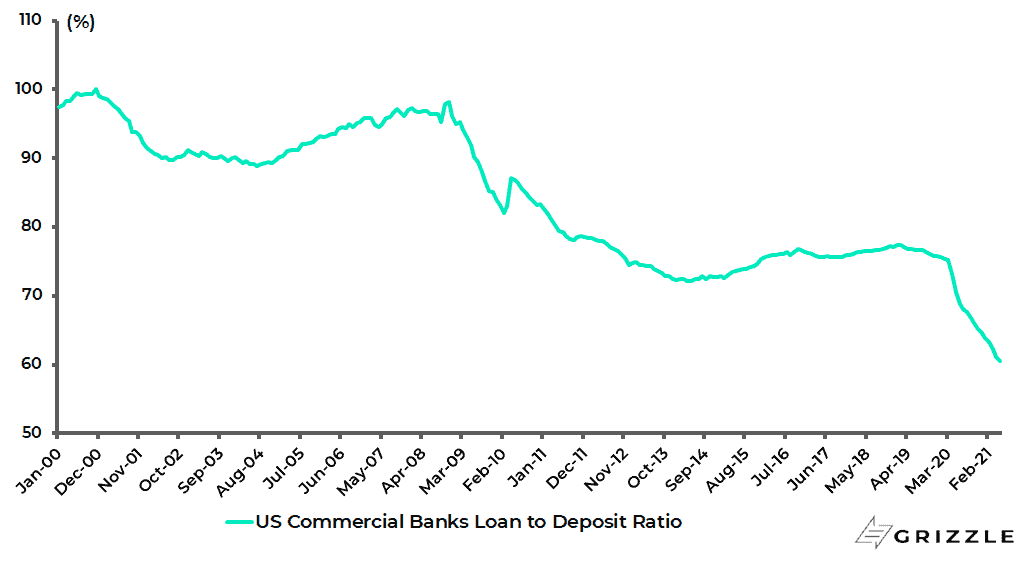

While the loan-to-deposit ratio of the whole US banking system has declined to 60.6% in the week ended 26 May, the lowest level since this data series began in 1973.

US commercial banks’ loan-to-deposit ratio

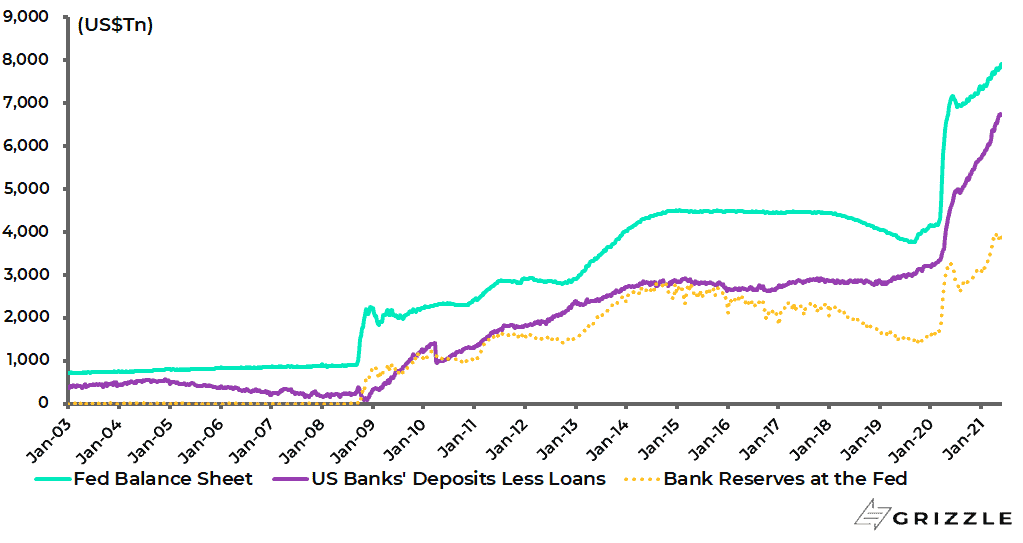

Meanwhile, the flip side of the Fed’s quanto easing efforts continues to be a pickup in banks’ excess reserves held at the Fed, as has been more or less the case since the launch of quantitative easing back in late 2008.

The Fed’s balance sheet has risen by US$3.76tn since the start of 2020, while US commercial banks’ excess deposits over loans have increased by US$3.55tn over the same period and their reserves at the Fed are up US$2.3tn.

US banks’ deposits less loans, bank reserves at the Fed and Fed balance sheet

Similarly, the Fed’s balance sheet has increased by US$7.03tn since September 2008, while US banks’ excess deposits over loans are up US$6.46tn and bank reserves up US$3.84tn over the same period.

Clearly, if the above dynamic is maintained, then this writer’s view of a change in investment regime will prove to be wrong.

