Debt Deflationary Spiral or the End of The Disinflationary Era?

These are rather strange times. This writer is reading more and more predictions that the world is heading for a debt deflation of the type last seen in the Great Depression.

As a long time believer in the deflationary trend, on the back of the ever higher debt levels, this writer is not naturally unsympathetic to such views. Still, despite the above, the base case remains that the extraordinary policy response to Covid-19 marks the beginning of the end of the disinflationary era in existence since the early 1980s.

That said, it is also the case that the believers in debt deflation will be right if governments stick for longer to their lockdown policies than is currently the base case. This is because if substantial areas of economic activity are still locked down by government fiat next quarter then a liquidity problem will be fast turning into a solvency problem.

That is, of course, unless governments have by then taken it upon themselves to pay everybody’s wages and all companies’ costs. And such an extreme approach, which implies growing monetisation of government spending via central banks, is likely ultimately to have an inflationary outcome.

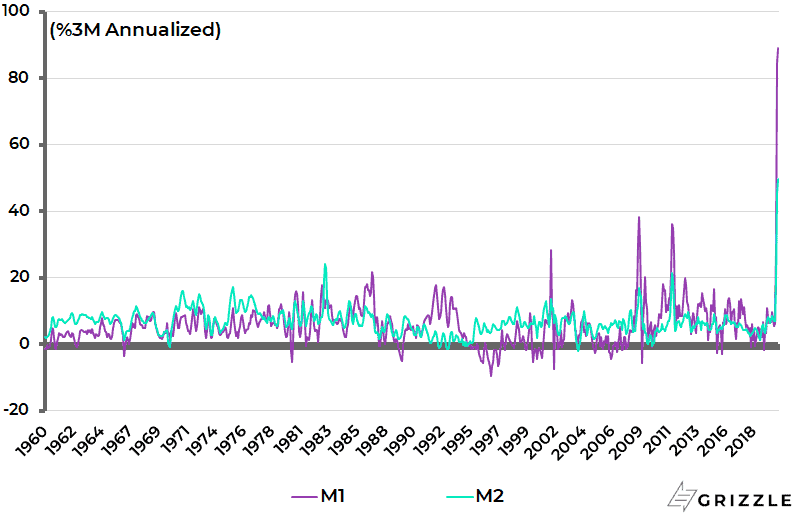

It is already the case that M1 and M2 money supply in America on a three-month annualised basis are now growing at their fastest rate since the data began in 1959. Thus, US M1 and M2 surged by a three-month annualized rate of 89.2% and 49.7% respectively in the four weeks to 4 May (see following chart).

US M1 and M2 Money Supply 3-month Annualised Growth

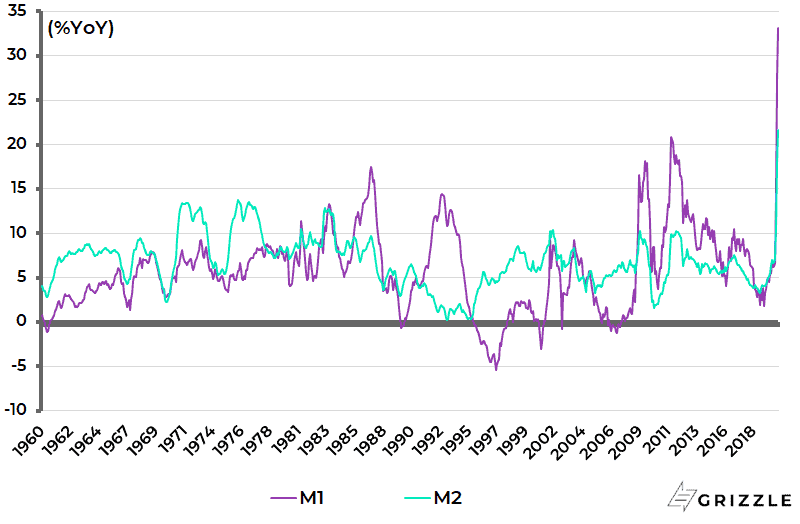

It is further the case that on a year-on-year basis US M1 and M2 rose by 33.1% YoY and 21.6% YoY in the week ended 4 May. This is also the highest YoY growth since the data began in 1959 (see following chart).

