Marketplace platform eBay (NASDAQ: EBAY) announced results that beat expectations.

Marketplace platform eBay (NASDAQ: EBAY) announced results that beat expectations.

Revenue came in at $2.8 billion in-line with consensus of $2.81 billion while earnings per share of $0.81 beat the consensus estimate of $0.76 by 7% and was up 1% from the same quarter in 2018.

Ebay is still struggling to show any kind of growth with revenue down 3% in Q4 following no revenue growth in Q3.

Investors likely did not like the revenue decline which is why the stock is down slightly in after-hours trading on Tuesday.

EBay also released 2020 guidance which was 1% below consensus estimates on revenue and 4% above on EPS, nothing for investors to get excited about.

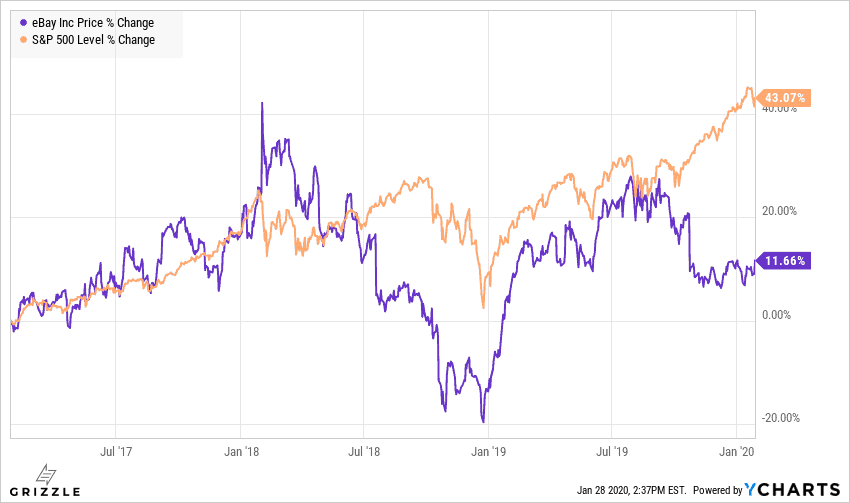

Investors punished eBay’s stock price during the last earnings report and it is now underperforming the S&P 500 by 32% over the last three years.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Management is having trouble finding growth and instead is cutting costs, selling non-core assets and pumping up shareholder buybacks. The 18% buyback yield is juicy, but if growth takes another leg down, investors will have wished they invested in a tech stock that’s actually growing. Invest elsewhere. [/su_panel]EBay Significantly Underperforming Against the S&P Recently

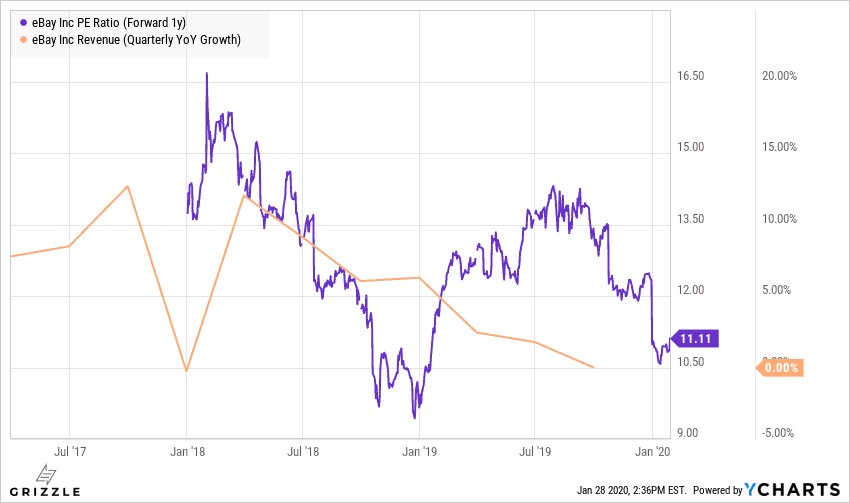

As revenue growth has slowed investors have pushed down the P/E ratio as they move on to higher growth opportunities.

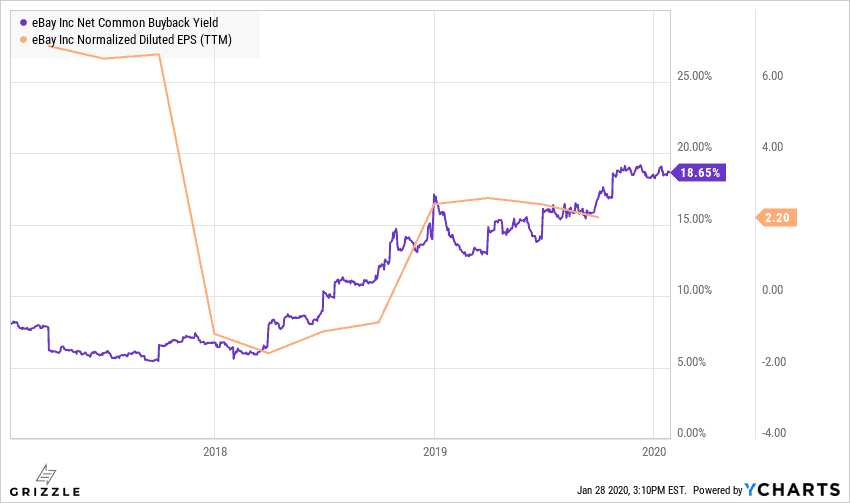

EBay is attempting to make up for the lacklustre growth and declining earnings by returning more money to shareholders and is now offering a juicy 18% buyback yield based on the current stock price.

Even though this may seem like a solid return opportunity for value investors, a buyback is still not a return of cold hard cash.

Buybacks decrease the share count so earnings per share should increase as well, but if the stock doesn’t reflect the better EPS by going higher, investors do not benefit from the buyback.

As long as EBay’s P/E multiple continues to decline it will offset the benefit of the rising buybacks.

Buyback Yield a Juicy 18% but Will it Last?

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.