It is always easy to come up with ex post facto rationalizations of market action.

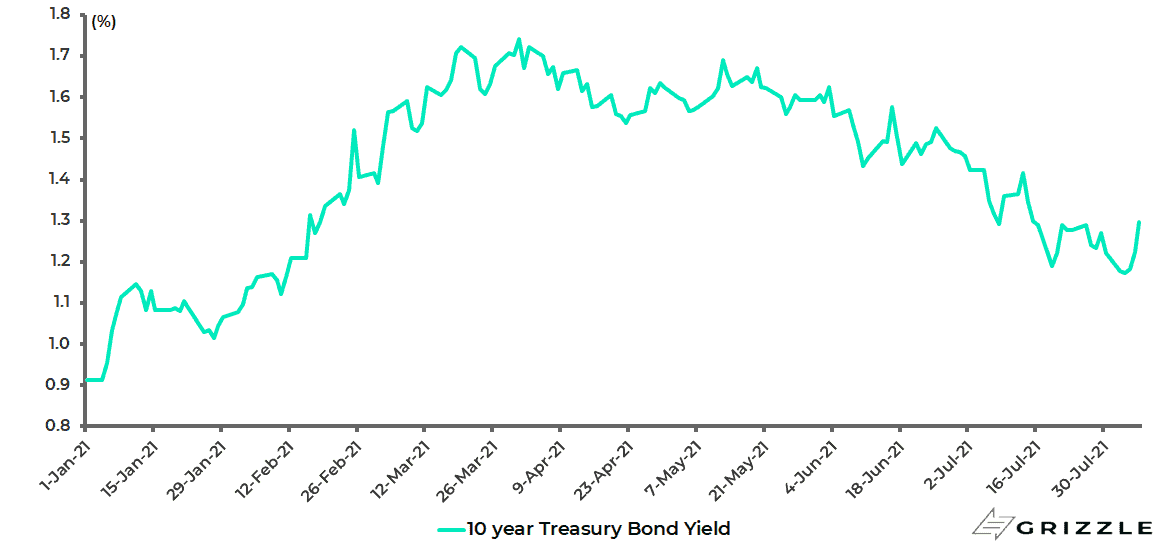

But this writer has to admit to being somewhat mystified by the scale of the US bond market rally which has seen the 10-year Treasury bond yield decline from 1.77% in late March to a bottom of 1.13% on 4 August before rising to 1.30% on Friday.

US 10-year Treasury bond yield

Initially, it was easy to rationalise the bond market action as driven by positioning and an assumed peaking out of the base effect in terms of the inflation data.

Still, this has become harder to do even allowing for illiquid markets during the summer holiday season, which has now commenced, and momentum-driven algo trading.

Indeed the Treasury bond market has of late been signalling a full-on growth scare, a concern which cyclical equities have also began to reflect.

It is also the case that expectations of the first Fed rate hike have been pushed back.