US M1 and M2 Money Supply %YoY Growth

Avoiding Economic Lockdown into Depression

Returning to the debt deflation risk, it would be truly extraordinary if governments locked down their economies into depressions to protect against a virus which is truly scary for inhabitants of nursing homes but should not be scary for the population at large, particularly for those aged under 50. Yet that is what will happen if these lockdowns persist in their present form for an extended period.

One question here is both government leadership and the perverse incentives created by government policies. As discussed here before (see Boomers Shafting Millennials & The Inflationary Impulse of Covid-19, 5 May 2020), the debate on opening up in America is dangerously politicised by the proximity of the presidential election.

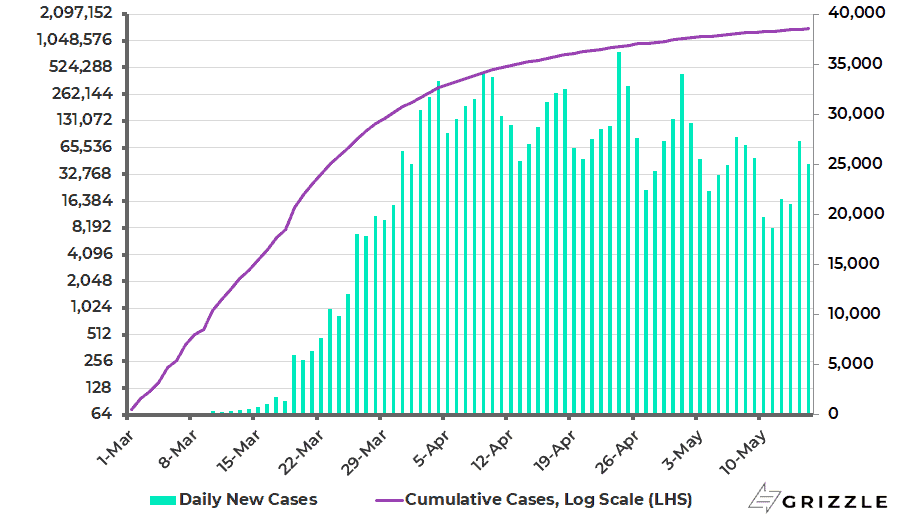

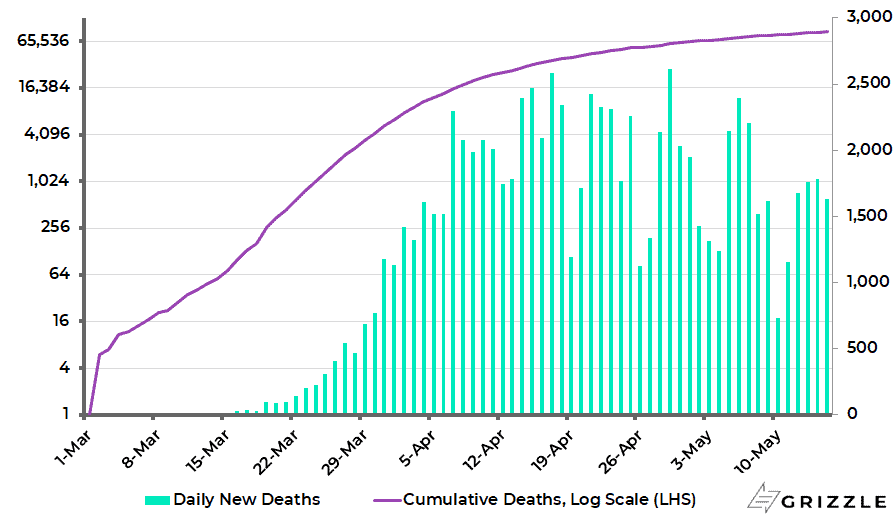

This is creating an uncoordinated policy response, in terms of different states following different policies as regards opening which does increase the risk of a relapse; most particularly as the rate of infections does not appear clearly to have peaked yet on a national basis in America, though that looks more likely to be the case in terms of the number of deaths.