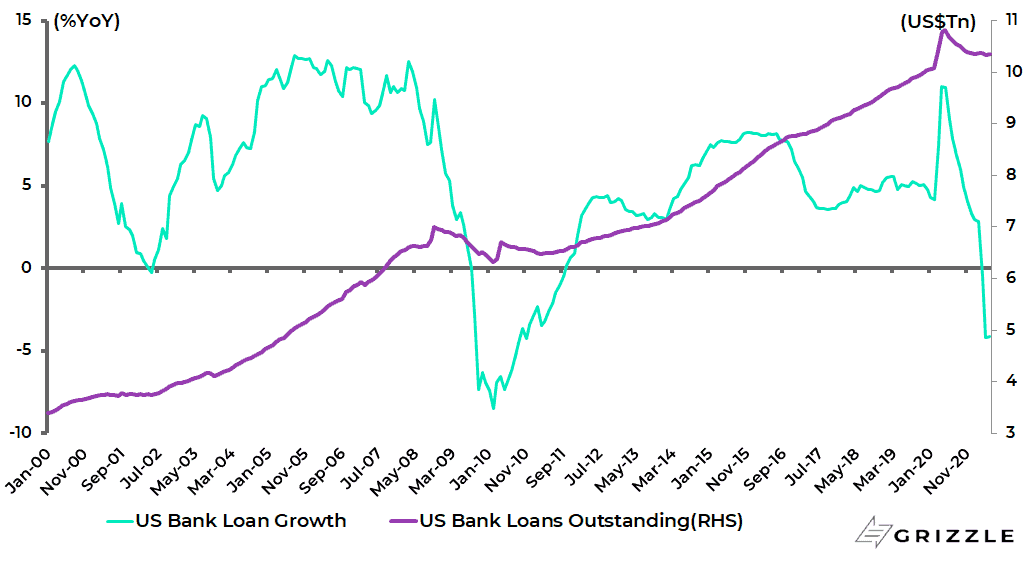

For now, from a more historical perspective, it remains the case that the four major US banks’ outstanding loans are running at levels only marginally above the level seen prior to the global financial crisis. The four major banks’ outstanding loans are up only 7% over the past 12 years since 1Q09, while their total deposits have doubled over the same period.

Indeed overall system loan growth only turned positive from 2011 and then never accelerated thereafter above the levels seen prior to the global financial crisis.

US commercial banks’ total loans have risen by an annualised 4.8% since bottoming in March 2011, compared with an average growth of 11% YoY between 2005-2008.

US commercial banks’ loan growth and loans outstanding

The above sluggish growth has been in part the consequence of the post-2008 tightening of regulations on banks’ ability to lend, in terms of tougher Basel-related capital ratios and the like, which had the perverse effect of working against the Fed’s own efforts to reflate via zero interest rates and quanto easing.

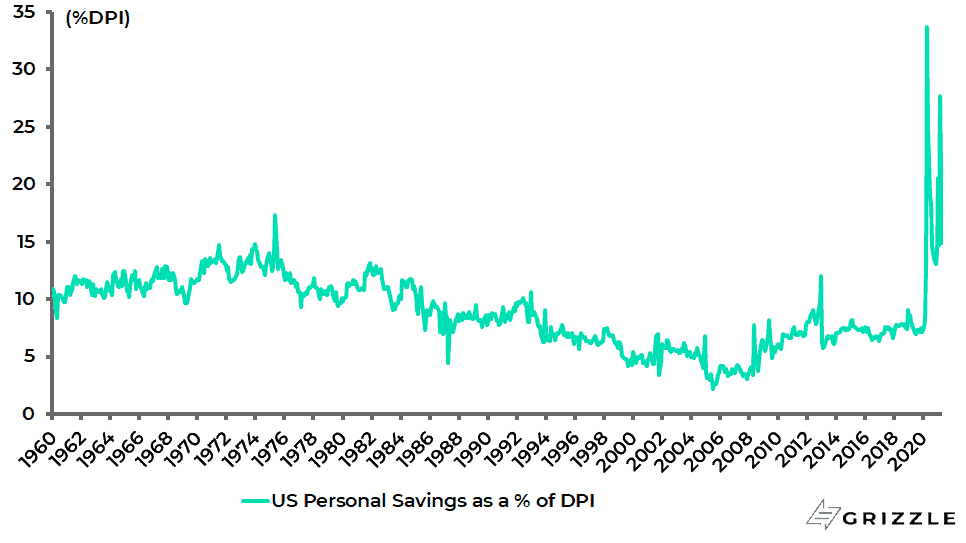

It is also the case that, in a related development, the post-2008 era saw a continuing deleveraging impulse after the housing market shock as US households increased their savings rate from 3.1% of disposable income in November 2007 to 7.5% in 2019 in a process which could be described as balance sheet repair.

US Personal Savings Rate

Still, it is too early to conclude that the animal spirits will never re-ignite.

The bank results were for the first quarter when lockdowns were still in force.

As the American economy becomes ever more normal in terms of the end of lockdown-related restrictions and as the yield curve continues to steepen, assuming that happens, the incentives will increase for banks to expand lending since banks make money by borrowing short and lending long.

And based on conventional monetary policy theory, growth in loans should create a self-feeding growth in deposits.

There is also a political context to the above. If bank loan growth continues to disappoint, the political pressure will likely grow for banks to be made to lend.

This could well take the form of a continuation or expansion of various forms of loan guarantee programmes.

There is also the potential for a relaxation in capital ratio restraints if lending is considered to be going into politically acceptable areas such as, for example, funding “green” projects.

In this respect, the political agenda of the Biden administration could turn out to be as relevant as the technical aspects of monetary policy.

For example, moratoria on loans are at present still applied to student loans and federally guaranteed mortgage loans in America but not to auto loans. These moratoria are meant to end at the end of September and June respectively. But will that really happen?

The expansion of such interventionist policies could set up a very different dynamic as would, without doubt, a decision by the Federal Reserve to sever the link formally between interest rates and inflation by imposing some form of yield curve control, thereby committing the Fed to potentially unlimited balance sheet expansion.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.