Dropbox (NASDAQ: DBX) reported Q4 2019 earnings today which beat analyst expectations on both the top and bottom lines as it creeps towards profitability.

Sales for the cloud storage company came in at $446 million for the quarter, ahead of consensus estimates of $443 million.

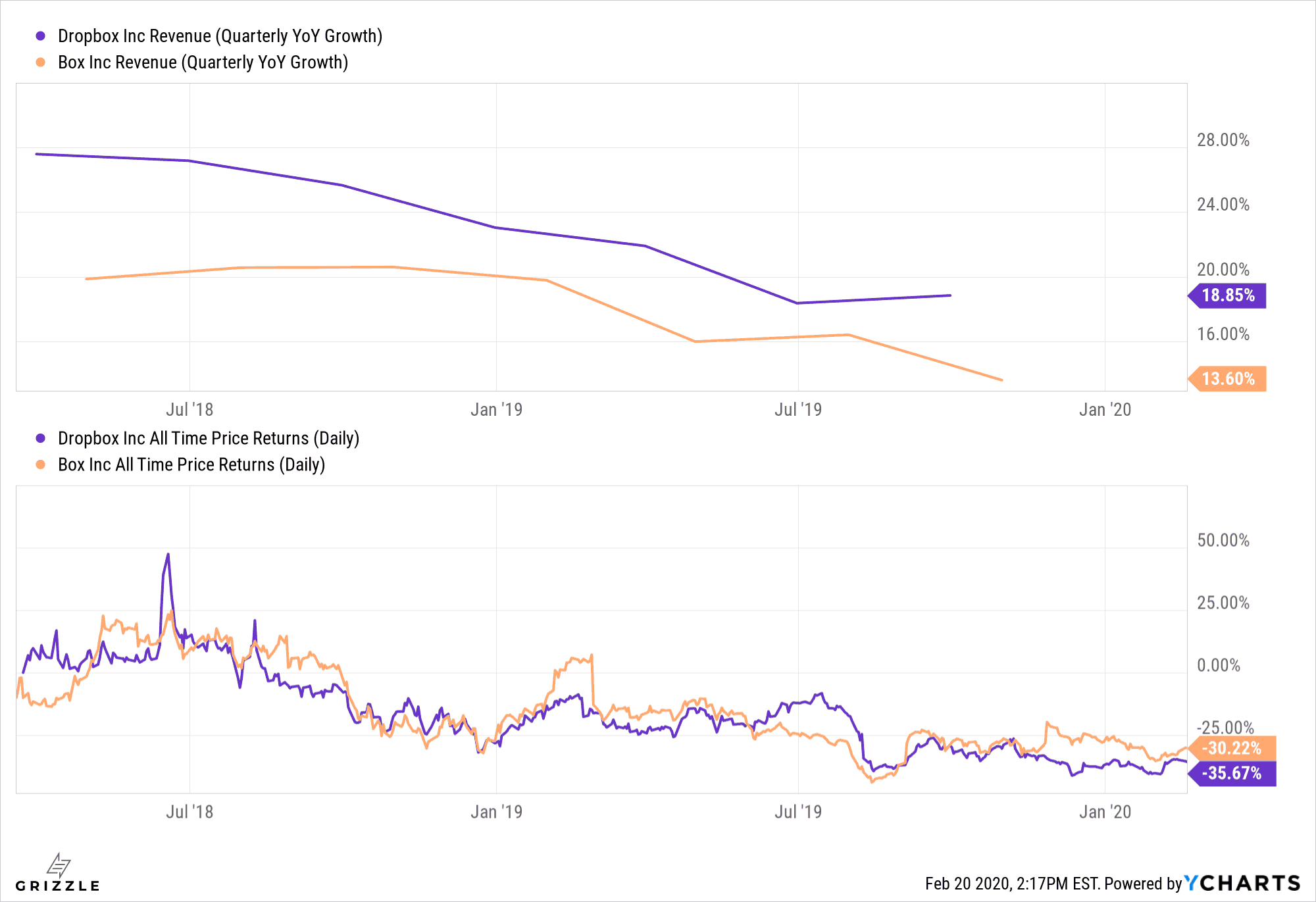

Overall revenues for the quarter were up 19% compared to the same quarter the previous year and up 19% for the full year 2019 compared to 2018.

Two other key metrics for the company are the number of paying users and the average revenue per paying user (ARPU). For the quarter Dropbox reported paying users totalled 14.3 million and ARPU of $125, up 12.6% and 4.5% respectively over the same period last year.

On the bottom line, Dropbox reported adjusted earnings of $0.16 per share which beat analyst expectations of $0.14. However, the company is still losing money on a GAAP basis with a loss of $0.02 per share.

The company earnings release is the first since CEO Drew Houston was named to Facebook’s (NASDAQ: FB) board of directors earlier this month which helped fuel a rally in the company’s stock. While investors seemed to be bullish on the news, it was one of several potential issues with the company that were raised in a report on Dropbox from short seller Spruce Point Capital Management who claimed it would be a distraction for the firm’s leader. Spruce Point also pointed out the lack of traction Dropbox has made in the enterprise market for cloud storage as competition from Google (NASDAQ: GOOG), Microsoft (NASDAQ: MSFT), and Box (NYSE: BOX) among others have focused on the enterprise vertical.

Since its IPO in the spring of 2018, Dropbox has had a rough ride on public markets. The stock is currently down 35% from the closing price on the day of the IPO and has also underperformed rival Box over that same time despite being able to grow top-line sales at a higher rate.

Going into this earnings report, Dropbox stock has seen a recent surge in price. Since the news of CEO Drew Houston’s appointment to Facebook’s board, the stock is up 9% and is up 2.3% overall year to date. Even Spruce Point’s short report, which identified a 25%-60% downside in the stock, barely dented Dropbox’s current momentum.

In aftermarket trading after the release of the earnings report, Dropbox was trading up 5% as of the time of publishing.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.