The number of daily new cases and daily new deaths are still running at around 25,000 and 1,700 respectively per day, compared with the highs of 33,000 and 2,400 reached last month (see following charts). The most positive explanation for cases plateauing rather than falling is increased testing in America.

US Covid-19 Confirmed Cases

US Covid-19 deaths

Coronavirus Benefits Incentivize Americans to Remain Out of the Labor Force

The base case remains that the Trump administration will continue pushing for a staggered re-opening throughout this quarter. One issue will be employers’ concern about lawsuits if employees return to work and get sick. Another is the incentive not to work created by the Coronavirus-triggered increase in the unemployment benefit well above what many Americans would expect to earn in normal jobs.

Thus, average weekly unemployment benefits have increased from US$387 a week to US$987 a week. This is because, under the virus triggered fiscal stimulus programme, all unemployment insurance claimants will receive an additional US$600 per week.

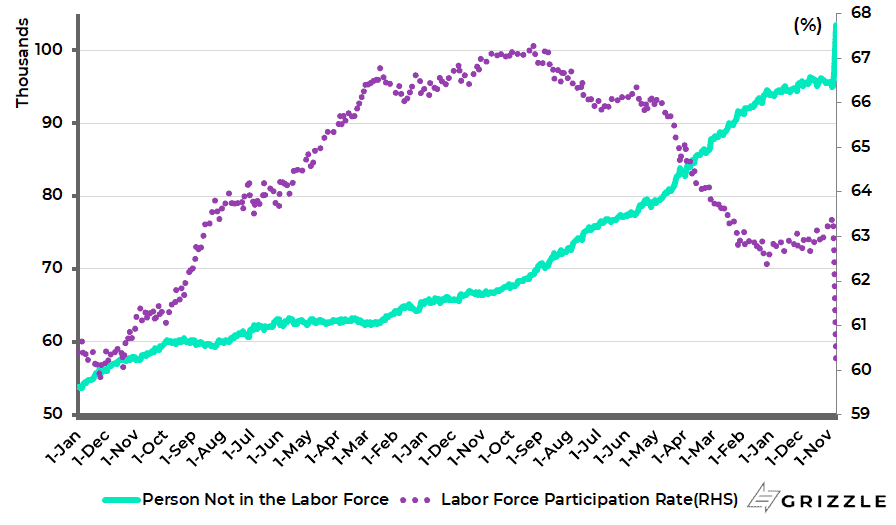

This increased unemployment benefit is meant to apply only until the end of July. But will it really be removed three months before the presidential election? If not, it raises the risk of a renewed increase in America’s nonparticipation rate which had only recently started to fall after rising to very high levels despite a ten-year long, now ended, economic recovery.

The number of Americans not in the labour force declined from a peak of 96.3m in August 2018 to 94.9m in January 2020, while the labour force participation rate rose from 62.7% to 63.4% over the same period. Still the number of Americans not in the labour force has since risen to a new record 103.4m in April with the participation rate falling to 60.2%, the lowest level since January 1973 (see following chart).

US Labor Force Participation Rate and Americans Not in the Labor Force

The Furloughed Welfare State of Mind

Meanwhile in another example of the dangerous incentives created by government policies a recent poll on 1 May found that 77% of British people supported the lockdown being extended. Another poll in late April showed that 67% of Britons would feel uncomfortable going to large public gatherings such as sport or music events while 61% would feel uncomfortable using public transport or going to bars and restaurants.