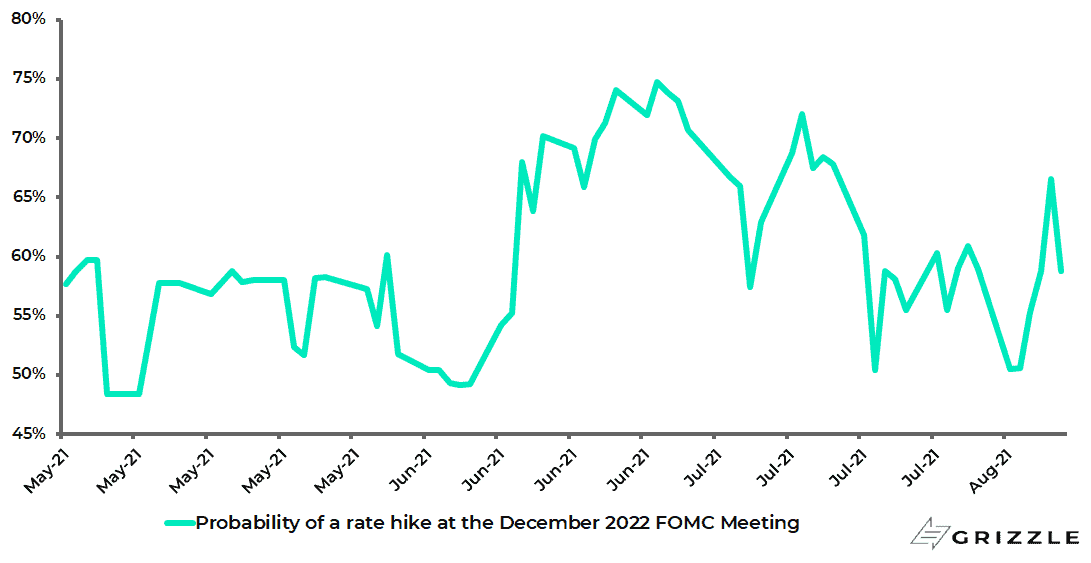

The futures market’s implied probability of a Fed rate hike by the end of 2022 has declined from 75% in late June to 59%, according to the CME Group.

Probability of a Fed rate hike at the FOMC meeting in December 2022

All this surprises this writer because, while it has been evident for some time that US cyclical momentum peaked last quarter, there is a complete lack of evidence that growth is collapsing.

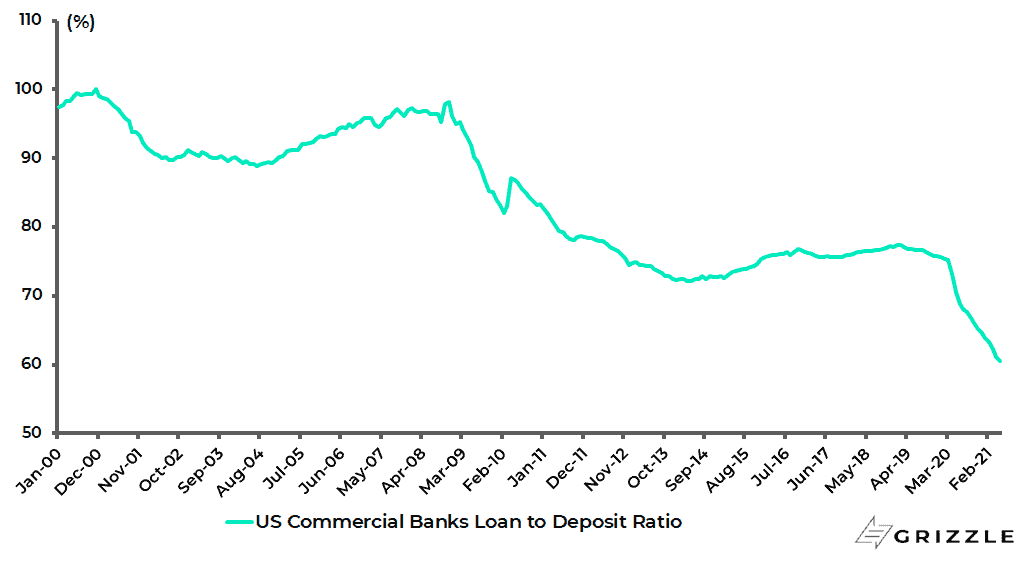

True, the loan-to-deposit ratio of the American commercial banking system running at an all-time low which certainly does not support the return of inflation story.

But that reflects more the surge in household deposits courtesy of transfer payments rather than a complete absence of loan growth.

US commercial banks’ loan-to-deposit ratio

Source: Federal Reserve

While in those Republican-governed states which opened first, such as Florida and Texas, loan growth in the first quarter was running well ahead of the national average.

This could turn out to be a meaningful lead indicator, though second-quarter data is not yet available.

