Dollar General (NYSE: DG) reported earnings this morning that topped both Wall Street’s EPS and Sales estimates.

Earnings per share (EPS) for the quarter came in at $2.10, surprising Wall Street’s expectation of $2.01 by 4.5%.

Revenue for the quarter came in at $7.2 billion compared to Wall Street’s estimate of $7.14 billion.

Net sales increased 7.6% QoQ and 8.3% YoY.

EBITDA came in at $1.25 billion, easily topping market estimates of $810 million.

Same-store sales growth in the fourth quarter grew at 3.2%, and 3.9% for the full year. Management considers same-store sales growth a critical metric for investors.

Shares are down 4% in premarket trading, along with the broader market on the continued fear of the coronavirus harming supply chains and consumer demand around the world.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Dollar General continues to put up solid numbers and is a defensive stock to own once the coronavirus panic subsides. When consumers are pinching pennies, as they do in recessions, value-priced stores typically do very well. [/su_panel]

Management says that they do not see the supply chain shock of the coronavirus “materially impacting their business” but list the COVID-19 pandemic as a risk to affecting the company’s supply chain in its forward-looking statement disclosure.

In an attempt to soften the blow from the markets and win back investor eyeballs, the Board of Directors voted to increased the quarterly dividend by 12.5% to $0.36 per share.

Dollar General has posted positive same-store sales growth for 29 consecutive fiscal years and continues to showcase superior profitability compared to peers, despite the absolute dominance of Amazon.

Discounted retail chains with small storefront locations and relatively little overhead costs prove to have a unique position in their market with trailing twelve-month (TTM) EBTIDA margins nearly double that of its peer group, with the exception of Target.

Dollar General EBTIDA margins (TTM) sit atop the peer group at 9.95%, while Walmart and Costco sit at 6.43% and 3.97%, respectively.

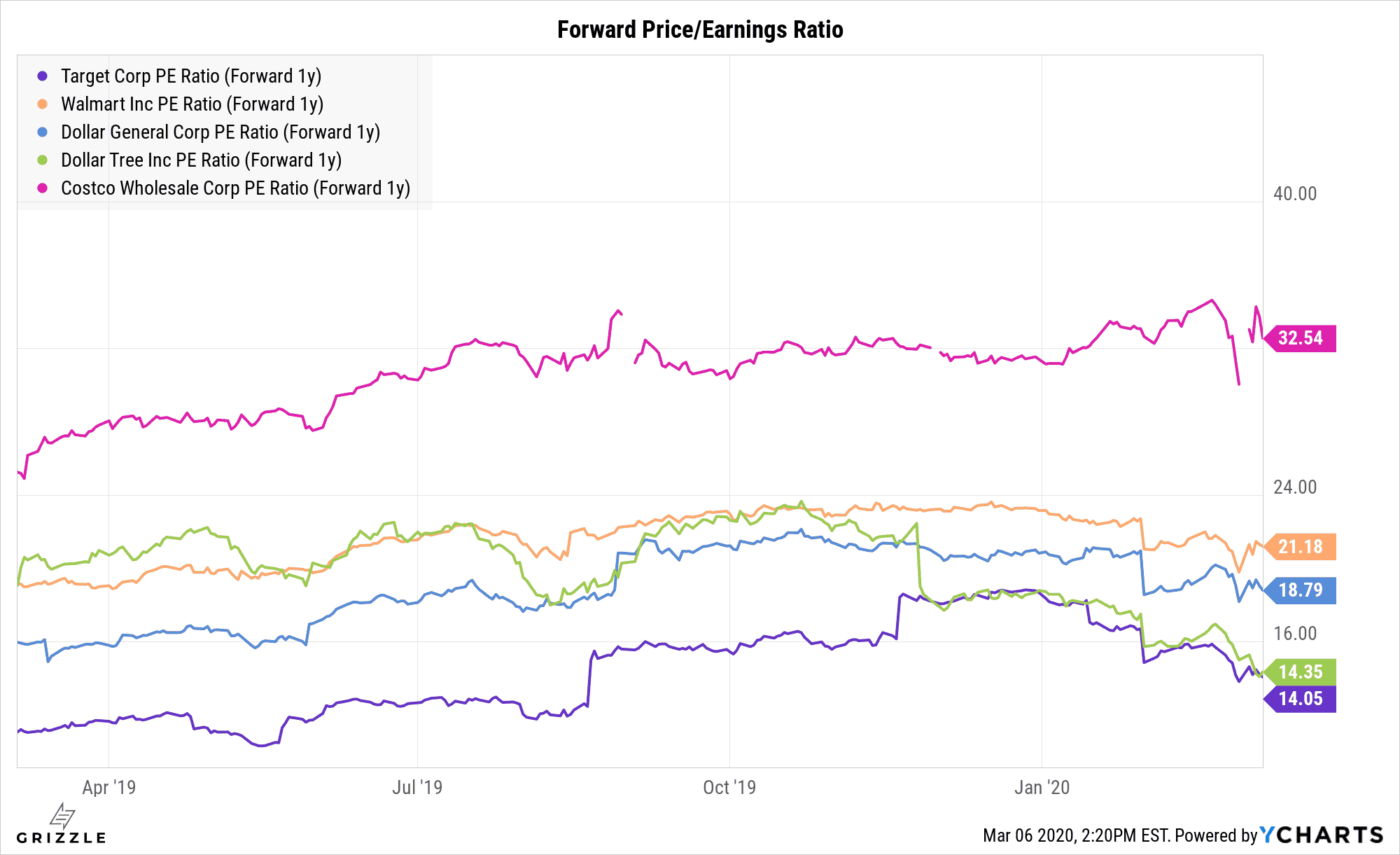

From a relative valuation standpoint in 1-year forward Price-to-Sales ratios, Dollar General’s stock trades at a lofty premium of 80% in relation to an average of its peers.

Although a forward-looking price-to-sales ratio portrays the company as being grossly overvalued, a comparison of forward-looking price-to-earnings ratios may be a more appropriate metric for analyzing profit-hungry retail chains.

Taking a peer group average of 1-year forward price-to-earnings ratios we find that Dollar General’s stock trades at a discount to Costco, but higher than some peers.

The stock looks neither cheap nor expensive on a relative basis.

In the last year, Dollar General’s stock has posted a record gain of 29.5%. The company repurchased $400 million worth of its common stock back in December of 2019 and has $561 million left in its share repurchase program.

Looking onward to fiscal year 2020, the company is eyeing net sales growth of 7.5% to 8% as it just opened a whopping 975 new stores. Management expects same store sales growth of 2.5%-3%; a touch under this year’s growth. They expect diluted EPS to grow at 11.5% and are estimating to repurchase another $1.15 billion of common stock.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.