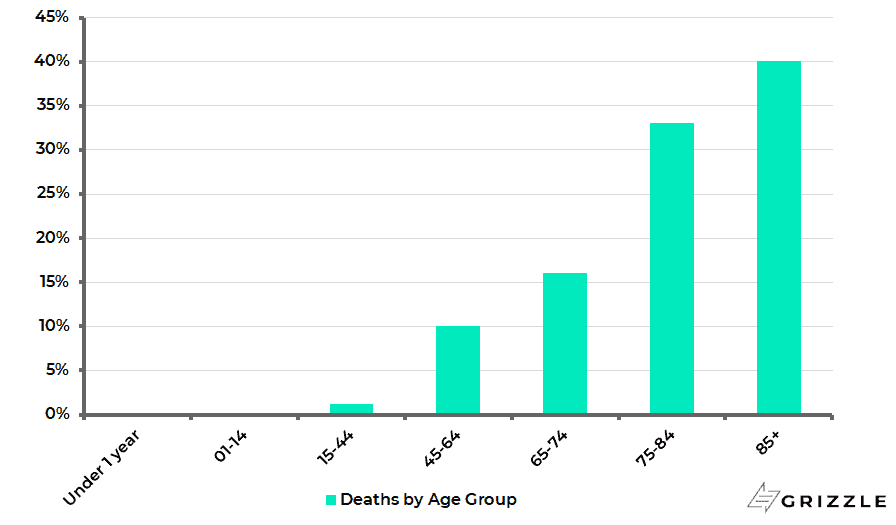

This, at first glance, surprises since the majority of people are not in mortal threat from the virus while the economic pain from the lockdown is obvious. In Britain 88% of the deaths involving Covid-19 are aged 65 or above (see following chart).

Share of Deaths Registered in the UK Involving Covid-19 by Age Group

But it becomes not so surprising when the incentives created by current policies are considered. The British Government, as of 11 May, has been covering 80% of the wages of 7.5m workers via the so-called furlough scheme which was originally meant to end at the end of June. It has now been extended to the end of October, though employers will have to share the burden with the government from August as furloughed workers will be able to return to work part-time.

The furlough scheme has been extended because of the obvious risk that many employees would have been laid off when the end of June deadline arrived, most particularly if the lockdown had not been relaxed in a material way in the interim.

This in why strong political leadership is required for politicians not to follow opinion polls which reflect the dangerous incentives created by virus-triggered interventionism.

In the developing world it is rather different since the welfare schemes are not in place to underwrite wages on the scale that is happening in the Western world. Rather in the case of developing countries, with young demographics, it is clear that the lockdowns in activity are more detrimental to general human welfare than the disease itself.

COVID-19: Asian Countries Have Fared Better Than the West

In this respect, it is a positive in Asia that more countries are following China’s example and opening up activity. Recent examples included Vietnam, Malaysia and Thailand. Still it is easier to open up when governments are perceived to have done a good job managing the crisis.