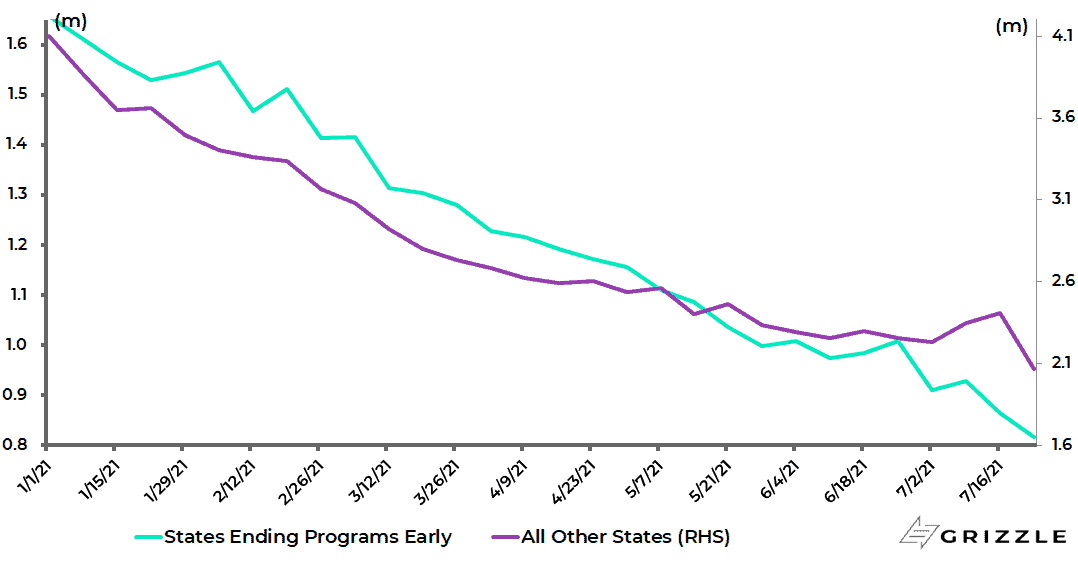

It is also the case that in the 25 Republican states that have already dispensed with the supplementary unemployment benefit, there has already been a marked decline in unemployment claims.

Continuing unemployment claims have declined by 25% since mid-May in those states ended the supplementary benefits in June/July, while claims in the other states were down 14%.

US continuing unemployment claims in states ended the supplementary benefits in June/July

If all of the above is the case, this writer is left wondering again whether the bond market knows something about the pandemic.

Surge in Cases Seems to be Driving the Bond Rally

It has been self-evident for some time that the best reason to own the long end of the US bond market, in anticipation of renewed Federal Reserve easing in the form of accelerated central bank balance sheet expansion, would be hard evidence that the vaccines are ineffective against new variants of the virus.

In the absence of any other explanation it has to be the case, as media focus on the surging Delta variant continues, that the latest surge in cases is what has been driving the bond market rally, and related concerns about renewed lockdowns.

Still the more the Delta variant cases rise without a corresponding rise in hospitalisations and deaths, the more it is a sign of vaccine efficacy which should, in many respects, be viewed as a positive not a negative.

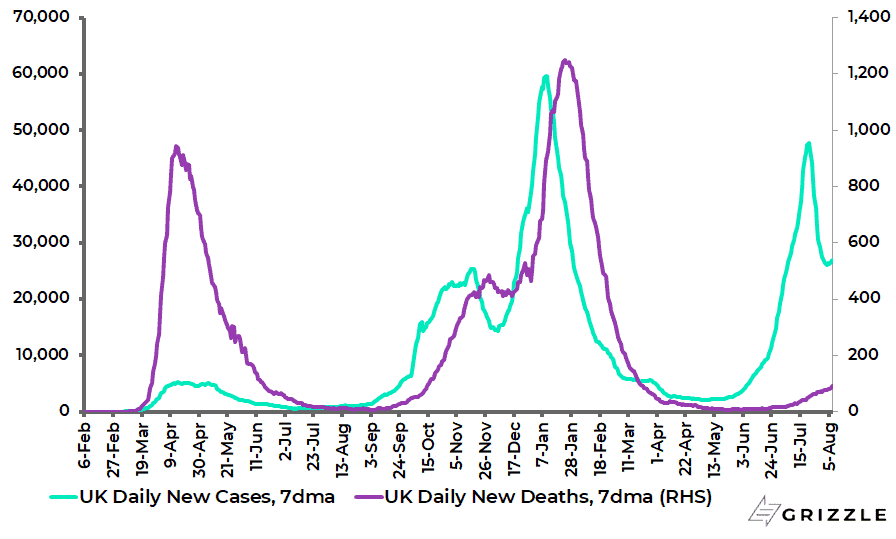

A good example is Britain, where Covid cases have surged, though they peaked on 21 July.