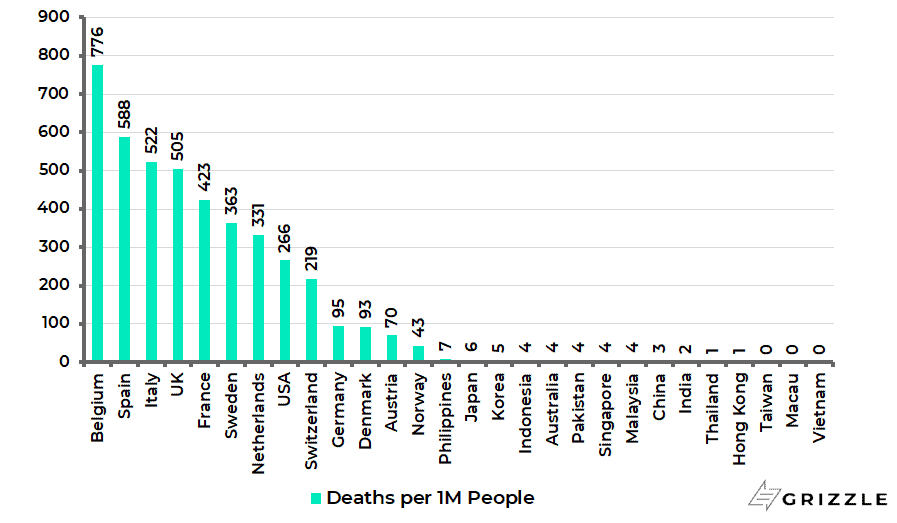

This is the case in many Asian countries where the remarkably low death rates stand in stark contrast to America and Europe. The number of deaths per 1m of population in Korea, Singapore and Thailand is 5.1, 3.6 and 0.8 respectively, compared with 266 in America, 505 in Britain and 423 in France (see following chart). In Vietnam there have been no reported deaths.

How to explain this extraordinary divergence? The best explanation heard so far, in the absence of any other, is that Asians tend not to be obese.

Number of Coronavirus Deaths per 1m of Population

The COVID-19 Infection Data Supports the View that Economies will be Opened Up Substantially by Next Quarter

Still where a government is perceived to have been behind the curve in managing the crisis, it is harder to lead from the front in terms of driving a re-opening.

Still the base case here remains what it has been from the start. That is that the virus will prove to be a three to four-month cycle and that the infections will fall as dramatically after peaking, as they rose dramatically in the first instance.

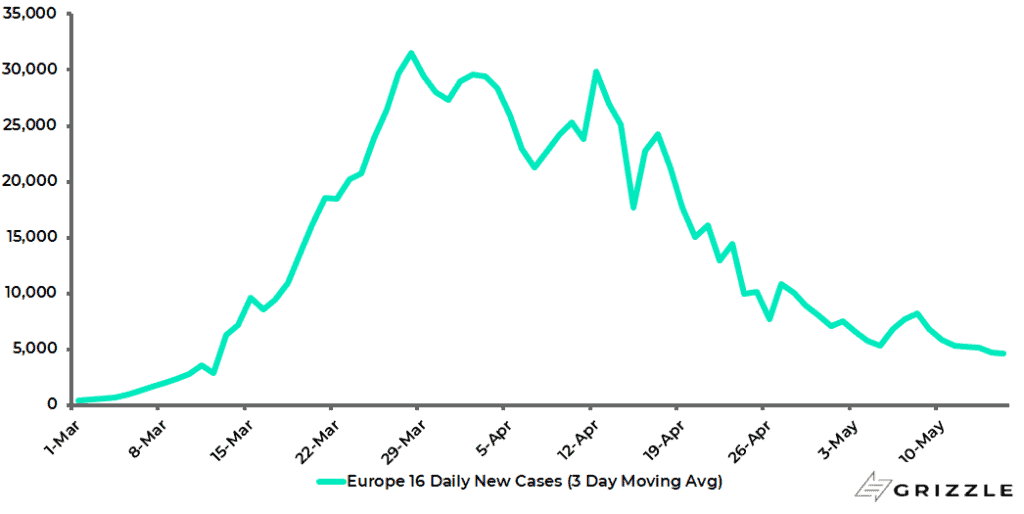

This is exactly the pattern now being seen in Western Europe where the number of new cases peaked in mid-April and is now down 84% from that peak based on a sample of 16 countries excluding Britain (see following chart).

Europe Daily New Coronavirus Cases

It is the trend signaled by such data which makes this writer take the view that economies will have opened up more substantially by the start of next quarter than is currently perceived to be the case by the consensus.

There are two main risks to this view:

- The first is a resurgence of infections on re-opening.

- The second is that, like financial regulators fighting the last war, governments stick to lockdowns long after the original rationale for imposing these lockdowns, namely hospital systems being overrun, has ceased to be a concern.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.