UK 7-day average daily new Covid cases and deaths

The data shows a marked decline in the Case Fatality Ratio (CFR) with Delta.

To be precise, the latest data from Public Health England shows the CFR running at 0.2%, which is substantially below the 1.9% level associated with the Alpha variant.

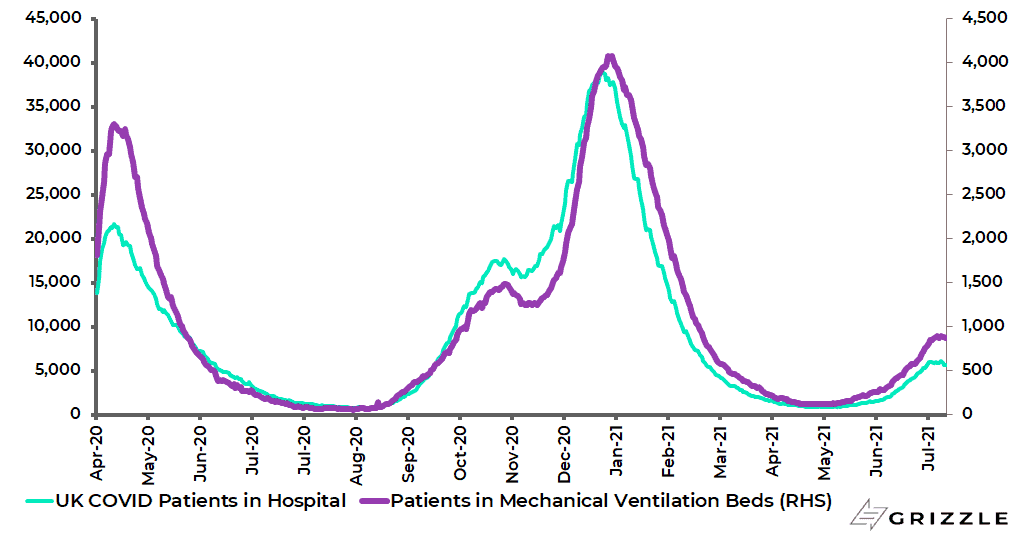

UK Covid patients in hospital and in ventilation beds

This is surely good news not bad news, though there is no doubt whatsoever that the Delta variant is way more infectious.

There is also no doubt that people who have been vaccinated twice can become infected with the Delta variant though, so far, in the vast majority of cases not in a way that requires hospitalisation.

The Delta Variant Will Keep Asia Closed Down

The Delta surge will also keep the nervous nellies in Asia from opening up in an ultimately futile effort to enforce their Covid suppression policies.

Singapore, for example, has closed all restaurants again from 22 July save for takeaways.

Still the Delta newsflow should also hopefully act as a further incentive to accelerate vaccinations in the region since vaccines ultimately remain the best defence against the new variants.

This writer was also interested to read that Chinese drug regulators completed last month an expert panel review of a Covid-19 mRNA vaccine co-developed by Shanghai-based Fosun Pharma and Germany’s BioNTech (see Caixin article: “China to use BioNTech vaccine as booster shot, sources say”, 15 July 2021).

Fosun plans to be producing 1bn doses per year by the end of this year at its Shanghai plant.

The Chinese authorities plan to use the vaccine as a booster shot for those who have already received home-made vaccines made by Sinovac and Sinopharm, according to Caixin.

China has already administered 1.76bn vaccine doses, though the Delta variant has in recent weeks arrived in China and has now spread to about 40 cities.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.